Tricks of the trade: Strengthening EU-African cooperation on trade in services

Summary

- Services are increasingly important for international trade, accounting for about half of global trade flows. Trade in services is growing more rapidly than trade in goods.

- Trade in services is critical for improving the competitiveness of African economies, increasing their participation in regional and global value chains, and promoting inclusive growth.

- Improved trade in services with African countries could help the EU diversify its supply chains, strengthening resilience and reducing dependencies on China and other Asian countries.

- The cooperation on domestic regulatory frameworks required for trade in services can promote a shared understanding of regulatory goals and standards between the EU and Africa across many sectors.

- None of the trade agreements between the EU and African countries currently covers services, and only one African country is part of the WTO Joint Initiative on Domestic Services Regulation. There is therefore no dedicated platform for cooperation on services regulations.

- The African Continental Free Trade Area agreement provides an unprecedented opportunity for African countries to improve domestic services regulations and could be a new basis for cooperation with the EU.

Introduction

Despite the growing importance of services in the global economy, Europe’s trade cooperation with Africa is almost exclusively focused on commodities and other primary goods. Services – which range from banking and insurance to transport – are largely missing from Europe’s trade and development cooperation agenda with Africa. Yet the services sector has outstripped the primary and secondary sectors in their contribution to African output, making up more than half of the continent’s gross domestic product (GDP). The rapid expansion of information and communication technology (ICT) and the digital economy, the ‘servicification’ of manufacturing, and the cross-border fragmentation of production processes make trade in services more important than ever before for industrialisation and integration processes.

Services not only enhance participation in trade and global supply chains, they also contribute to more equal and diversified growth. More women, young people, and micro enterprises operate in the services sector than in agriculture or manufacturing. Expanding opportunities in services is therefore particularly important for creating more inclusive employment. The high costs of energy, transport, logistics, and other backbone services across Africa make the production of goods and services expensive, impeding the competitiveness of firms across all sectors. Trade in services is a powerful tool to increase the efficiency and reliability of services, which in turn brings down production costs across the economy and facilitates diversification – and its importance goes beyond trade to offer possibilities for structural transformation.

A stronger services trade between the European Union and Africa would allow European multinationals to near-shore their production processes and diversify away from Asia-focused supply networks. As barriers to trade in services are embedded in domestic regulations, trade agreements covering services entail a degree of cooperation and shared understanding. Improved trade in services would also allow the EU to influence regulatory models across various sectors. China and other non-Western powers wield significant economic influence in Africa, which they can use to shape regulatory processes and influence standards in their favour. Faced with geopolitical competition with China, the EU should be wary of this influence. In this regard, trade cooperation on services could be a powerful means for the EU to nurture a shared understanding with African countries on economic, environmental, digital, and social goals.

No modern trade partnership can exclude services, which are central to the value of what businesses trade. While the so-called first-generation free trade agreements reached in the 1970s and 1980s only liberalised and addressed standards in the goods trade, services became an integral part of the ‘new generation’ agreements that emerged in the mid-1990s. These new agreements included goals for so-called deep integration, which covers a variety of issues beyond tariffs, including services, investment, competition, intellectual property rights, environmental standards, and other domestic policies that affect international competitiveness. More than 90 per cent of all free trade agreements signed in the 21st century cover services, making it the most widespread area of deep integration.

The 2018 African Continental Free Trade Area (AfCFTA) agreement includes a protocol on trade in services, which aims to liberalise services markets and improve their domestic regulation. The agreement provides an unprecedented opportunity for African countries to strengthen their domestic regulations to support more open and efficient services markets. It also offers an occasion for the EU to encourage intra-regional trade by supporting the AfCFTA negotiations, and to build on the agreement to create new opportunities for diversifying EU-Africa trade.

This paper explores the implications of cooperation on trade in services for the Europe-Africa relationship. The first section sets out the complex nature of the services trade and addresses misconceptions around it. The second section analyses the importance of the services trade for the industrialisation and integration objectives set out in the African Union’s (AU) Agenda 2063. The third section discusses the EU-Africa trade relationship, including the benefits for Europe of a more efficient African services sector and the existing obstacles and policy frameworks that govern services trade between the EU and Africa. The fourth section explains how the AfCFTA offers new opportunities for promoting more open and effective regulation of services markets. The paper concludes with recommendations for how Europe and Africa can enhance their cooperation on trade in services.

Trade in services: From oxymoron to opportunity

Traditionally, policymakers did not consider services as something that could be traded across international borders. As a result, governments have often focused their foreign trade strategies on agricultural and industrial goods. Yet the world has changed enormously, and technological and regulatory developments have made a growing range of services tradable across the world. From call centre operators to cloud computing, internationally traded services continue to emerge and expand.

For many years, services accounted for a small but stable share of global trade. But in the past decade, data that measures services in value-added terms have shown that they account for over 50 per cent of the value added in gross exports. This data only covers cross-border supply trade, and does not fully account for digitally enabled services, which are difficult to capture. Meanwhile, services account for over two-thirds of global foreign direct investment (FDI).

Services are also critical for the production of all goods in the economy, including in agriculture and manufacturing. The role of services as an input into consumer and capital goods is substantial, both in developed and in developing countries. A study by the OECD found that between 25 per cent and 60 per cent of employment in manufacturing firms is attributed to service functions, including research and development (R&D), engineering, transport, and logistics. The OECD database on trade in value added shows that services represent 30 per cent of the value added in exports of manufacturing goods. The total value added has been growing over time, as manufacturing companies increase the use, production, and exports of services. Given that goods and services are intertwined, increasing the efficiency of services improves the competitiveness of the overall economy.

In modern manufactured goods, much of the value added is created in the early stages of R&D, design, and commercialisation as the product is being conceived, and in the late stages of marketing, logistics, and after-sales services once production is complete. Countries that do not offer high-quality services relevant to the international production process are often confined to the assembly of goods, in which productivity growth tends to be lower. By improving the competitiveness of these services, a country can increase its prospects to improve its position in a regional or global value chain and capture activities with greater value added in the international production chain.

Services only appeared in international trade policy when the World Trade Organization (WTO) was established in 1995. Before that, countries’ trade relations were governed by the 1947 General Agreement on Tariffs and Trade, which only covered trade in industrial goods. The Uruguay round of multilateral talks on trade liberalisation (1986-1994) – which established the WTO – also led to the creation of an analogous instrument for trade in services: the General Agreement on Trade in Services (GATS). This agreement was part of the so-called great bargain of the negotiations, in which developing countries accepted the agreements on services and intellectual property rights – in which they saw few benefits for themselves – in exchange for ones covering two sectors of interest to them: agriculture and textiles.

The GATS classifies trade in services by the way they are delivered, known as “modes of supply”:

- Cross-border supply: The consumer and the service supplier remain in their respective countries. The service is transmitted online, or by telephone, email, or post. This mode includes digitally enabled services.

- Consumption abroad: The consumer travels to another country to obtain a service. Classic examples are tourism and courses for foreign students.

- Commercial presence:A company establishes a presence in another country to provide services to foreign consumers. This mode essentially refers to FDI in sectors such as banking, transport, and energy.

- Presence of natural persons: A supplier, such as an architect, nurse, or musician, travels to a foreign country to provide a service. The supplier remains temporarily (for a number of months or years) in the country, and does not obtain residency, citizenship, or permanent employment.

Unlike trade in goods, trade in services does not have tariffs, but is instead restricted by domestic regulations, which often apply equally to domestic and foreign actors. Services markets tend to be highly regulated, much more so than those for goods, hampering the potential for trade. Trade partnerships on services therefore require regulatory cooperation mechanisms that promote greater convergence or compatibility across domestic regulatory frameworks, from licensing procedures to mutual recognition of professionals.

These regulations are intertwined with a broad range of domestic policies that, though not motivated by trade protectionism, significantly affect trade. For example, regulations related to shipping and port services are often deeply rooted in national security, territorial, and other geopolitical factors, but they have become critical in modern services trade negotiations due to their importance for facilitating global value chains. Similarly, trade in services depends on the movement of service providers across borders, which is limited by migration and labour policies. The geopolitics around issues such as climate change and clean energy, technology and digitalisation, and cultural or indigenous promotion have also been acquiring growing importance in services trade negotiations. This complicates trade negotiations, which necessitate agreements around other policies. Yet it also means that the commitments made on these issues with regards to trade in services can significantly shape broader geopolitical relations. Cooperation between the EU and Africa in services trade negotiations could therefore promote understanding on a wide range of policies, deepening EU-Africa relations more broadly.

Africa’s services trade

The potential of trade in services for African countries

Many policymakers still see trade in services as the preserve of high-income countries and do not consider developing countries as having a comparative advantage in exporting services beyond tourism. But the trading landscape has changed significantly over the past two and a half decades, providing more opportunities to participate in trade in services. The increasing fragmentation of production processes – with different stages carried out in different countries – has generated fresh opportunities for countries to specialise in and export particular tasks, for example, marketing, logistics, or legal services, making it easier for companies in developing countries that cannot produce an entire product to participate in trade.

African countries should have a special interest in promoting an agenda for services trade. The sector provides opportunities for international research collaboration, and for young people to pursue education and work abroad – both of which are key for knowledge-oriented societies. Trade in services also offers possibilities to improve the reliability of transport and logistics; to expand the digital economy; and to exploit Africa’s comparative advantage in renewable energy. These sectors are key to African economies, and African governments should therefore not overlook the role of trade in services in strengthening them.

Trade in services also promotes inclusive economic growth. Unlike trade in commodities or manufacturing – which entails significant transport costs and cumbersome customs procedures – services can be traded across borders at lower costs. Services are also increasingly traded digitally, removing the need for transport and its complexities altogether. This enables smaller-scale traders, including micro enterprises and entrepreneurs, to import and export services from distant markets. Given that the services sector has a particularly high concentration of small and medium-sized enterprises, boosting their trade can induce economic growth at all levels.

African countries have untapped opportunities to trade services. Although data show that Africa’s exports of cross-border services make up just 2 per cent of the global total, this does not account for the value added to goods by services, which, as mentioned above, is substantial. Moreover, the fact that Africa’s exports of services have been growing relatively quickly in recent years suggests that the continent has a growing comparative advantage in trading services. Case study evidence also suggests that a significant part of the dynamism in Africa’s services exports is due to intra-regional trade.

Leveraging services trade for Africa’s economic transformation

The AU’s Agenda 2063 sets out a number of goals to transform Africa into a dominant global player, prioritising inclusive social and economic development, continental and regional integration, and democratic and security goals. The AfCFTA aims to boost the levels of intra-regional trade in Africa, and further diversify and increase the sophistication of traded products. This prioritisation of regional and continental integration above global trade is driven by the fact that African countries already trade an increasingly diversified and high value-added set of goods with one another.

Meanwhile, African exports to the EU remain largely concentrated in primary goods, including food and drink, raw materials, and energy, with most processing and value addition performed abroad. African countries are also not well integrated into global value chains, where they generally perform lower value-added tasks, such as the assembly of different parts. Services are high value-added activities, so making them more competitive and increasing their trade will help improve the position of African countries in both regional and global value chains. In addition, the lower sunk costs of intra-African trade – in part due to lower standards and greater knowledge of neighbouring markets – means that a greater number of African companies can export processed goods within the region, whereas only the most productive can export to the EU.

However, in the long run, Africa’s growth can best be supported by trade beyond the continent. New types of exports need to acquire scale, which would be challenging to achieve solely within African markets. Furthermore, the opportunities for technology transfers from trade, FDI, and strategic partnerships are typically greater with firms located in more advanced economies, such as those in the EU. African countries experience several common challenges in their efforts to boost trade with the region and beyond, which trade in services can either alleviate or avoid.

- Distance to markets and border friction: High transport costs in the region, especially between Regional Economic Communities, and customs ‘red tape’ are key impediments to Africa’s trade competitiveness. These costs are largely reduced or eliminated in services trade.

- Supply chain constraints: Many African companies and countries are not able to take full advantage of new market access opportunities, intra- or extra-regionally, due to supply side constraints. Improved services would lessen these supply bottlenecks, both in terms of human and physical capital. Services trade notably addresses ‘soft’ infrastructure – the regulation of services that operate on the ‘hard’ physical infrastructure platforms. For example, the economic activity that a port or airport generates is not solely determined by the physical infrastructure, but by open regulations that allow private and foreign shipping, logistics, and airline service providers to operate. This is less straightforward to address than hard infrastructure issues, but equally important.

- Lack of value addition: Many African agricultural exports – from cocoa to cotton to cashews – are exported raw to global markets. The domestic processing industries that do exist are often hampered by costly and ineffective services and high subsidies, create little employment, and struggle to add value. Services make up a significant share of the value added by processing primary goods, making the end product more competitive.

- Limited expansion of regional value chains: Africa is the region with the lowest degree of integration in global value chains, with integration largely limited to South Africa, and a few countries in North Africa. Governments have promoted the creation and expansion of regional value chains, but these remain short, with difficulties scaling up. The operation of cross-border value chains is highly sensitive to the cost and reliability of transport, logistics, distribution, and a range of other services. Regional value chains suffer even more from these factors, as companies are typically smaller than in global networks and less able to absorb costs related to inefficient and unreliable services. Improving these services would allow regional and global value chains to scale up.

Trade in services can therefore play an important role in improving the integration of African countries, regionally and with external partners. The growing middle class, increasing use of technology, and rapid urbanisation all contribute to the rising importance of service sectors. As African countries develop, and a growing share of their GDP is driven by services, diversification into service exports, particularly those that can be traded digitally, will be critical to maintain growth rates.

EU-Africa trade in services

Despite the rising importance of services, the EU and Africa have not been able to integrate services in any of their bilateral trade relationships. Similarly, the Aid-for-Trade initiative – a WTO scheme through which the EU and others channel trade-related technical assistance and capacity building to developing countries – focuses largely on the goods trade. Globally, nine out of ten bilateral or regional trade agreements (RTAs) signed since 2000 address the liberalisation of services and domestic regulations. The EU covers services in its bilateral arrangements with other trading partners, as well as in a number of trade agreements with developing regions, including the Economic Partnership Agreements with the Caribbean and with Central America. Although most recent bilateral agreements between the EU and African countries include provisions to negotiate services in the future, this has been difficult to put into practice. The two regions need fresh approaches to cooperation in order to modernise and diversify their trade relationship and increase its economic impact.

Mutually beneficial trade

Enhanced trade in services with Africa would also benefit the EU. Many European countries are net exporters of services, and European companies want to expand their presence in Africa in sectors that currently have high barriers to trade and FDI, such as commercial banking. Addressing Africa’s deficiencies in services such as transport, logistics, and distribution could help European multinationals to diversify their trade strategies, making them more competitive and resilient.

Trade in services does not carry the same risks for trading partners as trade in goods. Liberalising the goods trade in a bilateral or regional agreement often diverts trade away from more efficient third-party suppliers. By deepening their trade relationship in agriculture and primary goods, both the EU and Africa risk reducing trade with more efficient suppliers in other regions, such as Asia, north America, or Latin America. In contrast, trade liberalisation in services entails domestic regulatory reform, which often applies to all trading partners as it is not practical to maintain different domestic regulations for different partners. This limits the risks of diverting trade away from other partners and allows countries to maintain beneficial trading relationships with various partners. Trade in services therefore provides an opportunity for the EU to deepen its trade relationship with Africa, without jeopardising trade with other partners.

Trade agreements that include services not only have greater trade-boosting effects than those that only liberalise goods, they also affect the location of global value chains. The covid-19 crisis has intensified efforts from businesses and policymakers in the EU to diversify and near-shore global value chains, and to balance efficiency with resilience. Supply security vulnerabilities and dependencies on particular trading partners also have geopolitical ramifications, weakening the EU’s ability to act autonomously. Intensified geopolitical competition with China has also increased the EU’s desire to diversify away from its traditional partners in Asia. Open services markets in Africa would help Europe support both the security of its key supply chains and its autonomy. European companies would benefit from locating value chains in African countries too, given the geographical proximity of and lower production costs in Africa.

The EU and Africa have the potential to be natural trading partners in direct services. Trade in services is highly sensitive to factors that impede people-to-people contact, such as language barriers; differences in time zones; and cultural, historical, and institutional divides. Conversely, trade in services largely avoids the costs of distance and crossing borders, such as transport, customs, and complex rules of origin. Africa and the EU share similar time zones and some of the same languages. In addition, some of the regulatory frameworks and institutions in African countries have been modelled on European legal and institutional systems. The two continents therefore have relatively few of the common obstacles to trading services to contend with.

Existing obstacles

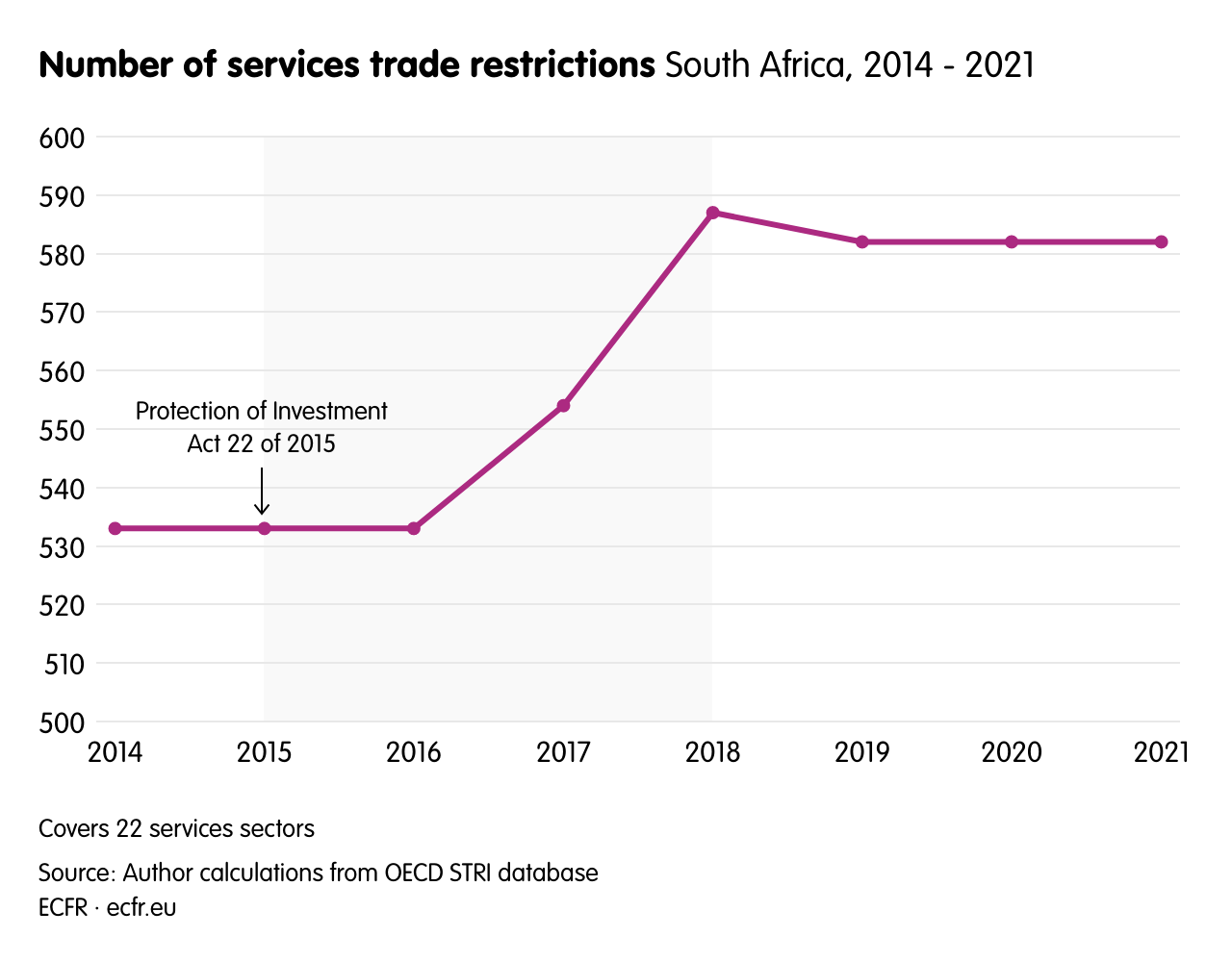

There is a lack of systematic and comprehensive information on barriers to trade in services across Africa, but the available data suggest that these are high. For example, an OECD index (covering 38 OECD countries and seven emerging economies) that measures policy restrictions in services finds that South Africa – the only African country covered – is more restrictive than the average EU, OECD, and emerging market economy covered in 15 of 22 service sectors. Over the years, new legislation passed in South Africa – where services represent 60 per cent of GDP and 70 per cent of employment – has increased the regulatory restrictions. Key sectors such as commercial banking, cargo-handling, and courier services have higher than average policy restrictions. On the other hand, South African policies in a few sectors, such as road freight transport, legal, and accounting services are closely aligned with those in advanced OECD countries and large emerging economies.

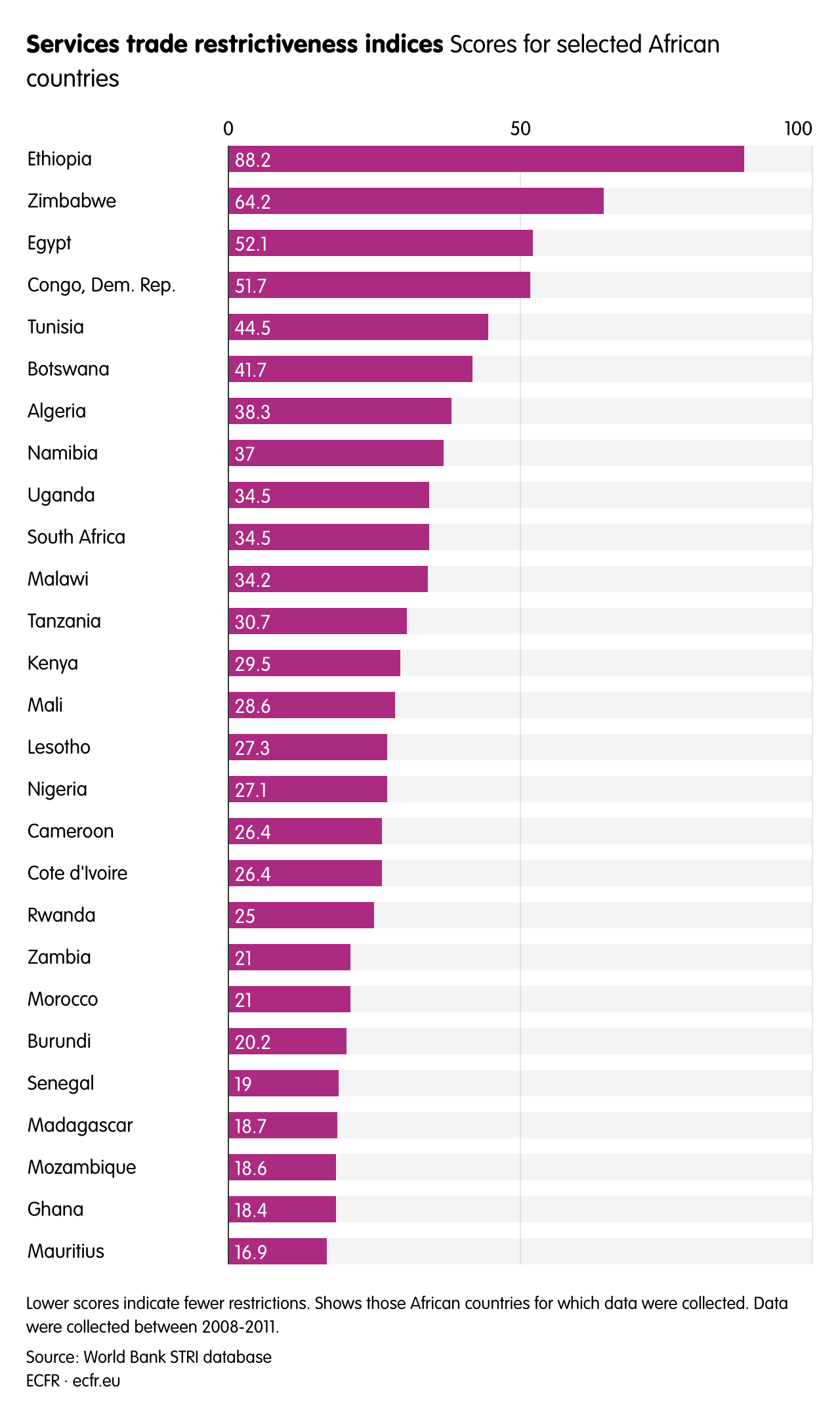

A 2010 World Bank index for 27 African countries, based on 2008 information, found great variation in the barriers to trade in services across African countries, ranging from Mauritius as the most liberal to Ethiopia as the most restrictive. However, the index only tracks regulations on services that explicitly discriminate against foreign services suppliers, while the problem for trade in services in many African countries is the absence of a regulatory framework. As a result, some countries that appear relatively liberal in this area in fact lack regulation, leaving decisions on whether foreigners can operate in the country to ministerial discretion.

Breaking down the barriers

In the absence of a bilateral agreement covering services, the trade relationship between the EU and African countries is governed by the GATS. However, when the GATS was concluded, most African countries were not interested in committing to comprehensive liberalisation in service sectors. There has been little substantive global liberalisation in services since, with the exceptions of financial services and ICT – for which WTO members concluded negotiations after finalising the GATS. In 2010, 70 countries attempted to conduct wider services liberalisation through an agreement on trade in services, but only one African country – Mauritius – participated in these negotiations, which were never concluded.

In December 2021, 70 countries – including all EU and other major European countries – concluded the first successful global services trade cooperation pact since the GATS: the Joint Initiative on Domestic Regulation. The agreement does not address market access, but participants commit to improving domestic regulation of services and to streamlining procedures such as certification and licensing. Only two African countries – Nigeria and Mauritius – are currently parties to the agreement. But, because participants have agreed to implement these commitments for all their trading partners, there will be export benefits for all African countries. In particular, they will benefit from more transparent and streamlined procedures for exporting services. Moreover, African countries can join the agreement if they wish, and there is a mechanism for least-developed countries (LDCs) to modify their commitments according to their capacities.

In June 2022, WTO members committed to reinvigorating efforts to operationalise a waiver that allows governments to grant more favourable services market access to LDCs. The LDCs ‘services waiver’, created in 2015, is similar to the duty-free and quota-free market access for goods given to LDCs under the WTO enabling clause. Unfortunately, implementation has been limited and ineffective. The waiver also has limitations: trade-related restrictions are higher on services than on goods in EU and other OECD countries, and have been rising in recent years in many sectors, including digital-related sectors. Moreover, because the liberalisation that is taking place multilaterally and in RTAs on services has been limited, the potential for trade preferences is more significant. In the case of goods, tariff preferences obtained in RTAs have been largely eroded as the level of tariffs has come down through WTO negotiations and more RTAs liberalising goods have been concluded. The waiver is also limited to LDCs, and so would only apply to 32 African countries. A similar waiver on goods has been in place for LDCs for decades, and it has arguably failed to substantially increase their participation in world trade.

Many of the impediments to trade in services are embedded in non-discriminatory domestic regulations. In practice, it is difficult to convince regulators to accord preferential waivers. In addition, trade in a service often requires several different modes of supply, which may face different degrees of regulation. For example, granting market access to allow a business to establish a commercial presence in a country without granting market access on the movement of persons means that a business would be allowed to invest abroad but would not be able to move its personnel. Given that multiple modes often co-exist, waivers are ineffective if they are limited to certain modes.

Liberalising services through the AfCFTA

EU and African policymakers should engage in renewed efforts to facilitate trade in services between the EU and Africa. The AfCFTA provides a unique opportunity for them to do so. The agreement is often hailed for its size and far-reaching tariff-free regime, but the liberalisation of trade in services is one of its most important features. Its protocol on trade in services is the continent’s first broad effort to liberalise trade in services and improve the domestic regulation of key services sectors. The protocol provides a framework, and actual liberalisation is taking place through subsequent negotiations.

The 54 countries that have ratified the AfCFTA to date have agreed on liberalising five priority services – financial, communication, transport, tourism, and business services – and are currently engaging in negotiations to make specific-sector commitments. This process was supposed to be completed by June 2022, but at the time of writing (January 2023) negotiations had not concluded, and the schedules of specific commitments were not publicly available. As a result, it is impossible to assess the extent of liberalisation to trade in services under the AfCFTA. However, the AfCFTA agreement has several advantages which can aid the process of liberalisation.

The negotiations are using a positive list approach (the so-called GATS approach), which is sometimes perceived as a less effective means of liberalisation than a negative list (the so-called North American Free-Trade Agreement approach). A positive list indicates all the sectors and measures that are being liberalised, whereas a negative list indicates the sectors and measures that are exempted from liberalisation (thereby liberalising all sectors or measures that are not listed). The same degree of liberalisation can be achieved through either approach. It is understandable and perhaps advisable that countries with limited administrative capacities adopt a positive list approach, which does not require internal consultation concerning all service sectors of the economy – just those in which there is a decision to liberalise. Moreover, the GATS followed a positive list approach, and using the same approach facilitates synergies between regional and multilateral negotiations.

A key difference between the AfCFTA services protocol and the GATS is the treatment of commitments by LDCs. Unlike the GATS framework and LDCs waiver – in which LDCs are not required to make any substantive liberalisation commitments – in the AfCFTA, any differential treatment is considered on a case-by-case basis. This encourages all countries regardless of their level of development to liberalise services and strengthen their domestic regulatory frameworks, which in turn allows them to be more competitive in exports. This departure from an LDC-centred form of special and differential treatment can provide inspiration for new approaches of engagement in the WTO and other trade partnerships between developed and developing countries.

There are open questions about the effectiveness of the AfCFTA in facilitating domestic reforms. Yet, given the difficulty of passing reforms at the domestic level, it is hard to imagine that such reforms would more readily take place without an external anchor. It is very difficult to change shipping, ports, and logistics regulations that are embedded in maritime and ports laws which often date back to or predate countries’ independence, and which are grounded in national security motives. A major RTA such as the AfCFTA provides governments with an external mandate to review and modernise these laws and generates peer pressure as other African countries pass reforms and gain the benefits from doing so. It also provides incentives for the less appealing measures (for example, visas for temporary study and work abroad in exchange for resisted changes in transport services or warehousing regulations) and avoids policy reversals when governments or regulators change. Furthermore, it often brings external technical assistance and capacity building to implement reforms. With sustained political commitment and strengthened implementation capacity, the AfCFTA creates important incentives and momentum for reform. The EU can support this process further by providing capacity building and technical assistance on these issues.

Finally, the AfCFTA covers disciplines that are closely related to services, including investment, competition policy, intellectual property rights, digital trade, and e-commerce. Negotiations around policies in these sectors should have mutually reinforcing effects with those around trade in services, as they also facilitate the operation of regional and global value chains. These negotiations also provide an opportunity to promote international good practices from existing deep international agreements and a shared understanding across a variety of sectors. Eventually, the agreement aims to create a single market for goods, services, and capital, and to enable the free movement of people within the region.

Conclusions and recommendations

Facilitating trade in services is key to ensuring that the EU-Africa trade partnership is comprehensive, forward-looking, and mutually beneficial. As technology blurs the lines between goods and services, a shallow trade partnership that addresses goods alone is no longer grounded in the reality of modern business and offers limited prospects for a dynamic trade partnership in the 21st century.

Services are not just the fastest-growing component of international trade, they are also critical to the competitiveness of other exports, including industrial goods. Services are therefore essential to diversify the EU-Africa trade relationship, which remains excessively concentrated on commodities and other primary goods. In addition, efficient and reliable services are vital for the operation of global value chains and for the investments of multinationals across Africa.

Unlike goods, barriers to trade in services do not take the form of tariffs and other traditional trade barriers, but are more commonly embedded in domestic regulations. For this reason, the degree of regulatory alignment across countries is critical for opportunities for trade in services. This does not mean that countries need to strive to have identical regulations, but their differences in regulations need to be transparent and as compatible as possible.

The extent to which Africa and the EU adopt similar policy stances with respect to the regulation of services markets will influence the growth of bilateral trade partnerships between the regions. Yet, its importance goes well beyond trade. Trade in services and cooperation on domestic policy go hand-in-hand. For example, the stances that Africa takes in its regulatory frameworks with respect to data policy – including privacy, security, and access issues – will determine the ease with which companies from both continents can trade digitally enabled services that are vital for doing business across borders in virtually all modern sectors of the economy. Indeed, services trade negotiations are not just about removing barriers to trade, but about creating shared regulatory models and processes across countries.

Beyond that, the regulatory choices that Africa makes in these trade negotiations will advance or limit the EU’s capacity to be a global standard-setter. This is particularly important with regard to the EU’s intensifying geopolitical competition with China. The latter has become a key political and economic power in Africa, with the ability to influence the development of regulations and standards. By strengthening trade relations with Africa, the EU can counter this influence and promote good practices in line with its environmental, social, and digital goals. Open services markets in Africa also provide the opportunity for European companies to near-shore global value chains, reducing their dependency on China and other Asian countries, and promoting European resilience. In this way, tighter EU-Africa trade relations provide both economic and geopolitical benefits.

As African countries conclude services liberalisation commitments under the AfCFTA and initiate negotiations on the digital economy, the EU and Africa need to explore deeper cooperation on services, including in digitally enabled services. In particular, EU and African governments and officials – at both state and regional level – should consider several avenues for cooperation on the implementation and expansion of the continental services agenda under the AfCFTA.

Strengthen the data on Africa’s services trade

As the old saying goes, what cannot be measured cannot be managed. The EU and the AU should cooperate to strengthen the data on Africa’s services trade, leveraging EU expertise and cooperating with relevant African institutions like the United Nations Economic Commission for Africa. Reliable information on the contribution of services to the added value in all sectors, that is comparable across countries, would help governments to design better industrialisation and trade strategies.

Promote regulatory transparency and cooperation between Africa and the EU

Barriers to trade in services can be difficult to identify without comprehensive data on regulations across sectors. The OECD, World Bank, and WTO have created databases and indices on services regulations and their impact on trade, but coverage of African countries has been limited and not kept up to date. Better-quality information would help EU and African countries to identify measures that could form the basis for bilateral cooperation and promote dialogue between regulators and trade officials of both continents on good regulatory practices.

Exploit synergies between the AfCFTA and multilateral initiatives on services

The EU should work towards operationalising its LDCs services waiver in light of the outcome of the services negotiations under the AfCFTA. The services waiver and the AfCFTA’s specific commitments could be mutually reinforcing if they align sectors and modes of supply. Moreover, the EU should consider WTO-compatible ways of enabling non-LDC AfCFTA countries to benefit from the same market access, including through bilateral arrangements. Finally, the AfCFTA should be used as a stepping stone for greater participation of African countries in the Joint Initiative on Domestic Services Regulation under the WTO.

Experiment with non-traditional, light institutional structures

Pursuing cooperation on trade in services will require a pragmatic approach. Both the EU and Africa have adopted heavy, formal, and institutional trade policies. The AfCFTA’s lack of teeth may therefore be regarded as a weakness, particularly when compared to the powers of European institutions in trade policy. Yet, the experiences of other regions suggest that less institutionalised models can achieve the desired outcomes in the presence of political will and adequate capacity-building efforts. In particular, the Asia-Pacific Economic Cooperation has served as a global role model for catalysing domestic regulatory reforms across Asia and the Pacific, despite being a voluntary arrangement, without even a dispute settlement process. Similarly, the Pacific Alliance has made rapid and important strides in the services trade agenda despite its ‘ultra-light’ institutional structure, which does not include a standing secretariat. In both cases, it could be argued that the lighter legal and institutional structure has enabled, rather than deterred, greater progress. Experimenting with non-traditional approaches in EU-Africa trade cooperation can help bring services to the fore.

About the author

Iza Lejarraga is a trade policy expert with more than 15 years of experience in international organisations, academia, and the private sector. She has worked as a senior economist in leading international organisations, including the Organisation for Economic Co-operation and Development, the African Development Bank, the World Bank, and the Organization of American States. She has taught courses on trade and investment in the joint advanced policy programme of the University of Georgetown and the Solvay Brussels School of Economics and Management, and at the University of Paris (Sorbonne). She has also taught short courses at the Kiel Institute for the World Economy, the European University Institute, and the World Trade Institute. She holds a master’s degree in public administration in international development from the Harvard Kennedy School, and was a visiting scholar at Harvard’s Center for International Development.

Acknowledgments

This paper was made possible by support for ECFR’s Africa programme from the Bill & Melinda Gates Foundation.

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.