The EU’s Montenegro dilemma

Following a recent dispute over a $1 billion loan to Montenegro, the EU has an opportunity to take a more systematic approach to the growing Chinese presence in the Western Balkans

Montenegrin Deputy Prime Minister Dritan Abazovic has sparked a public debate that matches the drama of Steven Spielberg’s Oscar-winning film “Saving Private Ryan”. In the movie, a group of US soldiers in Normandy cross enemy lines to save American paratrooper James Ryan. The mission is filled with danger, but the officer in command orders them to take the risk out of a desire to spare Ryan’s mother the loss of her fourth son.

In Montenegro’s real-world drama, Abazovic recently suggested to the European Parliament’s Committee on Foreign Affairs that the European Union should embark on a rescue mission to refinance Montenegro’s $1 billion debt to the Export-Import Bank of China – a debt that the country incurred to pay for a highway, and that comes due in July this year. Abazovic’s intervention came across as a spontaneous gaffe rather than a serious request. Nevertheless, it was widely interpreted as a signal that Montenegro cannot repay the loan, shaking investors’ confidence and leading to a sharp decline in the value of Montenegrin government bonds.

In the foreign policy community, the incident prompted a number of geopolitical arguments on why the EU needs to step in to counter China’s growing presence in Montenegro and prevent another port in a NATO country from transferring to Chinese ownership. Speculation that China will gain control over the Port of Bar, on the Adriatic Sea, emerged after it was reported that Montenegrin land was the collateral of the loan. Chinese state-owned company COSCO Shipping Lines already owns a majority stake in the Greek port of Piraeus; 47 per cent of the Italian port of Genoa; and 35 per cent of the Dutch port of Rotterdam. So, the question is: will Brussels embark on a mission to save a fourth port in a NATO state?

In a Spielberg movie, a rescue mission would be the natural next step. Yet there is no such straightforward course of action in this story – which is more complex in its risks, and in its cast of characters and their weapons of choice.

To start with, the EU has no instruments to refinance loans from third states for projects nearing completion. The EU allocates funding through a meticulous financial plan that it negotiates over five years with member states and the European Parliament. Brussels does provide budgetary support to countries in need – not to repay third-party loans, but to push forward regulatory reforms. In the past, the Montenegrin government has avoided this sort of conditionality related to budgetary support.

At the same time, the loan agreement signed by Montenegro stipulates that it may not assign or transfer loan obligations to a third party without the prior written consent of the lender. According to the contract, the Montenegrin government has to inform the lender bank first if it cannot service its debt.

Nevertheless, it is unclear whether Montenegrin land actually serves as collateral in the loan, since the relevant part of the agreement is vaguely formulated. And comprehensive studies such as one by the Rhodium Group suggest that asset seizures by China are an extremely rare occurrence, while debt forgiveness and refinancing are common. The key issue is whether Montenegro’s new government is well-equipped to renegotiate Chinese debt deferment or forgiveness given the haste with which it has handled the process so far. The Montenegrin minister of finance has already clarified his government’s position by saying that Montenegro can repay the loan. Following a meeting with the Chinese ambassador in Podgorica, he praised the country’s work with the Chinese bank, called for greater cooperation with China on tourism, and argued that Montenegro should certify the Chinese vaccine.

In a Spielberg movie, a rescue mission would be the natural next step. Yet there is no such straightforward course of action in this story.

Therefore, while there may be no need to refinance Montenegro’s highway loan, the EU should take the opportunity to reflect on a more general set of problems related to governance and accountability in Montenegro and other Western Balkans countries. These problems are central to the geopolitical challenges the bloc faces in the region. The EU needs to create a rigorous, long-term strategy on the nexus between governments’ lack of accountability and the growth of Chinese and Russian influence. This would be far more effective than firefighting in crises whose parameters are unclear.

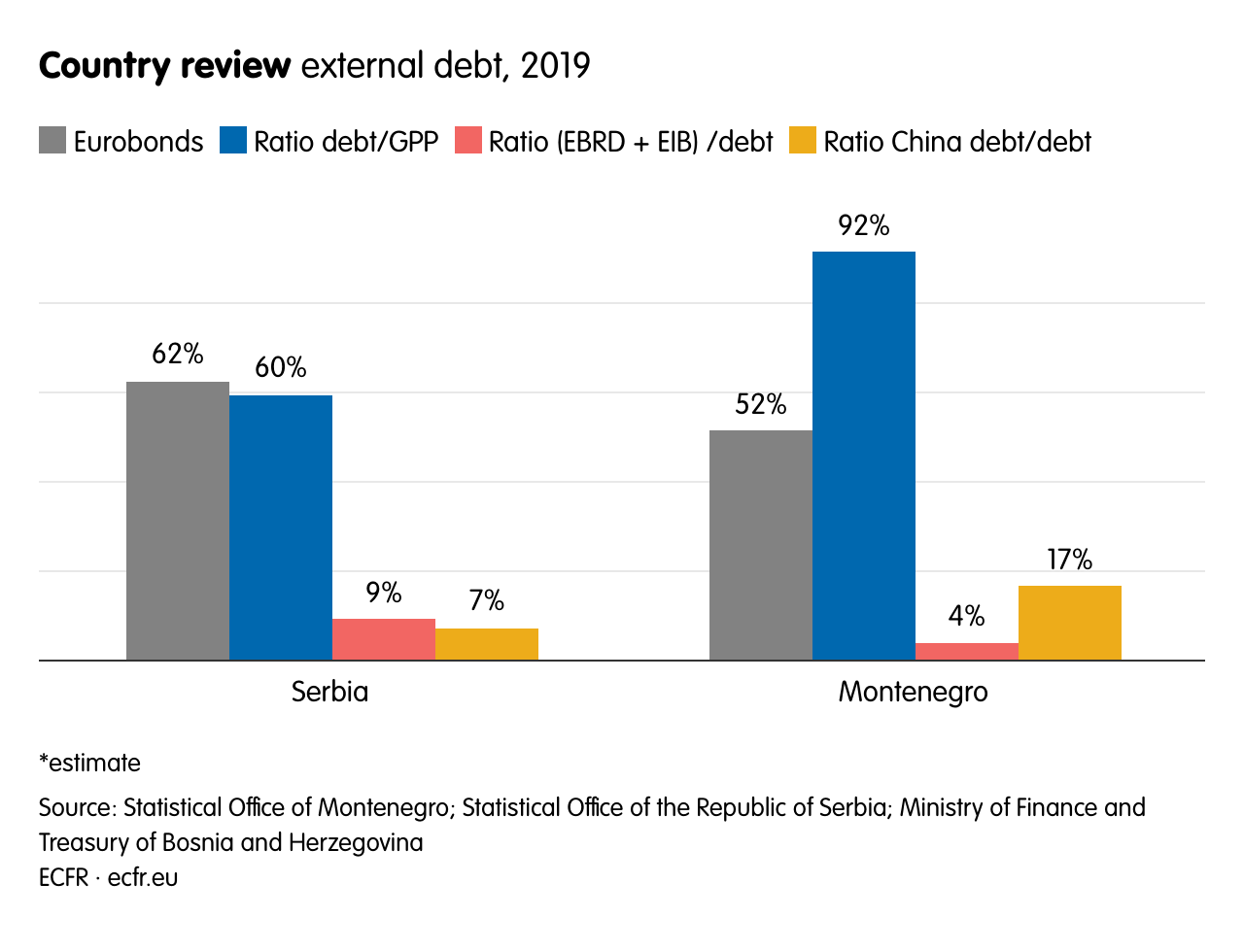

The fiscal challenges in Montenegro are real. Highly dependent on tourism, the country’s economy has contracted by 15 per cent last year largely due to a loss of revenue caused by coronavirus-related travel restrictions. Montenegro’s external debt reached 91.6 per cent of its GDP in 2020. The country’s debt to China amounts to 16.7 per cent of the total, which it will have to repay at an interest rate of 2 per cent over 20 years. Meanwhile, 51.56 per cent of Montenegro’s external debt is in Eurobonds. In Montenegro, Serbia, and Republika Srpska, the sale of Eurobonds on international markets – with higher interest rates and shorter repayment periods than those that the International Monetary Fund (IMF) and the EU usually offer – is a preferred mechanism for covering budget deficits and servicing old debt.

These relatively unfavourable terms are widely perceived as the price for avoiding IMF and EU conditionalities on the economy, the rule of law, and governance. And this is where the problem lies: the reluctance of many political actors in the region to proceed with reforms. Montenegro has only reached one agreement with the IMF since joining the organisation. Global financial conditions are currently favourable – allowing Montenegro to borrow internationally at relatively low interest rates, despite its poor credit rating – but continuing to borrow through the issuance of Eurobonds could become more difficult if these conditions tighten. In the medium to long term, debt sustainability may become a greater risk for the country than Chinese seizure of its territory.

| Serbia | Montenegro | |

|---|---|---|

| EIB | 1,219.42 | 109.66 |

| EBRD | 86.00 | 38.15 |

| Paris Club | 856.10 | 69.35 |

| WB IBRD | 2,197.10 | 181.53 |

| WB IDA | 150.40 | 23.83 |

| MMF | 455.10 | 71.62 |

| Eurobonds | 5,135.90 | 1,977.45 |

| Russia | – | – |

| China Exim Bank | 1,008.12 | 640.54 |

| External government debt | 3,627.10 | – |

| Total external debt | 14,028.00 | 3,835.27 |

| Ratio unknown debt / debt | 62.47% | 51.56% |

| Ratio debt / GDP | 59.50% | 91.60% |

| Ratio (EBRD + EIB) / debt | 9.31% | 3.85% |

| Ratio China debt / debt | 7.19% | 16.70% |

Therefore, if the EU provides a support package to Montenegro with conditionality on macroeconomic management and sustainability, this should be based on clear reform conditions. The bloc should closely monitor compliance with the terms of the agreement in the economic and governance realms, as well as in the political system.

The ruling coalition in Podgorica is dominated by Moscow-orientated parties, whose political agenda could prove destabilising for the region. Montenegro was recently shaken by a scandal in which the new head of its intelligence agency published classified information about another NATO member state. The Montenegrin minister of justice received a rebuke from the United States and the United Kingdom for denying the Srebrenica genocide (as established by the rulings of the International Criminal Tribunal for the Former Yugoslavia and the International Court of Justice). The new Montenegrin parliamentary majority has proposed amendments to a law on the special prosecutor’s office previously agreed with the Venice Commission. These changes seem geared more around internal political disputes than efforts to strengthen the rule of law.

Finally, the EU should use the loan debacle as an opportunity to take a more systematic approach to the growing Chinese presence in the Western Balkans. For instance, the Montenegrin prosecutor’s office is already conducting an investigation into the alleged violation of environmental standards in the construction of the highway. This process should extend beyond Montenegro: China is investing in energy and infrastructure projects across the region.

Chinese contracts’ violation of EU public procurement and environmental norms has become a huge issue in Serbia and Bosnia. As aspiring EU members and recipients of Instrument for Pre-Accession Assistance (IPA) funds, these countries should be striving for greater approximation with the EU directives rather than violating them. Under an economic and investment plan it announced last year, the EU has committed €9 billion from the IPA and €20 million in a loan guarantee facility to the Western Balkans – funding that will cover the energy and transport sectors, which are often targets of Chinese investment. The EU needs to attach more stringent conditions to both IPA funds and budgetary support, to deter future violations of procurement, environmental, and rule of law standards. As much of this EU investment will require co-financing, the bloc should restart a debate on cooperation with the US on infrastructure projects in the Western Balkans.

As the EU works to increase its leverage in Montenegro and the region, it will need to think strategically. Above all, the bloc should aim to promote accountability and good governance, which are its best hope for containing both Chinese and Russian influence.

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.

{kind=link}