Against the flow: Europe’s role in kickstarting Algeria’s green transition

Summary

- Russia’s war on Ukraine has reshaped European energy markets and lent new urgency to the EU’s decarbonisation plans, altering the incentives of the bloc’s energy partners.

- Surging demand for Algeria’s oil and gas exports has temporarily undercut pressure for domestic reform, including in the energy sector.

- But growing local energy consumption and European plans to reduce fossil fuel imports in favour of renewables threaten Algeria’s rentier system.

- The country’s leaders have taken only minimal steps to build renewable energy capacity and remain fixated on raising hydrocarbon investment.

- While Algeria has little spare capacity to increase its hydrocarbon exports in the short term, it holds far more promise for Europe as a long-term partner in renewable energy.

- Europe’s ambitious climate goals, deep pockets, and technical expertise make it well placed to help Algeria kick-start a robust energy transition – if the country chooses to go along.

- At a high-level energy dialogue this month, EU and Algerian officials will convene for the first of many discussions to reshape the future of their energy partnership.

Introduction

Until recently, energy security had slipped down Europe’s list of policy priorities. Europeans’ memories of the 1970s oil crisis had faded, the effects of human-induced climate change were becoming ever more visible, and energy imports were flowing steadily. These trends culminated in the approval in 2020 of the European Green Deal, which committed the European Union to reducing greenhouse gas emissions by 55 per cent by 2030 (compared to 1990 levels) and achieving carbon neutrality by 2050. The accompanying Fit for 55 package followed last year.

But Russia’s full-scale invasion of Ukraine in February 2022 upended Europe’s confidence in its energy security. The conflict prompted the EU to re-evaluate its energy supply chains, provider relationships, and timeline for the transition to renewables.

In May, with the prospect of a cold winter on the continent looming, the European Commission unveiled REPowerEU, its accelerated plan to sever the EU’s energy ties with Russia – long its largest supplier of oil, coal, and natural gas. In the short term, the package has boosted EU countries’ efforts to rapidly secure alternative sources of fossil fuels. However, the package’s greatest impact may be to expedite Europe’s energy transition: it substantially raised targets for both the production and import of renewable energy resources, especially green hydrogen. Brussels has pledged to mobilise €300 billion in grants and loans to end Europe’s reliance on Russian oil and gas by 2030. These measures, and the sweeping transition they aim to support, create significant opportunities for Europe’s energy partners that join it in this effort – and great risks for those that do not.

Algeria, already a key energy supplier to Europe, can choose to become an even more critical one. A major hydrocarbon producer, the country provided around 10 per cent of the EU’s gas imports in 2020-2021 (making it the third-largest source of foreign gas, after Russia and Norway) and around 3 per cent of its oil imports. But, for as long as Europe has been seeking to pivot away from fossil fuels, it has viewed renewable energy as Algeria’s greatest asset. It is the world’s tenth-largest country and the biggest in Africa, with nearly 2.4m square kilometres of land and more than 1,600km of coastline. The Sahara makes up much of its surface; more than 3,000 hours of annual sunlight could allow Algeria to build one of the world’s greatest solar fields. A 2020 International Finance Corporation study ranked the country first in Africa for its potential for wind power generation, which is “equivalent to over 11 times current global installed wind capacity”. Algeria’s wave energy potential is, according to other research, “one of the highest” in the Mediterranean basin. The country’s location means that the cost of exporting renewable energy to Europe would be relatively low, making it appear to be a natural partner for the EU in its energy transition plans.

Yet, so far, such ambitions have been stymied by political factors. In reaction to a long and painful history of colonisation by France, Algerians are often wary of foreigners’ intentions. In today’s globalised world, Algeria is an outlier. The country is isolated and wary of any perceived threat to its hard-won sovereignty. Fossil fuel exports anchor its economic model – and, for decades, have underwritten both extensive elite corruption and the subsidies leaders use to ensure citizens’ well-being and buy social peace.

As a consequence, the Algerian government is anxious about the prospect of transitioning away from these precious resources in favour of unfamiliar new technologies. The boom in oil and gas prices caused by the Ukraine conflict and Western sanctions on Russia only increases Algeria’s reluctance to venture into the unknown. To date, leaders in Algiers have made only a minimal effort to develop renewables.

EU and Algerian officials’ October 2022 energy dialogue, their first high-level meeting of this kind since 2018, will come shortly before the global COP27 climate conference and an expected renegotiation of Algeria’s EU Association Agreement, which has been in place since 2002. These meetings give Algeria and the EU an opportunity to recast their partnership for a new era. They also coincide with a period of intense anxiety in Europe about gas supplies. However, in light of production constraints, Algeria has a limited capacity to assist Europe further in this regard (though there are other ways that the two sides can help each other in the short term). Nonetheless, this limitation may be beneficial in one sense: it should prevent Europe’s short-term energy concerns from giving Algerian energy officials false hope about the future of hydrocarbons – false hope that could have precluded longer-term energy collaboration between the sides.

For Europe, the talks are a chance to invite Algeria’s leaders to join the energy transition. Given fossil fuels’ centrality to the country’s political and economic system, Algeria will not drop oil and gas overnight. But it is possible for the country to rapidly scale up its renewables industry in the coming decades. Algeria can reduce its dangerous overreliance on hydrocarbons by accelerating its energy transition, initially to meet domestic energy demand and later to develop new energy exports. This dependency has led the country into crises before and, given fossil fuels’ uncertain future, is likely to do so again.

Such a transition could help Algeria ensure the well-being of its growing population and maintain or even expand its role as a reliable energy supplier to Europe. The transition could also help Algeria become part of the solution to climate change, which has increasingly severe implications for the country.

For all these reasons, the EU needs to identify how to promote and facilitate such a shift in Algeria. This paper analyses how energy resources shape political and economic dynamics in the country, including through its minimal efforts to develop renewable energy. The paper then explores the dilemma Algerian policymakers face and how Europeans might provide solutions to it.

While recent developments in global energy markets have created obstacles to the green transition in Algeria, they have also increased the potential costs of inaction. By working together, Algeria and Europe can sustain their energy partnership and contribute to their long-term economic and energy security.

The state that oil made

Hydrocarbons have been a pillar of the modern Algerian state since its inception. Oil and natural gas were discovered in Algeria shortly before the country gained independence from France in 1962. This presented an unparalleled boon to a young nation eager to develop its economic and human capital. As a consequence, Algeria moved quickly to build up its energy sector. By 1964, the country had inaugurated the world’s first commercial liquid natural gas production facility at Arzew, near Oran. Newly founded universities and technical institutes began training highly qualified petroleum engineers. In 1969 Algeria joined the Organization of the Petroleum Exporting Countries (OPEC). It nationalised its oil and gas industry in 1971, consolidating all energy resources, infrastructure, and revenues under state control. In a country that prizes its sovereignty above all else, that event is still celebrated as a milestone in Algerians’ long struggle for self-determination.

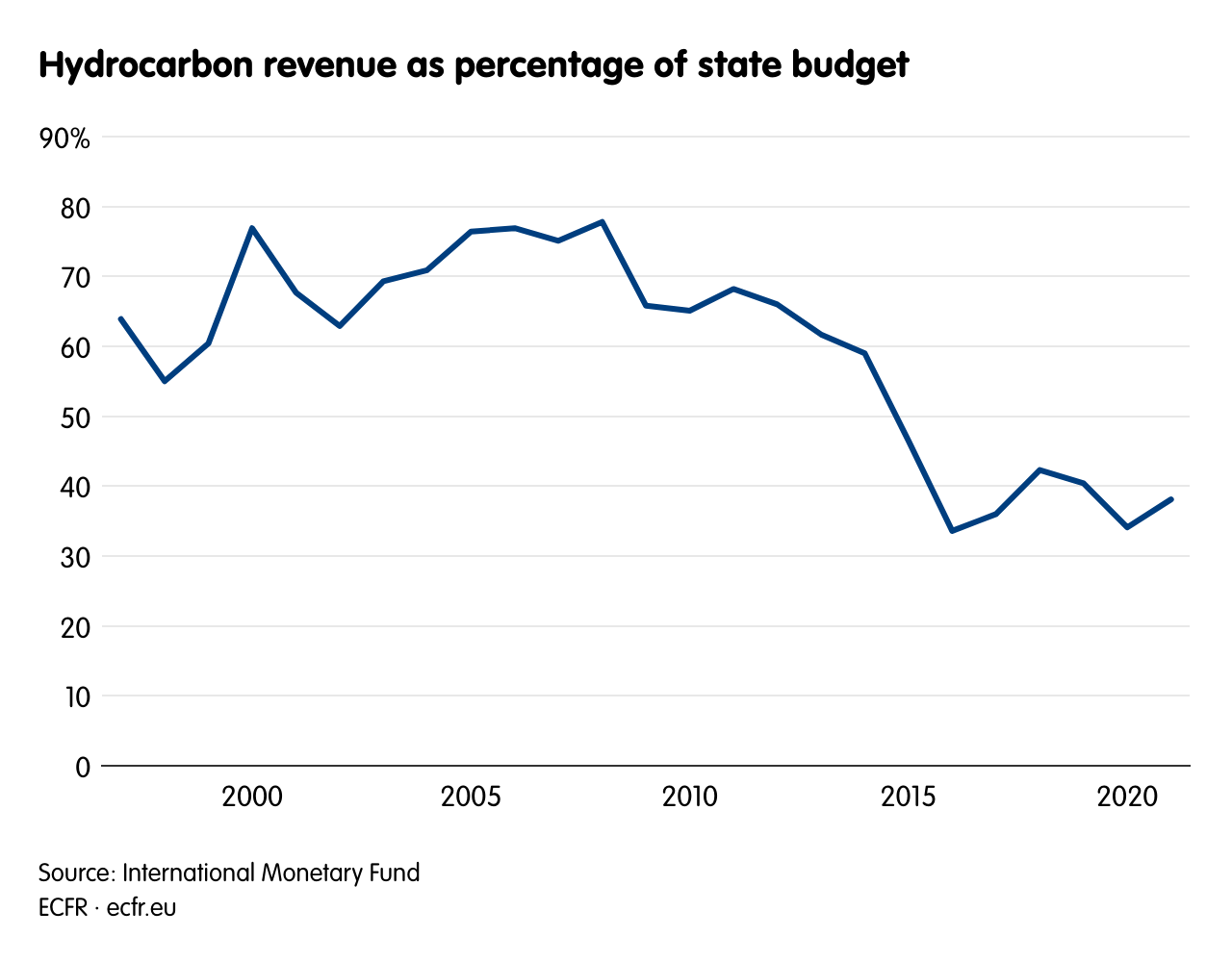

Today, Algeria is Africa’s largest gas producer and an important global oil supplier, holding the world’s tenth-largest gas reserves and fifteenth-largest oil reserves. Hydrocarbon sales have accounted for more than 90 per cent of its export revenues and around half of the state budget in recent decades. The country’s energy wealth has produced numerous distortions in the economy and led to a dependence that is difficult to break – a classic example of the resource curse. Advocates of the energy transition in Algeria need to contend with the reality that their proposals threaten to upset long-established equilibria.

Algerian leaders claim that oil and gas wealth has allowed the country to exercise an independent foreign policy, taking principled stands when and where it chooses. Throughout the 1960s and 1970s, Algeria was a stalwart supporter of anti-colonial liberation movements across the developing world. Today, it continues to promote the Palestinian cause and provide material support to Western Sahara’s independence movement. Algeria spent the cold war balancing its close military ties with the Soviet Union against its commercial links to Europe. The country now maintains strong bilateral relations with Russia and China, as well as Europe and the United States. Algerian leaders argue that a dependence on foreign support forces North African countries with fewer resources, such as Morocco and Egypt, to enact policies that are unpopular at home, ranging from structural adjustment programmes to the normalisation of relations with Israel. By contrast, in the past year, Algeria has ended its diplomatic relationship with Morocco over myriad disputes and dramatically scaled back its ties with Spain in response to changes in Spanish policy on Western Sahara. Without its financial independence, Algeria would have found it difficult to make either move.

Domestically, Algeria’s vast oil and gas resources and their centralisation under state control have long created substantial incentives for state capture. The result is le pouvoir (the power), Algerians’ traditional shorthand for the opaque and ever-shifting constellation of rival clans who have long occupied the upper reaches of the state apparatus. Drawn from the political class, the business elite, and the powerful army and intelligence services, members of le pouvoir battle for senior positions to gain access to state revenues, which they have long siphoned off through corruption schemes. According to one estimate, senior officials embezzled nearly one-third of the $1 trillion Algeria earned from hydrocarbon sales between 1999 and 2019. An anticorruption campaign launched in 2019 has led to prison sentences for dozens of former prime ministers, cabinet members, other public officials, and oligarchs, but has recouped little of the stolen money.

Algeria’s rulers use a mixture of repressive tactics and generous handouts to convince citizens to overlook such crimes. Under the regime’s social contract, Algerians risk jail time for criticising their leaders – but they receive free health care and education, alongside considerable subsidies for housing, staple foods, energy, water, and more. Last year, those subsidies reportedly cost the state €32 billion, or 23 per cent of GDP. Since independence, Algeria has constructed thousands of new schools and hospitals, as well as millions of low-cost housing units. Expansive public sector employment also helps buy social peace, while cash stipends to war veterans and their descendants, among others, are designed to ensure the loyalty of key constituencies. The government typically increases these payments when it needs to quell public protests – be it localised demonstrations, such as the anti-fracking ones that broke out across southern oasis towns in 2015, or wider protests like those seen during the 2011 Arab uprisings.

While the country’s hydrocarbon wealth enriches its leaders and provides a minimum standard of living for ordinary Algerians, it also has economic costs. An exchange rate policy engineered to maximise oil revenues reduces the competitiveness of other exports, stifling local production and feeding unemployment – which has fluctuated between 10 per cent and 12 per cent in the last decade, with rates for young people nearly three times higher. Algeria’s informal economy contains an estimated one-third of its currency and half its workers. Since the statist agricultural and industrial boom in the 1970s, non-hydrocarbon sectors of the formal economy have withered. In contrast to its neighbours, Algeria has resisted developing a tourism industry and has largely missed the tech boom of recent decades.

Overreliance on hydrocarbons also leaves Algeria vulnerable to fluctuations in international energy markets, which have had dramatic consequences for the country. In the late 1980s, a collapse in oil revenues prompted Algerian leaders to announce cuts to public subsidies, triggering mass protests. In response, the government initiated a hasty political liberalisation process that precipitated a decade of bloody civil war. The country’s leaders failed to learn the lessons of that tragedy: in 2014 they were again caught off guard by a rapid plunge in oil and gas prices, which led to several years of erratic austerity measures. These policies rankled Algerians, contributing to the emergence in 2019 of the Hirak, a peaceful nationwide protest movement. The Hirak forced long-serving president Abdelaziz Bouteflika to resign and – amid calls for sweeping reform of the political system – briefly posed an existential threat to le pouvoir.

Algeria continues to bear these costs less because its leaders see them as an unavoidable drawback of hydrocarbon wealth than because dependence has produced self-reinforcing political and economic inertia. This inertia shapes the structure of le pouvoir, whose internal fragmentation and competitiveness prevent its members from supporting strategic shifts that would be in the country’s long-term interest. Typically, Algeria’s elites only reach a consensus when they face an existential threat – and only at the last minute. While politicians have room for manoeuvre on minor issues, their approach to major policy challenges is characterised by short-term crisis management rather than long-term planning.

In this environment, talk of large-scale reform is inversely proportional to global energy prices. The surge in these prices caused by the Ukraine crisis has only complicated efforts to pursue an energy transition and reinforced Algerian leaders’ attachment to hydrocarbons.

A new oil and gas boom

Late last year, Algeria was in dire straits: global energy prices had collapsed, successive waves of the covid-19 pandemic had pushed the economy into recession, inflation and unemployment were at their highest levels in years, shortages of staple goods were deepening, and the country’s foreign exchange and domestic reserves were dwindling. Algerian leaders announced plans for tax increases and subsidy cuts in an effort to rein in unsustainable deficit spending.

These measures would have begun the process of replacing Algeria’s blanket subsidies with a system targeting only the neediest households – a move the International Monetary Fund has long advocated. But the price of Algeria’s Saharan Blend oil increased from just $15 per barrel in April 2020 to $100 per barrel in February 2022. Days before Russia launched its full-scale invasion of Ukraine, Algerian President Abdelmadjid Tebboune – a former housing minister who replaced the ousted Bouteflika in December 2019 – abruptly called off the planned tax increases and subsidies reforms, before announcing a new programme of cash transfers to unemployed young people. He later promised pay increases for millions of public-sector employees. Algerian leaders now seem unlikely to proceed with the subsidies reforms.

In July, the government passed a major investment law that ignored proposals from the country’s leading independent business council and has not substantively improved Algeria’s challenging investment climate. The law streamlines several bureaucratic procedures and designates tax incentives for priority sectors, including renewables. Yet it does not address fundamental concerns about regulatory consistency, fair market access, and the rule of law.

High energy prices have not only eroded Algerian leaders’ incentives for reform but also shifted their focus to efforts to expand hydrocarbon revenues – which are already projected to reach $50 billion this year, or nearly as much as the two previous years combined. Amid a steady stream of high-level visits from prospective energy buyers, Algerian leaders are negotiating price increases or new supply deals with Spain, France, and other countries. State oil and gas producer Sonatrach signed a major new gas export package with Eni that includes studies on a potential green hydrogen pilot project – one of several deals Algeria negotiated with Italy earlier this year. The Algerian government has resurrected long-dormant plans for a trans-Saharan pipeline that would bring Nigerian gas to Algeria for export. Sonatrach’s recent exploration efforts have delivered a flurry of oil and gas discoveries, albeit with production investments slower to follow.

Few of these developments will increase Algeria’s energy revenues or export volumes in the short term. Despite its reliance on hydrocarbons, the country may be missing its moment. Algeria’s oil output is capped by OPEC quotas and, after years of underinvestment in infrastructure, the country has little capacity to rapidly scale up gas production. Liquefied natural gas terminals and pipelines linking Algeria to Spain and Italy have been operating below capacity, despite sky-high European demand for alternatives to Russian gas. Many of Algeria’s oil fields are maturing and reducing output – requiring more gas injections to keep oil flowing. In recent years, Sonatrach has sometimes struggled to reach its OPEC output quotas. Algeria’s gas exports rebounded from the pandemic with a 5 per cent increase last year, but have fallen again in 2022. It is now unclear whether the government will fulfil its promise to boost these exports before the end of this year.

In January 2022, Sonatrach announced plans to invest $40 billion over five years to expand production. However, the company has since pressured its foreign clients to help cover the costs of this expansion. In June, energy minister Mohamed Arkab told Der Spiegel that anyone hoping to buy energy from Algeria would be expected to invest in upstream development. He also blamed European environmental priorities for the decline in Algerian investment, implying that Europe was to blame for Algeria’s difficulties in expanding production.

Such messages show that Algerian leaders intend to revitalise their hydrocarbon sector and sustain it for decades to come. They also speak to the critical role that Europe plays in bankrolling the process – which will provide European officials with leverage in their upcoming energy discussions with their Algerian counterparts. They will need to balance their use of that leverage carefully, ensuring that long-term hydrocarbon investment deals do not hinder the pursuit of EU climate goals.

Need for change

In the short term, the boom in global energy prices has limited the prospects for a green transition in Algeria. Nonetheless, two important local factors signal that there is a growing need for Algeria to reduce its reliance on fossil fuels.

Domestic energy consumption

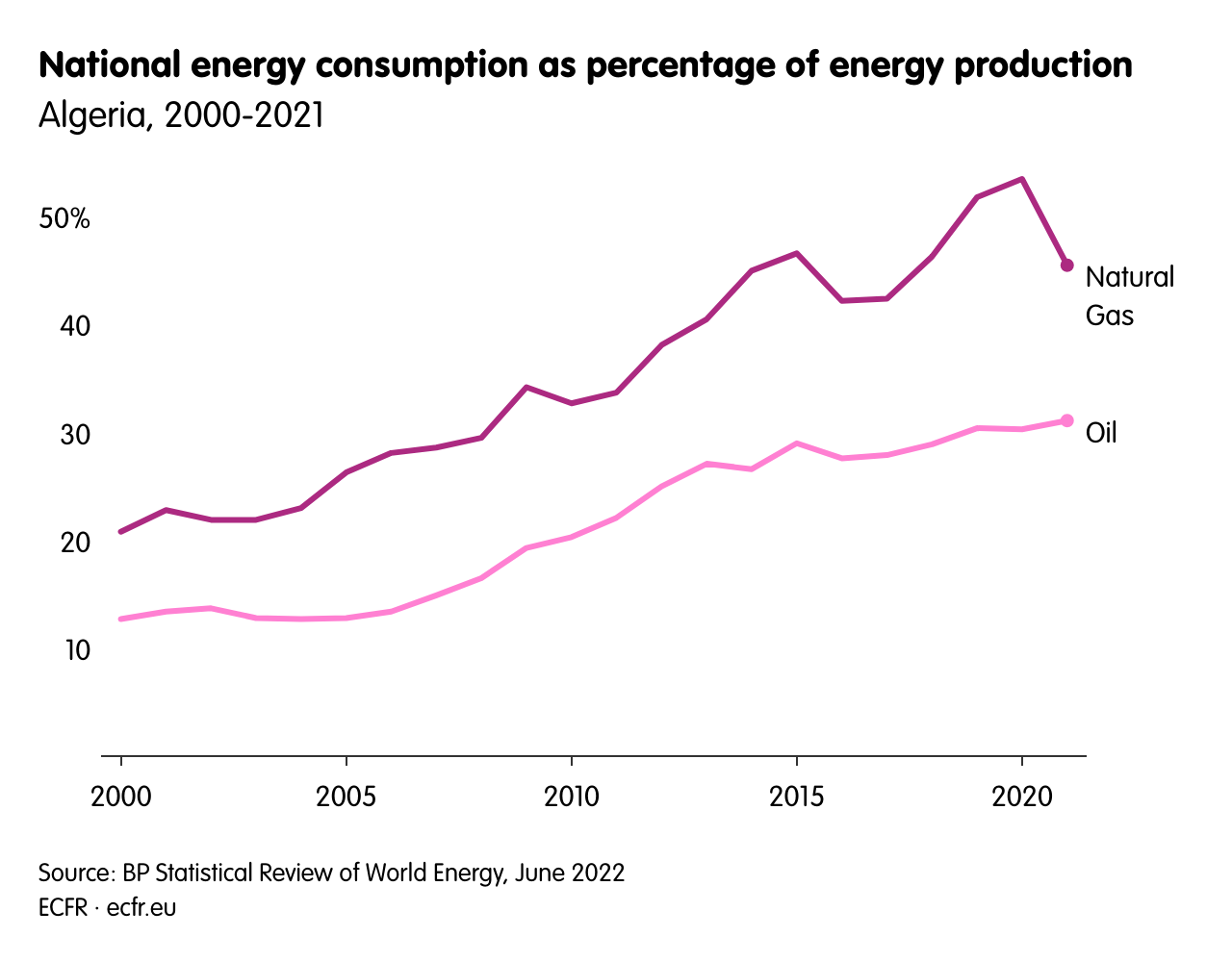

In recent decades, Algeria’s rising domestic energy consumption has substantially reduced its energy resources available for export, sapping its largest source of revenue. Due to the challenges discussed above, Sonatrach’s gas production increased by just 10 per cent, and its oil production declined by a similar percentage, between 2000 and 2021. In the same period, Algeria’s population grew by more than 40 per cent and its standards of living also rose, prompting a boom in housing and infrastructure construction, as well as in purchases of energy-hungry cars, air conditioners, and appliances. The country’s blanket subsidy programme reduces domestic energy prices by more than half, stimulating consumption and costing the state $112 billion in the last decade, equivalent to 5.8 per cent of GDP.

As Algeria is Africa’s most electrified country – with more than 99 per cent connectivity – these changes have translated into increased power consumption, almost all of which comes from burning fossil fuels. National energy consumption has more than doubled since 2000 and will further increase: Algeria’s population of 45 million is projected to reach 60 million by 2050. State electricity provider Sonelgaz projects that, to keep pace with growing demand, it will need to upgrade electricity infrastructure and expand generation capacity from around 25,000MW to 32,000MW by 2030. This presents an important opportunity to develop the renewables sector.

Every unit of oil or gas consumed in Algeria is another unit sold below market value and not exported for profit. For decades, Algeria’s leaders have mostly elided this trade-off in public statements while promoting energy efficiency and savings initiatives. But these half measures have done too little to reduce the surge in national consumption. Recently, against the background of rising energy prices, officials have begun to speak more explicitly of the need to rein in domestic consumption to ensure Algeria can maintain its all-important oil and gas exports. This new prioritisation of export substitution provides one of the most promising openings for the EU to help Algeria build a robust renewables sector. The first step in this process is to focus on meeting Algeria’s domestic power demands, before investing in development of low-carbon energy exports.

Climate change

The effects of human-induced climate change are growing more visible to Algerian policymakers and citizens alike. According to a government white paper published last year, climate change already costs the country 1.8 per cent of its GDP annually. The expansion of the Sahara has long been a concern for Algerian policymakers, with their failed schemes to combat desertification reaching as far back as the 1970s. During an especially arid summer last year, wildfires ravaged northern Algeria – killing at least 90 people and piercing the public consciousness like never before. Another 43 people died in wildfires in summer this year. Declining rainfall, rising temperatures, migration to urban areas, and growing water consumption by households and farms are increasing the pressure on reservoirs and aquifers, leading to intermittent cuts in public services.

The growing strain on Algeria’s water resources illustrates some of the destructive feedback loops created by climate change. Since 2014, water shortages have obliged the government to begin decommissioning the 13 hydroelectric turbines Algeria built into dams across the north. To cover these shortages, Algeria is investing heavily in seawater desalination, with 12 plants already in operation and more under construction. While this investment will help alleviate shortages, desalination is an energy-intensive process that adds to the demand for power.

Climate change largely results from external factors such as historical emissions from wealthy industrialised nations – which is why Algeria forcefully advocates in international forums for those countries to help the global south adapt. Yet external factors are increasingly exacerbated by internal ones. Between 1962 and 2020, Algeria accounted for one-third of a per cent of global CO2 emissions, placing it among the top 40 global emitters in that period. Its CO2 emissions per capita have increased by 50 per cent since 2000. And these figures do not account for emissions from Algerian oil and gas exported for consumption abroad, nor for the vast quantities of gas flared, vented, or leaked from Algeria’s hydrocarbon production and processing facilities – including major leaks revealed earlier this year, which are estimated to have the same warming effect as several million cars.

Burning fossil fuels also increases local air pollution. A World Bank analysis of health sector data found that air pollution caused nearly 8,000 premature deaths in Algeria in 2013. Many Algerians are aware of this problem – a 2019 survey found that one-third of them see climate change as a “serious concern” – but there is little public outrage about the rising costs of Algeria’s use of fossil fuels, partly due to fears that mitigation measures could hinder the country’s development. Algeria’s few civil society organisations dedicated to environmental justice have tended to focus on containing the worst excesses of extractive industries, and on ensuring that projects in these sectors create jobs in local communities. For now, Algeria lacks a substantial domestic constituency for an energy transition on either environmental or public health grounds.

Algeria’s existing transition plans and activities

In recent years, Algerian leaders have made tentative steps to exploit the country’s abundant renewable energy potential. In part, they have sought to hedge against uncertainty about fossil fuels’ capacity to ensure Algeria’s fiscal stability and energy security in the long term. They have also done so to keep up with global trends – and to demonstrate to Algerians that the country is not falling behind its neighbours on their watch.

The government has built up and repeatedly reconfigured the state’s institutional architecture around renewable energy, but has been slow to take more substantive action. Some of those institutions have been in place for decades. For example, the research-focused Renewable Energy Development Center has its origins in a colonial-era solar-research lab. The government has created or adapted other institutions following constitutional revisions in 2016 and 2020 that established citizens’ “right to a clean environment” and explicitly cited the threat of climate change. In 2017 the government enlarged the Ministry of Environment to include a renewable energy portfolio, before spinning this off in 2020 as the new Ministry of Energy Transition and Renewable Energy (MTEER). In 2019 the government created the Commission on Renewable Energies and Energy Efficiency (CEREFE) within the prime minister’s office. In 2020 Algeria established a dedicated renewable energy college at the University of Batna to develop national expertise. Last year, it created the National Renewable Energy Company (known by the Arabic acronym ‘SHAEMS’, meaning ‘sun’) under Sonatrach’s and Sonelgaz’s joint ownership but the MTEER’s nominal oversight. The company manages renewable energy procurement, a function previously performed by the Ministry of Energy.

The government may have ostensibly placed the MTEER at the heart of its energy transition plans, but it did not give the institution the resources it needed to fulfil its mission. In its first year, the MTEER was headed by veteran energy scientist Chems-Eddine Chitour. But, in July 2021, the government replaced him with Benattou Ziane, a medical doctor whose primary qualification for the job was his position in a political party loyal to Tebboune. The MTEER’s budget was far smaller than that of the main energy ministry. And, after the political mood shifted against reform, Ziane had little political capital.

However, his ministry still had ambitious targets – the latest in a series of climate change and energy transition goals that Algeria has announced in recent years. In the 2015 Paris Agreement, Algeria pledged to reduce its greenhouse gas emissions by 7 per cent by 2030. First published in 2011, its plan to achieve this goal set targets of 4,500MW of installed renewables capacity by 2020 and 22,000MW by 2030, enough to cover a quarter of Algeria’s power generation. Yet, by the start of 2020, Algeria had installed capacity equivalent to less than a tenth of the first target. The government responded by revising its goal to 16,000MW (including 1,000MW of decentralised, off-grid generation) by 2035.

In recent years, as global prices of solar photovoltaic (PV) cells have fallen precipitously, Algeria has adjusted the breakdown of its renewables targets to focus primarily on this technology. The trend has made low-carbon green hydrogen economically competitive, prompting a surge in international interest in this area. The hydrogen industry received a further boost in the EU’s REPowerEU plan, which included the ambitious target for the EU to import 10m tons of low-carbon hydrogen annually by 2030.

These developments have presented new opportunities for Algeria. In November 2021, German development agency GIZ published a study outlining Algeria’s potential as a hydrogen producer and exporter. The same month, the Algerian government established an inter-ministerial working group to develop a national hydrogen road map, which appears likely to largely mirror the vision in the German study.

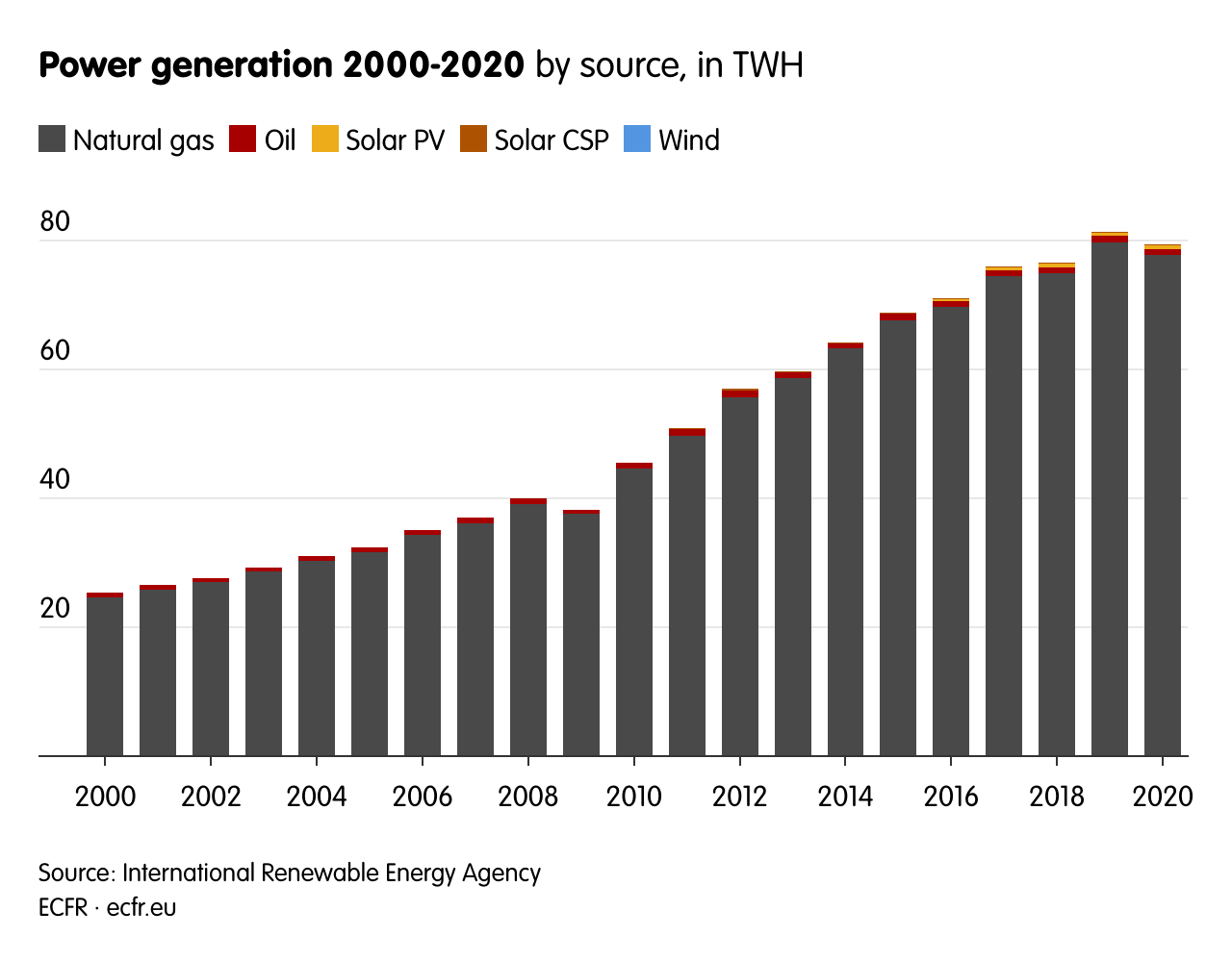

All this institutional reshuffling, target setting, and planning has produced limited results. According to CEREFE, by December 2021, Algeria had 438MW of installed solar and wind capacity, merely 26MW more than two years earlier and just a tenth of Morocco’s renewables capacity. Nonetheless, the Algerian solar industry is developing and might soon boost these figures. Private factories in Batna, Bordj Bou Arréridj, Mila, and Ouargla can now produce solar panels with a combined capacity of 460MW each year – even if they cannot yet do so at prices that are globally competitive. The government’s heavy subsidisation of electricity ensures that private citizens and businesses have little incentive to buy these firms’ panels. Nonetheless, the state is supporting companies in the sector by including local sourcing requirements in solar tenders.

Foreign power producers are eager to enter one of the world’s largest potential renewables markets, but have often been dissuaded from doing so by an inhospitable business climate and unfavourable contractual terms. Following years of undersubscribed or cancelled tender attempts, the authorities have been working to reduce obstacles to the process. In 2020 the authorities freed the renewable power sector and many others from the so-called 49/51 rule, which had long mandated a majority Algerian stake in any joint ventures. This change and the aforementioned 2022 investment law removed some of the major impediments to attracting foreign investment and expertise. A revised electricity law, which the government promised last year and which is expected to clarify the provisions of international energy partnerships, has yet to materialise – as has an energy transition law that the MTEER was reportedly preparing earlier this year.

With the legal framework still unresolved, in December 2021, SHAEMS nonetheless launched Solar 1000MW, a long-awaited tender to build and operate installations at 11 sites across central Algeria. Ziane spent the following few months meeting with foreign investors and power producers, but the tender – which Algeria intended to be the first in a multi-year series of projects to bring it closer to its renewables target – has fallen flat. SHAEMS delayed the submission deadline from April to June and then indefinitely, claiming that bidders needed more time to meet technical and budgetary requirements. If they are built at all, the installations will likely not begin production before 2024 – well beyond the initial target of this year. Planned follow-on tenders are likely to face delays as well.

In response to this disarray, Tebboune folded the MTEER back under the environment ministry in a September 2022 cabinet reshuffle. The ministry had little to show for its two years of operation. In light of Algerian leaders’ failures with renewables procurement and targets, the demise of the MTEER raises questions about the credibility of their public commitments to the energy transition and their capacity to attract international expertise in the renewables sector.

Algeria’s dilemma

After two years of fruitless experimentation under the MTEER, Algeria has again reset its institutional infrastructure for energy transition but not yet clarified policy priorities or provided missing components of the legal framework.

Meanwhile, Algeria is just one of Europe’s many energy partners that have recently struggled to interpret Europeans’ “mixed signals” – as Faten Aggad, senior adviser at the African Climate Foundation, told this author.[1] In response to the current energy shortage, she noted, European governments have scrambled for gas supplies and issued household energy subsidies even as the European Commission increased renewables targets, spreading confusion about Europeans’ priorities.

Early last month, European Council President Charles Michel visited Algiers in a preliminary attempt to clarify Europe’s aims, setting up the October 2022 energy dialogue. The EU’s representatives will have the difficult task of negotiating to maintain or even expand its supplies of Algerian oil and gas, while also encouraging Algeria to accelerate its development of low-carbon renewables for future export.

Algerians across the energy sector and the government have diverse views of the energy transition, supported by one series of arguments for delaying Algeria’s energy transition and another for accelerating it. Europeans will need to understand both mindsets if they are to convince Algeria to join them in a rapid transition to renewable energy.

Arguments for a delayed transition

As discussed, the inertia in Algeria’s energy sector is partly a product of calls for delay and inaction. Europeans should be prepared to address these calls.

Enduring demand for oil and gas

Algeria has a substantial interest in preventing its gas and oil reserves from becoming stranded assets. Long-term projections of global hydrocarbon demand vary dramatically, reflecting the diverse worldviews of the forecasts’ authors. In one scenario of rapid green energy adoption, the International Energy Agency projects that, between 2020 and 2050, global demand for gas and oil could decline by 55 per cent and 75 per cent respectively. In response to the current turmoil in energy markets, many policymakers in Algiers project that demand will fall far more slowly than this, if at all. Soaring energy profits have reinforced that view – as has the sight of environmentally conscious European governments ramping up investment in fossil fuel supplies and infrastructure. The EU’s decision in summer 2022 to classify natural gas as a green energy source only added to Algerians’ hopes that the bloc would not abandon fossil fuels in the coming years. Some even question Europeans’ assumption that a global energy transition is inevitable. And they reason that, even if Europe decarbonises its economy, they will still have eager customers for oil and gas in China, India, and other emerging markets.

Immediate costs and uncertain future benefits

Elected leaders everywhere dislike investing resources today in exchange for uncertain gains in the distant future. This is particularly the case in Algeria, whose decision-makers tend to measure upfront investment in not only financial terms but also the huge amounts of political capital that would be required to affect a change of this magnitude, given the country’s fragmented top-level decision-making structure. The uncertainty around the benefits of such reform compounds the problem. Nonetheless, it is possible to imagine how Algeria could gain economically from greater use of renewables in the steel, cement, and fertiliser industries – or of opportunities for synergies such as agrivoltaic farming (planting crops under solar panels). As Europe looks to reduce its dependency on Chinese manufacturing, Algeria could present an attractive nearby alternative due to its low energy and labour costs, as well as its untapped reserves of minerals critical to renewables and tech products. However, as discussed, Algerian officials have yet to articulate a vision for a post-hydrocarbon Algerian economy built around abundant, low-cost renewable energy sources.

Risks of rapidly evolving technologies

For years, European pleas to Algeria around renewables exports focused on electricity transmission via undersea cables like those that link Morocco and Spain. Some such projects are still under consideration. For instance, Algiers and Rome are exploring the possibility of constructing a cable between eastern Algeria and Sardinia. However, in the last few years, green hydrogen has leapt to the fore of the discussion. This is despite the fact that hydrogen was not among the principle axes of cooperation set out in the previous EU-Algeria energy dialogue, in 2015, and that the EU only published its first hydrogen strategy in mid-2020. Today, green hydrogen is at the centre of Europe’s energy transition plans, propelled by its potential as a high-density energy resource suited to transport, storage, and industrial use – and promoted by a burgeoning European hydrogen lobby. Europe’s rapid pivot from electric transmission to hydrogen transport has made some Algerian policymakers wary. As one Algerian energy analyst told this author: “there’s a fear that they’ll get it wrong.”[2]

Green hydrogen is relatively new and untested. Various studies have raised serious questions about its cost-effectiveness as an export product – suggesting, for example, that green hydrogen from Eni’s proposed Algerian solar facility would be 11 times as costly as natural gas even before transport. Proposals to transport green hydrogen from Algeria to Europe by repurposing gas pipelines would require expensive retrofits and could corrode the infrastructure. Mixing hydrogen with natural gas or other substances for transport may alleviate these problems, but optimal concentrations are still under study. Leakages could contribute to global warming, undercutting the climate benefits of decarbonisation. Many of these issues involve engineering challenges that, in the face of an influx of European research funding, likely have technical solutions. But the costs, scale, and timeline those fixes require could dramatically shift the economics around hydrogen production and export.

Meanwhile, Algerian officials worry about rapid changes in solar, wind, and other power generation technologies – which threaten to make investments inefficient or obsolete in just a few years. As before, they argue that it is safest to wait for the technologies in question to mature.

A history of successful delays

Europeans have long tried to tap into Algeria’s huge renewable energy potential. The German-led DESERTEC consortium launched in 2009 to meet a substantial portion of Europe’s electricity needs by constructing massive concentrated solar power (CSP) installations in the Middle East and North Africa, then linking them to Europe with undersea cables. The international engineering, construction, and investment firms that backed the project had mixed success courting governments in the region – with Algeria’s among the most sceptical. DESERTEC faced serious technical challenges, including transmission losses on long cables, grid compatibility issues, and peak-time power surges. It also suffered from CSP’s high cost and complexity compared to PV solar, the price of which was then plummeting. Most importantly, though, the initial concept focused exclusively on providing energy to Europe. This ignored growing local power needs and gave DESERTEC a reputation for green colonialism that it struggled to shake off even after revising its plans to prioritise supply to local markets. Due to these and other failures, DESERTEC collapsed in 2014.

Algeria’s ambassador to the EU, Mohammed Haneche, told this author that stakeholders in DESERTEC had come to Algeria with an interesting concept but insufficient financing.[3] Their assumption that the country would pay for the project up front appears to have rankled leaders in Algiers.

Despite this, other states have pressed on with the DESERTEC model – none more enthusiastically than Morocco. In recent years, the country has spent more than €5 billion on large-scale solar projects. The most prominent of these is the 510MW Noor CSP plant near Ouarzazate, which the Moroccan government built between 2013 and 2018. The plant has garnered Morocco international acclaim and helped offset its foreign energy imports but, due to high operating costs, it generates power at an annual loss of €80m. The process of cleaning the plant’s mirrors requires large quantities of water, which is sourced from a nearby reservoir in an arid region. Local communities have voiced their frustration that their land, water, and public funds are being squandered, but Morocco is continuing to build new facilities.

Meanwhile, various Gulf countries have begun investing heavily in renewable power generation and making forays into hydrogen production, including for export. Egypt, Tunisia, and others are following suit – all potentially providing valuable lessons for Algeria.

Change and social peace

Policymaking in Algeria is far from democratic, but the Hirak provide the country’s elites with a stark reminder that there are limits to what the public will accept. Algerian leaders have learned to carefully consider the potential for a public backlash before finalising policy decisions. A change as substantial as an economy-wide energy transition could pose a considerable threat in that regard. Local communities in southern Algeria protested in 2015 to block government plans for hydraulic fracturing, fearing that this would contaminate critical aquifers. Today, some Algerian environmental justice activists are outspoken in denouncing ‘green colonialism’ across the region – and the alliances of foreign corporations and local elites they see as enabling it. Such arguments could easily gain traction in Algeria, whose citizens have been raised on a revolutionary, anti-colonial ideology and where the authorities repressed but did not resolve the social tensions that led to the Hirak.

Arguments for an accelerated transition

On the other side of the ledger, there are reasons to believe that Algeria only has a limited window to initiate its energy transition. By highlighting these arguments, Europeans may be able to promote a constructive sense of urgency among their Algerian counterparts.

An ideal time to reform

Elected in a contested vote amid the upheaval of the Hirak, Tebboune has struggled to earn popular legitimacy and fulfil his promise of a “new Algeria”. Now in the second half of his five-year term, his administration is focused on making short-term gains to ensure a smooth re-election process in 2024. Today’s surging hydrocarbon revenues give his administration the resources it needs to enact ambitious policies but, true to historical pattern, Algeria’s leaders have instead spent recent months buttressing the current system and postponing plans for reform. The country’s history suggests that, if it delays until energy markets collapse again, it may be too late to make the necessary changes. Despite evidence to the contrary, Algerian leaders claim they are working to avoid that fate and seize the moment – as Arkab did in June 2022, asserting that “we will not make the mistake that we made ten or fifteen years ago. We want to invest the income from gas sales in the energy transition, which is our priority.”

Europe’s commitment to a low-carbon future

Senior EU officials are working hard to prove their commitment to European climate goals. Some leaders in Algiers recognise that taking EU officials at their word could have substantial benefits for Algeria. The REPowerEU plan and related initiatives are channelling considerable resources into such efforts. This level of investment from the EU could unleash the so-called Brussels effect – in which non-EU economies fall into regulatory alignment with the bloc. Once large industries such as automobile production, tech manufacturing, air travel, and others transition to renewable energy, this will leave a dwindling number of clients for Algeria and other major oil and gas producers. By joining this wave of reform now, Algeria could gain early-mover advantages and even help shape the standards, practices, and alliances that may dominate in future global energy markets.

Abundant financing for the energy transition

In the past two decades, Africa received just 2 per cent of global renewables investment. But, in the next few decades, Europe’s new focus on alternative energy sources in its neighbourhood looks certain to change that – in North Africa, at least. For some Algerian officials, this presents a chance that they cannot afford to miss. Others are more sceptical, but they are willing to explore renewables provided that this does not divert resources away from the hydrocarbon sector. By removing this trade-off, outside funding can prove decisive in efforts to win these officials over. The EU is making substantial financing available via, for example, the €300-billion Global Gateway and the European Fund for Sustainable Development Plus, which will guarantee loans for up to €135 billion in foreign infrastructure projects by 2027. The G7’s Partnership for Global Infrastructure and Investment, launched in June 2022 as a counterweight to China’s Belt and Road Initiative, is designed to provide capital for $600 billion in infrastructure development in the next five years. Algeria’s strong bilateral relations with many European countries are another potential source of partnership financing – as are multilateral institutions such as the African Development Bank, the World Bank, and the United Nations. In all these cases, the precise financing terms will have a significant influence on Algeria’s choices, particularly given the country’s traditional aversion to external debt. Finally, Algeria could tap the growing global green bond movement, which holds great promise to attract financing.

Algeria’s long-term economic security

Algeria will eventually need a new source of economic security if projections of declining global oil and gas demand prove accurate in the coming decades. For the reasons discussed above, the country now has a chance to create an economic model with far greater potential than its current one. The development of the renewables sector could also help mitigate Algeria’s unemployment challenge. Some research suggests that every $1m shifted from fossil fuel production to green energy could lead to a net increase of five jobs. According to CEREFE, even Algeria’s nascent green energy sector already employs 2,400 people. One energy think-tank estimates that Algeria could create more than 60,000 jobs by scaling up solar and wind generation in line with its 2030 target.

The energy transition creates an opportunity not just to replace one revenue source with another but improve the competitiveness of Algerian goods. This is particularly true in light of the carbon border adjustment mechanism (CBAM) the EU included in the Fit for 55 package. Scheduled to fully enter into force by 2026, the CBAM imposes carbon penalties on goods produced with fossil fuels as they enter the EU, Algeria’s largest trade partner. As economist Amir Lebdioui argues, “if Algeria doesn’t yet have a solid supply of clean, reliable, and cheap energy [by that point], it could miss out on a wide range of new green industrial opportunities, well beyond the production of energy.”[4]

Hesitation and regional competition

Algeria’s role as a major energy supplier to Europe is not guaranteed to last. “If we don’t position ourselves on the market today, someone else will do it in our place,” energy analyst Tewfik Hasni stated in April 2022. Other countries in the region are currently attempting to do just that. Morocco, which Algeria’s rulers view as their principal rival in North Africa, established a national hydrogen commission in 2019 and published its green hydrogen road map last year. Renewables accounted for 37 per cent of Morocco’s power generation capacity by 2020, when it signed a green energy partnership with Germany. Morocco is now preparing a similar accord with the EU – as is Egypt, which is experiencing an influx of green hydrogen investment as it prepares to host COP27. Gulf countries are making similarly rapid progress. And new road maps and partnerships are proliferating worldwide. Algeria has had its own energy partnership with Germany since 2015, but has taken little action on it. And Algeria has made little effort to learn from global leaders in renewables, such as Australia, Chile, Japan, and South Korea.

The present course

In all, there are compelling arguments on both sides of Algeria’s renewables debate. Some officials view the country as charting a middle path. As Haneche puts it, “there is, in fact, a third way: follow the others but with great prudence.”[5]

He pointed to several of the factors discussed above, while citing the prevailing geopolitical uncertainty – from the outcome of the Russia-Ukraine war to a possible new Iran nuclear deal, to world powers’ reactions to such events – as a further reason why Algerian leaders remain in an observation mode regarding the energy transition. The risk is that, by biding their time amid such rapid changes, external events could determine which path they will take.

Recommendations for Europe

As discussed, the October 2022 discussions between Algeria and the EU could shape the country’s approach to these issues. The talks provide both parties with an opportunity to reach mutually beneficial agreements on energy issues, including the green transition. There is good reason to avoid further delay and push for a comprehensive deal now. As time passes, it will become more difficult to reconcile Algerian leaders’ desire to maintain the status quo with the EU’s stated aim of rapid decarbonisation. And the energy crisis in Europe could shift the bloc’s focus away from this long-term goal. Accordingly, the EU should present its Algerian partners with a carefully sequenced package of incentives to minimise risks and maximise returns in the energy transition.

Establish a partnership of equals

The EU needs to inaugurate a new phase of its energy relationship with Algeria. The leader of the EU delegation, energy commissioner Kadri Simson, was uninvolved in the last Algeria-EU energy dialogue – and is, therefore, well placed to reconfigure the partnership.

It will be important for European negotiators to strike the right tone. As Cinzia Bianco wrote last year in a piece for ECFR on European climate diplomacy in the Gulf, Europeans should help their interlocutors “think of themselves as drivers of green development, not losers trying to survive the transition”.

This may be difficult to achieve if either side overestimates its leverage over the other and abandons its pursuit of a compromise. Algeria knows that it holds vast hydrocarbon reserves at a time when Europe is desperately seeking energy supplies. The EU knows that it is Algeria’s largest trade partner – and that, while Algerian gas exports to the EU amounted in 2021 to 12 per cent of the bloc’s gas imports, they constituted more than three-quarters of Algeria’s gas exports. While both sides hold valuable cards, attempts by either side to strongarm the other would jeopardise a productive long-term partnership.

Coordinate expectations

It is vital that EU member states speak to Algeria with one voice. A lack of effective internal coordination would undermine the credibility of EU representatives’ negotiating positions, perhaps enabling European energy firms to pursue bilateral deals that do not serve the bloc’s interests. In this scenario, Algerian officials might view EU member states as willing to compete in a race to the bottom in standards, undercutting long-term European objectives – as threatened to occur earlier this year, when Spain and Italy briefly appeared to approach a bidding war for Algerian gas supplies. The EU should use revisions to its Renewable Energy Directive or other mechanisms to ensure that its member states pursue their energy goals together.

The EU needs such coordination to end Algeria’s uncertainty about the mix and quantity of the bloc’s future energy demand. Algerian officials complain that the EU’s and its member states’ history of revising their energy priorities without consulting or even informing their partners has damaged their credibility, reinforcing the impression that they view the relationship as one between a supplier and a client rather than a true partnership.

Europeans should make greater efforts to compile and transparently share future projections – or, better yet, future commitments – of long-term energy demand. By clearly expressing their future energy needs, they will give advocates of the energy transition in Algeria an invaluable tool to combat delaying tactics within key institutions. By providing advance contracts for long-term renewable energy purchases, Europeans could reduce Algerian officials’ hesitancy, help them attract international investment for renewables projects and infrastructure, and prepare a road map for the energy sector, including the green transition.

The EU Energy Platform – a voluntary mechanism for collective energy purchases established in April 2022 under REPowerEU (and open to certain European countries outside the bloc) – could serve as a forum for pooling projections of energy demand and then issuing long-term power purchase agreements. This form of centralisation would reduce the risk for all participants.

Reduce the pressure to overextend gas purchases

Europeans expect that, even in the best-case scenario, they will need fossil fuel imports for several decades to come. So, it would be unrealistic for them to completely cut off investment in oil and gas exploration and production. Algeria and powerful corporations in Europe have a vested interest in extending such investments – as they have continued to do in recent months. Alongside US firm Occidental Petroleum, Eni and French company TotalEnergies committed in July 2022 to a $4-billion, 25-year investment in Algeria’s Berkine Basin.

Given the severity of the energy crisis in Europe, Algeria will enter negotiations confident of its ability to compel Europeans to invest considerable sums in gas production in exchange for expanded, or merely sustained, supply. EU officials should remain cognizant of the fact that Algeria is currently producing at the limits of its capacity and has already committed much of that production to European buyers through long-term contracts. They should also remember that any new investment agreed is unlikely to increase output until next year at the earliest. Therefore, no amount of investment in traditional gas production in Algeria will ease Europe’s energy crunch this winter.

However, measures to reduce gas wastage could have benefits in a matter of months, particularly if they were supported by European funding, equipment, and expertise. The capture of gas that would otherwise be wasted through flaring, venting, and leaks would have immediate environmental benefits and could harvest as much as 13.5 billion cubic metres of the product annually, the equivalent of more than 10 per cent of Algeria’s output last year. The EU and Algeria should include an effort to tackle such problems in any deal they sign, as it would have benefits for both parties.

More broadly, Europeans should carefully weigh the risks of investments in Algerian gas production. Algerian officials will interpret any investment in fossil fuels as a confirmation of the long-term viability of their economic model, raising their expectations of further commitments and directly reducing their incentives to commit to the energy transition. European investment also risks developing assets that the EU may not need in the coming decades, as Algeria’s renewables sector frees up more gas for export and the EU reduces its fossil fuel imports. Accordingly, such investment risks creating stranded assets or, more likely, developing assets that only benefit other buyers.

Prioritise local needs

As discussed, Algeria’s priority in the development of its renewables sector is to meet domestic power demand first, freeing up more hydrocarbons for export. Given this consideration and Algeria’s track record of cautious change, the country will almost certainly not develop export-oriented renewables in time to contribute to Europe’s 2030 energy import goals.

In this context, Europe should help Algeria launch its energy transition in earnest through a two-stage plan. With Tebboune up for re-election in 2024, his administration will welcome projects that it can point to as evidence of progress and modernisation (even if the benefits for citizens are not immediately tangible). Quick wins of this kind, implemented with European technical and financial support, would help generate goodwill with the Algerian government. Such initiatives could include the rapid construction of pilot solar PV and wind installations, energy efficiency initiatives that benefit from European expertise and equipment, and training courses or educational exchanges to build expertise in the renewables sector.

Europe should help Algeria establish a scalable plan for the development of renewables projects to offset domestic power consumption. Such initiatives could involve the construction of solar PV and wind installations – and perhaps even solar CSP stations, whose greater cost might be offset by their capacity to continue providing power for several hours after sunset. Given its abundance of expertise in this domain, Europe would be well placed to provide technical support to Algeria as it defined and implemented its renewables strategy, including in the critical choices over the desired energy mix and technology selection. European financing will be essential to facilitating this process, particularly in overcoming initial public scepticism about its value.

Europe should also provide support for auxiliary projects such as electrical-grid upgrades, the installation of smart grid management systems and smart meters, and the rollout of net metering – all of which would facilitate the widespread adoption of private renewable generation. Europe could also help Algeria explore ways to exploit low-cost energy to expand industrial activity, opening up a new area of potential public-private collaboration between the sides and creating opportunities for pilot projects involving green hydrogen.

Policy frameworks are another potential area of assistance. Europeans could provide advice to Algerian policymakers about how to improve the investment climate by aligning the terms of public tenders and power purchase agreements with international best practices – expanding on the work they have begun as part of a joint cooperation project. Algeria could also benefit from European assistance in establishing carbon markets as the CBAM goes into effect, and in overhauling energy subsidies to adapt consumer incentives to the green transition.

Once Algeria’s renewable energy sector is on its way to covering a significant portion of local power demand, Europeans should help the country develop low-carbon energy for export. This phase will require an even greater scale of deployment, making it all but certain that Algeria will look to Europe for investment.

Europe should provide expertise that can help Algerian leaders make critical choices about technological development – both for large-scale power generation and for transport to Europe. Given the scale of projects in these areas, Algerian leaders will be particularly reluctant to invest in unproven technologies. It will be up to Europeans to demonstrate the advantages of green hydrogen or to propose an alternative form of renewable energy exports.

Invest in Algerians

The EU should offer to help Algeria establish specialised universities (following a model already in place in the tourism and hospitality sector), vocational training centres, and other educational partnerships to train the workforce needed to sustain a thriving nationwide renewable energy sector. To help reduce backlash against this sector and smoothly integrate workers transitioning from the fossil fuel industry, the EU should support retraining programmes.

As the relationship between Algeria’s government and citizens is strained, the EU should seek to help the sides avoid confrontation over the transition to renewable energy. Europeans can head off accusations of green colonialism by recruiting employees from local communities near project sites and financing projects there that offset the negative side-effects of new energy installations. It would be worthwhile to explore initiatives that could benefit these communities, such as agrivoltaic projects. Firms operating in Algeria’s oil and gas sector are not required to commit a share of their profits to corporate social responsibility or community welfare spending.[6] As a result, few choose to do so. This contributes to resentment in communities near many energy production sites. The EU should help Algeria avoid repeating this mistake as it transitions to new forms of energy production. For example, Brussels could set minimum requirements for European energy firms that operate in Algeria to support local communities.

Conclusion

Europeans should be realistic in their expectations of the pace and nature of the change Algerians are seeking in the energy sector, a domain they view as central to national security. The partnership between the sides will never be exclusive: Algeria will continue to cultivate its ties with geopolitical rivals of the EU, such as Russia and China, in its energy transition. But this need not hinder cooperation between the EU and Algeria to achieve their energy goals.

Europeans can achieve much by remaining sensitive to their Algerian partners’ needs, helping them to resolve their problems, and focusing on areas of mutual interest. In doing so, the EU can make progress towards meeting its own energy security goals while helping Algeria find a sustainable path to prosperity. A robust energy transition in Algeria would still leave many of the country’s challenges unresolved. But effective cooperation in this domain could help rebuild trust between the sides, creating new opportunities for Europe to engage with Algeria in other domains.

About the author

Andrew Farrand is a visiting fellow with the Middle East and North Africa programme at the European Council on Foreign Relations. He is also a non-resident senior fellow at the Atlantic Council. He is the author of “The Algerian Dream: Youth and the Quest for Dignity” (2021), a first-person analysis of the origins and implications of Algeria’s 2019 Hirak revolution, and translator of “Inside the Battle of Algiers” (2017) by Algerian independence heroine Zohra Drif. He lived in Algeria from 2013 to 2020, working in a variety of roles in international development and economic and political analysis. Farrand holds a BS in African and Middle Eastern Studies from Georgetown University’s School of Foreign Service.

Acknowledgments

The author is profoundly grateful to the officials and policy experts who generously shared their time and insights in the research for this paper, including Mohammed Haneche, Faten Aggad, Reda Amrani, and Amir Lebdioui. The author wishes to thank his ECFR colleagues Julien Barnes-Dacey, Anthony Dworkin, Hugh Lovatt, Jeremy Shapiro, and Edin Dedovic for editing support and other valuable guidance in preparing this paper. Any mistakes are the author’s alone.

This paper was made possible by support for ECFR’s Middle East and North Africa programme from Fondazione Compagnia di San Paolo.

[1] Author’s interview with Faten Aggad, September 2022.

[2] Author’s discussions with an Algerian energy analyst, August 2022.

[3] Author’s interview with Mohammed Haneche, August 2022.

[4] Author’s interview with Amir Lebdioui, August 2022.

[5] Author’s interview with Mohammed Haneche, August 2022.

[6] Author’s discussions with an Algerian energy analyst, August 2022.

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.