The green great game: Crafting an EU-Central Asia energy alliance

Summary

- Central Asia is diversifying partnerships beyond Russia and China, creating an opening for the EU.

- Energy and critical raw materials offer the most viable and mutually beneficial anchors for long-term cooperation.

- Regional cooperation is accelerating as Central Asian states resolve long-standing border and water disputes, paving the way for cross-border energy and infrastructure projects.

- Turkey and Azerbaijan are stepping up their engagement with the region, positioning themselves as potential logistical and diplomatic launchpads for Europe.

- The EU’s policy and financial tools are stronger than ever, but delivery is held back by weak legal protections, outdated infrastructure and Chinese competition.

- To secure a lasting role, the EU must act faster and more pragmatically, prioritising tangible projects and regulatory alignment to become a reliable “third force” in the region.

New playmates

Central Asia, a region of over 80 million people, rich in resources and serving as a strategic land bridge between major global markets, is increasingly seeking diverse partnerships. Historically influenced by Russia and currently heavily dependent on China, its countries are eager to strengthen their ties with Europe.

In April 2025, the inaugural Central Asia-EU summit in Samarkand marked a significant milestone, elevating relations to a strategic partnership. The EU announced €12bn in investments as part of Global Gateway, fuelling aspirations for cooperation in energy, infrastructure and trade. Clean energy presents the most promising area for EU collaboration. The region needs technology to tap into the full potential of its rich reserves of fossil fuels and rare earth minerals, resources the EU needs.

Furthermore, Central Asia’s strategic location is crucial for the Middle Corridor, also known as the Trans-Caspian International Transport Route, an integrated transportation route connecting China and Europe that circumvents Russia. The Middle Corridor is of particular interest to Kazakhstan and Uzbekistan, the region’s largest economies and the best positioned to cooperate with Europe.

Turkmenistan continues to adhere to a rigid foreign policy of “permanent neutrality”, with the ruling elite tightly controlling most aspects of life and promoting personality cults around its leaders. Tajikistan, still grappling with the devastation of the 1990s civil war, remains the region’s poorest and is heavily dependent on Moscow and China. And Kyrgyzstan, despite being the most democratic country in the region—evidenced by revolutions in 2005 and 2010 that forced leaders into exile—and having experienced rapid GDP growth in recent years (9% in 2024), still has a structurally weak economy, with limited diversification and an underdeveloped private sector.

In contrast, Kazakhstan’s strong-enough economic position allows it to more effectively implement what it calls a multi-vector foreign policy and balance its relationships with China and Russia. Uzbekistan has pursued a cautious liberalisation since the death of Islam Karimov in 2016, opening the doors to increased cooperation with the West. The new leader, Shavkat Mirziyoyev, has also prioritised resolving the many border disputes that previously hindered regional collaboration. In 2025, he convened with the leaders of Kyrgyzstan and Tajikistan in Khujand to sign agreements demarcating the tri-state border and establishing a formal declaration of friendship. Soon after, Kyrgyzstan and Tajikistan, which arguably had endured the most complex and violent border dispute since the Soviet collapse, also signed a historic border agreement. With territorial boundaries clarified and pacts to manage vital water resources, the region is increasingly becoming more integrated, facilitating cooperation with external partners.

However, despite this push to diversify their international relations, Central Asia remains wary of antagonising Russia, a concern the EU must carefully consider. Kazakhstan, in particular, is an active participant in Russia-led multilateral bodies—the Commonwealth of Independent States (CIS), the Collective Security Treaty Organization (CSTO) and the Eurasian Economic Union (EEU), as well as the China-led Shanghai Cooperation Organisation (SCO). China’s significant economic presence in the region, particularly through the Belt and Road Initiative (BRI), also poses a challenge for the EU. As Chinese-led investment and infrastructure projects flourish, the EU must strive to present attractive alternatives.

This paper makes the case for deeper EU energy cooperation with Central Asia. By supporting Central Asia’s quest for diversified partnerships, the EU can significantly bolster its energy security while deepening its strategic position. The paper will first chart the region’s shifting geopolitics: Russian dominance is eroding, China’s economic weight is rising but is persistently dogged down by public resistance, and the US, Turkey and Azerbaijan are stepping up their game. It will then map Central Asia’s energy and resource offer, from fossil fuels and critical raw materials to renewables and early-stage hydrogen, and assess what the EU is currently doing, from partnership agreements and financing tools. Finally, it will identify the main barriers to cooperation and offer practical recommendations for both Central Asian governments and the EU to turn promises and potential into tangible projects.

Navigating partnerships

Russia’s dwindling role

Historically, Russia has been Central Asia’s main political, military and economic partner. Moscow continues to maintain this influence through deep economic links, labour migration from these regions to Russia (especially from Tajikistan, where remittances account for half of its GDP), security guarantees via the CSTO (of which Kazakhstan, Kyrgyzstan and Tajikistan are part of) and cultural and linguistic ties.

This influence has lately begun to decline, especially in the wake of Russia’s invasion of Ukraine. Central Asian countries are increasingly viewing Russia not only as a partner but as a potential source of risk. This shift is reflected in both public attitudes and policy decisions. While historically Russia has enjoyed favourable views among the populations of these countries, polls conducted since 2022 paint a somewhat different picture. Besides, more than half of the region’s population is under 30 years of age, and their ties to Russia are much looser than those of their parents or grandparents.

All Central Asian countries have maintained a neutral stance on Russia’s aggression in Ukraine. None has recognised the annexation of Ukrainian territories or provided military support, although they have avoided openly criticising Moscow. Their neutral stance is also reflected in their voting patterns on related UN resolutions, where they often abstain or choose to be absent.

Kazakhstan in particular has taken notable steps to distance itself from the Russian aggression. For example, it declared support for Ukraine’s territorial integrity and unequivocally rejected the possibility of recognising the independence of the so-called Donbas republics before Russia’s illegal annexation of these regions in September 2022. Around 15% of Kazakhstan’s population is comprised of ethnic Russians, most of whom live in the northern part of the country. The fact that Russian public figures continue to make statements questioning Kazakhstan’s sovereignty over these areas has further prompted Kazakhstan to seek stronger ties with Western partners. This shift is particularly notable considering that, as recently as January 2022, Russian troops were dispatched to the country to quell protests over fuel price hikes.

However, Kazakhstan and Kyrgyzstan remain key for Russia to circumvent Western sanctions. Russia has extensively used these countries for parallel imports and re-exports of sanctioned goods, including dual-use technologies critical to its economy and military. This also helps explain the increase in trade turnover between Russia and Central Asia since 2022.

China’s soft power struggle

In this century, China has emerged as a major economic partner for Central Asia. It is the main trading partner of all countries except Kazakhstan, whose top partner is the EU—although China does not trail that far behind. In Kyrgyzstan and Tajikistan, China is also the main creditor and investor, and all countries in the region participate in the BRI.

By 2019, a total of 261 projects involving Chinese participation were underway in Central Asia, either through the BRI or bilateral initiatives, including a railway line from China through Kyrgyzstan to Uzbekistan, currently under construction. This route would bypass Russia and potentially Central Asia to South Asia via Afghanistan in the future. From Central Asia’s perspective, the cross-regional BRI projects are not a path to dependence on China, and are believed to align well with its ambitions for greater regional cooperation.

However, public attitudes towards Beijing across the region have long been negative. Underlying much of this antipathy is a blend of historical grievances and racism, compounded by concerns with the labour and environmental practices of Chinese firms. China’s demographic superiority fuels fears of migration, job stealing and interethnic marriage, while its treatment of the Uyghur minority in Xinjiang, while not necessarily generating widespread sympathy, fosters perceptions of China as “anti-Muslim”.

In Kyrgyzstan in particular, being the more democratic country in the region (at least before Sadyr Japarov came to power), anti-Chinese protests are notably frequent. In 2020, a $275m Chinese project to build a logistics centre in the eastern part of the country was abruptly cancelled following local demonstrations. Similar small-scale protests have also occurred in Kazakhstan, and even in further away Uzbekistan, anti-China sentiment has emerged on social media.

While China has long dismissed these sentiments as the “China threat theory,” there is a growing recognition among Chinese policy experts of the limitations of China’s soft power in the region. BRI policy documents emphasise the importance of cultural, artistic and media exchanges to mitigate these negative perceptions. Although there is some evidence of younger generations in Central Asia viewing China more favourably, this shift has yet to significantly influence overall public sentiment.

Renewed US involvement

The perceived lack of US interest in Central Asia has long faced criticism. In 2022, the US launched the Economic Resilience Initiative in Central Asia (ERICEN), focusing on expanding trade and strengthening the private sector and human capital. The initial funding for this initiative was set at only $30m, expanded to $50m in 2023 following a visit by then-Secretary of State Antony Blinken to Kazakhstan and Uzbekistan (the first visit by a US Secretary of State in three years). Experts have said that the funding is insignificant compared to what other powers are bringing in.

But there are reasons to believe this could change. In the Central Asia-US summit held in Washington in November 2025, all participating countries signed a Joint Statement of Intent on Economic Cooperation, along with several bilateral agreements with select nations. Kazakhstan and the US signed a memorandum of understanding on critical minerals and rare earths. Kazakhstan has reserves or production capacity for about half of the 54 minerals considered essential for national security by the US Geological Survey.

In addition, the US and Kazakhstan have established a joint venture to develop tungsten deposits in North Katpar and Upper Kairakty, some of the world’s largest. The American Cove Capital holds a 70% stake in the joint venture and controls metal sales, while the Kazakh Tau-Ken Samruk, a state company, holds the remaining 30%. Total investment amounts to approximately $1.1 billion. This move reflects the American strategy to diversify its supply of critical raw materials beyond China.

The US also signed bilateral agreements with Uzbekistan on rare earths, including tungsten. To operationalise these objectives, the partners have agreed to form a Joint Working Group, which will conduct technical and financial feasibility studies and coordinate investment.

While renewed US involvement could contribute to the relevance and development of the Middle Corridor, it could also pose a challenge for the EU. A more pragmatic US administration is unlikely to impose the stringent requirements and conditions for which EU engagement is known. Europe risks being sidelined in a region where big powers compete for influence and resources.

Enter Turkey (and Azerbaijan)

Thanks to its shared ethnic, linguistic and cultural ties in Central Asia, Turkey is well-positioned to capitalise on Moscow’s waning influence. While the role of the Organisation of Turkic States (OTS) is still limited, and Turkey cannot yet match Russia’s established position in security or the scale of Chinese investment, Ankara is not standing still.

As Central Asian nations seek to reduce their dependence on Russia for energy transportation, Turkey is increasing investments in infrastructure along the Middle Corridor, of which Azerbaijan is of course a key piece. Baku is pursuing several joint energy projects with Central Asian countries (discussed below), viewing them as means to strengthen its role as a transit hub between Asia and Europe and increase the energy significance of the Caspian Sea region. This outreach culminated in November 2025, when Azerbaijan was formally admitted as a full participant in what had been the C5 format of Central Asian presidents. Some commentators have suggested that this has marked the beginning of the C6 format. Such cooperation not only enables Azerbaijan to diversify its fossil fuel exports but also paves the way for future investments in clean energy, deepening its strategic partnership with the EU.

For Azerbaijan, the Middle Corridor is not only a transport route but also a geopolitical project aimed at enhancing its strategic autonomy. By integrating into Central Asian supply chains, including energy, transit and digital connectivity, Baku mitigates its vulnerability to disruptions from Russia or Iran. And after consolidating control of Nagorno-Karabakh, Azerbaijan has acquired greater diplomatic and strategic capacity to pursue these plans.

However, Azerbaijan’s ambitions to strengthen cooperation with Central Asia are not uniformly embraced by all Central Asian countries. While Uzbekistan is more open to it (the Uzbek president called for setting up the Community of Central Asia with Azerbaijan included, for example), Kazakhstan and Kyrgyzstan, the two members of the Russia-led Eurasian Economic Union, seem to be more cautious. Nevertheless, increased engagement with Azerbaijan and Turkey, along with the region becoming more integrated, present positive opportunities for Europe.

Central Asia’s resource landscape

Fossil fuels and nuclear

While hydropower is the main energy source for Kyrgyzstan and Tajikistan, fossil fuels remain vital for Kazakhstan (mostly coal), Uzbekistan and Turkmenistan (mostly natural gas). With the EU accelerating efforts to reduce its dependence on Russian fossil fuels following Russia’s aggression against Ukraine, Central Asia has emerged as a promising partner in meeting the union’s energy needs.

The main EU programmes designed to achieve this are the REPower EU and the Roadmap, put forth by the European Commission. The REPowerEU programme, announced in May 2022, mobilises investment in renewable energy and infrastructure for gas and hydrogen, while accelerating the deployment of clean energy technologies across the Union. The Roadmap, announced in May and June 2025, outlines a coordinated and gradual phasing out of Russian oil, gas and uranium imports by all member states by the end of 2027. The strategy includes bans on new contracts as well as plans to diversify supplies. The relevant regulations have been approved by the European Parliament in late 2025 and are expected to be approved by the European Council early in 2026.

Following Russia’s invasion of Ukraine, the EU’s crude oil imports from Kazakhstan increased by 48%, positioning the country as the EU’s third largest supplier after the US and Norway. However, these imports rely heavily on pipelines or Baltic sea ports in Russia. In 2024, nearly 93% of Kazakhstan’s oil exports were transported via these routes.[1]

Although Astana is uncomfortable with its level of dependence on Russian territory, it is interested in increasing transport via the Druzhba pipeline. In December 2025, the Kazakh company KazTransOil opened an office in Poland, crucial for facilitating the transit of Kazakh crude to the German refinery in Schwedt. This is the company’s first representative office in the EU and underscores Poland’s role as a transit point for raw materials. However, more important is Kazakhstan’s interest in increasing exports by tanker across the Caspian Sea and through Azerbaijan to reach European customers, which would bypass Russia.

Kazakhstan also accounts for 40% of global uranium production and is the leading provider for the EU’s nuclear energy sector, meeting 21% of the EU’s total uranium needs. There is potential for further cooperation in this area. Bulgaria and Finland are currently in discussions with Kazakhstan to increase uranium imports. Central and Eastern European countries that are currently planning large nuclear projects, such as Poland, could also become potential markets in the future.

Turkmenistan has the fifth-largest global reserves of natural gas, although most of it remains undeveloped. In 2024, 73% of all its gas exports went to China. As there are no pipelines connecting Turkmenistan to Europe bypassing Russia, it is currently not viable for the EU to tap into this potential.

Clean energy

Critical raw materials

Central Asia is abundant in rare earth metals and critical raw materials essential for the EU’s energy transition. Kazakhstan in particular can supply 21 of 34 raw materials classified as critical by the EU, including several deemed strategic. Currently 19 of them are already extracted and processed in Kazakhstan. The country has significant potential to produce tungsten, a key component in renewable energy equipment, with estimated reserves of over 2 million tonnes of tungsten trioxide, which could account for half of the world’s total known reserves. Kazakhstan also controls 2% of the world’s copper reserves (11th largest globally) and accounts for 3.3% of global copper production. The country is also the second-largest producer of chromium.

Uzbekistan has significant reserves of 32 critical raw materials, including 2.4% of the world’s graphite reserves. It has reserves of lithium, rhenium, tellurium, germanium, tungsten and vanadium. Uzbekistan is currently a major producer of copper, uranium and silver, as well as contributing 3% to the world’s gold production.

According to the US Geological Survey, 384 rare earth metal deposits have been identified in Central Asia, with 160 located in Kazakhstan, 87 in Uzbekistan, 75 in Kyrgyzstan and 60 in Tajikistan. In Turkmenistan, while limited data availability prevents reliable assessment, some available studies indicate that it may have reserves of lithium, copper ores and rare earth elements.

Despite this potential, exports of critical raw materials from Central Asia to the EU are small. Of the 34 critical raw materials identified by the EU, only three are imported in significant quantities from Central Asia: 65% of the EU’s phosphorus comes from Kazakhstan, 54% of its antimony comes from Tajikistan and 36% of titanium metal from Kazakhstan.

These limitations can be explained by infrastructure constraints, such as bottlenecks at Caspian ports and high transit costs, as well as China’s dominance in processing. In 2024, China imported 70% of all the critical raw materials extracted in Central Asia. The situation is further complicated by Central Asia’s limited investment in modern extraction and processing technologies, and its partnerships in the sector with China and Russia. This creates a competitive and challenging environment for the EU.

Although the EU plans to develop its own mining projects for critical raw materials in Sweden and Portugal, the union will likely remain dependent on imports for a long time. Given its significant reliance on China for these materials, the EU needs to seek alternative sources of supply, with Central Asia representing a promising option.

Renewable energy sources

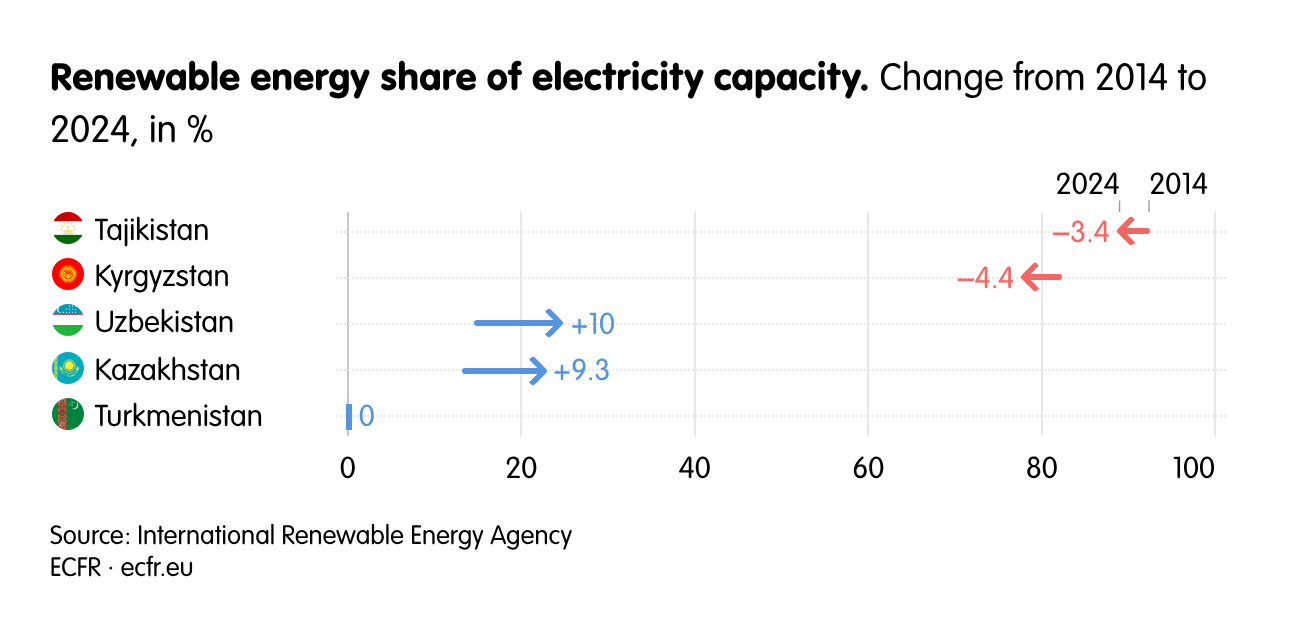

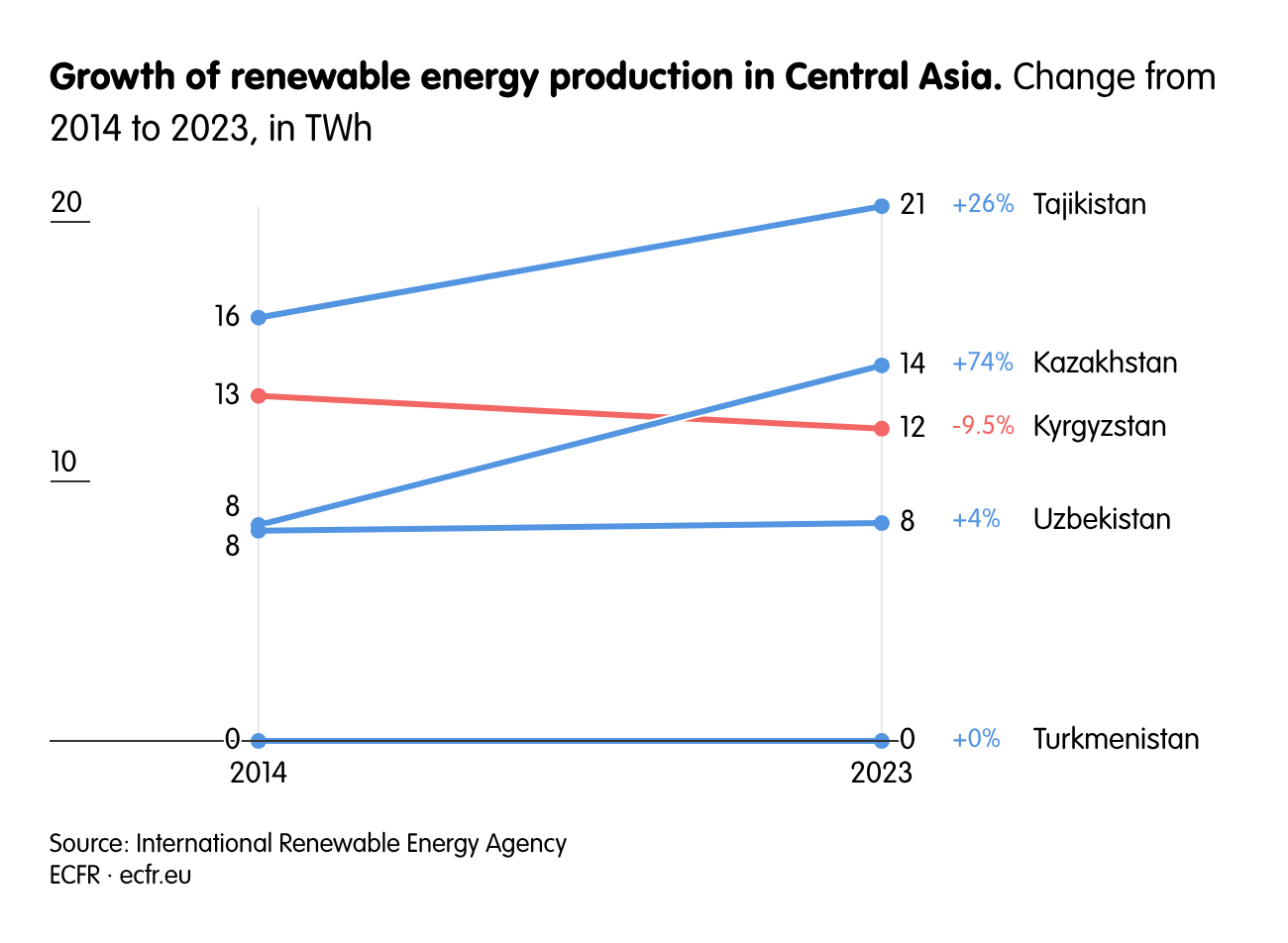

According to analyses by the International Renewable Energy Agency (IRENA), the UN and the World Bank, Central Asian nations have the potential not only to generate renewable energy for domestic consumption but also for export. Kazakhstan, Uzbekistan and Turkmenistan have the greatest potential for the development of solar, wind and geothermal energy. In contrast, Kyrgyzstan and Tajikistan are well-suited for hydropower. Tajikistan has only tapped into 5% of its hydropower potential, estimated at 527 billion kWh per year. This indicates substantial room for growth in the renewable sector.

Leaders of most countries in the region are keen on developing renewable energy sources. In 2019, Uzbekistan adopted a Green Economy Strategy for 2019–2030, aiming to increase the share of renewable energy sources in its energy mix to 40%, up from 13% in 2022. Kazakhstan aims to increase the share of renewable energy in electricity production to 50% by 2050. It also aims to achieve climate neutrality by 2060. In 2024, the president of Tajikistan, Emomali Rahmon, declared that 100% of the country’s electricity generation will come from renewables by 2032. In June 2025, Tajikistan presented its first-ever national Green Energy Roadmap, which includes the goal of net-zero carbon emissions by 2050.

Both Uzbekistan and Kazakhstan are working to export surplus clean energy to neighbouring markets, such as other Central Asian countries and Afghanistan, but also to more distant regions like the South Caucasus and Europe. They have begun implementing various projects to facilitate these exports, themost important of which is the Trans-Caspian Green Energy Corridor. This project will connect power grids in Kazakhstan and Uzbekistan to Azerbaijan via the Caspian Sea to export electricity to Turkey and Europe.

The Trans-Caspian Green Energy Corridor will be developed by the Green Corridor Alliance, a Kazakh-Uzbek-Azerbaijani joint venture, and will be funded by the Asian Infrastructure Investment Bank. The project is the culmination of a strategic partnership agreement signed by the three countries during COP29 in 2024 in Baku. The plan is to begin electricity exports in 2032, initially at a volume of 4 gigawatt-hours and ultimately at 6 gigawatt-hours.

In December 2022, Azerbaijan, together with Georgia, Romania, Hungary and later Bulgaria, initiated a project to build a green electricity bridge across the Black Sea. Serbia and Moldova have also expressed interest in this initiative. Originally designed for Azerbaijan to export electricity to Europe, the project now has the potential to benefit Central Asian exports too. The parties have established the GECO (Green Energy Corridor) consortium and will seek to obtain Projects of Common/Mutual Interest (PCI/PMI) status in the EU, which gives projects priority for faster permits and access to funding.

By connecting the energy systems of Central Asia with those of Europe, projects such as the Caspian and Black Sea energy bridges are set to play a crucial role in integrating the energy systems of Central Asian countries as well as strengthening Europe’s energy security.

Another cross-border project aimed at producing clean electricity is the CASA-1000 (Central Asia–South Asia Electricity Transmission and Trade Project). This major regional infrastructure initiative is aimed at facilitating cross-border electricity trade between Central and South Asia. It is designed to transmit up to 1,300 megawatt of surplus hydropower from Kyrgyzstan and Tajikistan to energy-deficit markets in Afghanistan and Pakistan, primarily during peak summer months. As of 2025, construction in Kyrgyzstan and Tajikistan was largely complete, with the remaining components expected to be finalised and commercial operations to begin between 2026 and 2027. The project involves the development of high-voltage transmission lines and converter stations and is financed by a consortium of international development partners led by the World Bank. Beyond its technical scope, CASA-1000 is often cited as a test case for regional energy integration, infrastructure-led cooperation, and the monetisation of seasonal hydropower surpluses in Central Asia.

As for hydropower projects, the Kambarata-1 hydropower plant, in Kyrgyzstan, and the Rogun dam, in Tajikistan, besides expanding renewable generation capacity, have significant cross-border and external implications. Kambarata-1 is substantially supported by international financing, including the European Investment Bank. Upon completion, the project is expected to increase national electricity output, enhance energy security and strengthen Kyrgyzstan’s role within the unified Central Asian power grid, thereby enabling greater regional electricity exports. In Tajikistan, the Rogun Dam, one of the tallest dams in the world, is a central pillar of the country’s long-term energy policy. The project aims to generate large volumes of low-carbon electricity, supporting Tajikistan’s objective of achieving near-total reliance on renewable energy by 2032. Beyond domestic supply, Rogun significantly enhances Tajikistan’s potential as a regional electricity exporter, particularly in light of the emerging cross-border transmission initiatives linking Central and South Asia.

Hydrogen

Central Asia has considerable opportunities for green hydrogen production, with several countries already initiating hydrogen projects with foreign partners. In 2025, Uzbekistan launched the region’s first green hydrogen production plant, aiming to produce 3,000 tonnes of green hydrogen per year. Saudi Arabia’s ACWA Power and China’s Donghua Engineering are involved in its implementation.

Currently, green hydrogen only plays a minor role in Kazakhstan’s industry, mainly in refineries and fertiliser production, but Astana is hoping to change this. Kazakhstan has the capacity to produce both green and the cleaner blue hydrogen. In April 2024, the Kazakh Ministry of Energy adopted the “Concept for the Development of Hydrogen until 2040”, which targets at least 50% of hydrogen production to be green by that year.

One of the most ambitious hydrogen initiatives in the region is Kazakhstan’s Hyrasia One, led by Swedish-German company Svevind Energy Group. This project aims to build renewable energy farms with a combined capacity of approximately 40 GW of wind and solar power, which will supply a 20 GW water electrolysis plant located on the Caspian coast. Once fully operational, targeted for around 2032, Hyrasia One is expected to produce up to 2 million tonnes of green hydrogen per year, or, after processing, up to 11 million tonnes of green ammonia annually.

As part of its low-carbon development strategy, Kazakhstan is also pursuing clean hydrogen pilot projects. One such initiative uses the laboratory unit at KMG Engineering’s Atyrau laboratory to produce green hydrogen. KMG Engineering is a subsidiary of the oil and gas company KazMunayGas (KMG). The project is being carried out in partnership with the Kazakh company Green Spark and uses a 200 kW solar power plant, with plans to install an electrolyser that will split ordinary water into oxygen and pure hydrogen. Another pilot project, launched in December 2025, is Kazakhstan’s first integrated green hydrogen production station, based on its own patents and engineering developments.

The state of EU-Central Asia energy ties

In recent years, the legal framework governing relations between the EU and Central Asian countries has strengthened significantly, both at the multilateral and bilateral levels. In May 2019, the EU adopted a new strategy on Central Asia and, in October 2023, a joint roadmap to complement it.

The first document outlines a renewed EU strategy to deepen cooperation with the region by supporting reforms, boosting economic modernisation and concluding partnership agreements. The Joint Roadmap sets out a concrete action‑oriented framework across five priority areas: enhancing political dialogue and cooperation; expanding trade, investment and economic links; boosting energy, climate and connectivity cooperation under the Global Gateway; tackling shared security challenges; and strengthening people‑to‑people contacts and mobility.

In addition, the EU has signed partnership agreements with several individual countries: Kazakhstan (December 2015), Kyrgyzstan (June 2024) and Uzbekistan (October 2025), while a similar EPCA has also been initialled with Tajikistan (July 2025). The EU has not yet ratified a partnership agreement concluded in 1998 with Turkmenistan.

These new partnership agreements replace the old agreements of the 1990s, upgrading and expanding cooperation in areas such as trade, sustainable development, digital technologies and political dialogue, while aligning with the EU’s 2019 Central Asia Strategy.

The agreements on cooperation on critical raw materials and hydrogen are currently only memoranda, ie, they do not create firm commitments for cooperation. These include a November 2022 memorandum on raw materials, batteries and renewable hydrogen signed with Kazakhstan, and another on raw materials with Uzbekistan.

Another such initiative is the EU Support to Sustainable Energy Connectivity in Central Asia (SECCA). Launched in 2022, it aims to help Central Asian countries adopt more sustainable energy systems, offering regulatory and institutional support for renewable energy and inclusive energy access aligned with EU best practices.

The EU’s financial institutions also play an important role in its policy towards Central Asia. The EBRD is the largest single institutional investor in Central Asia. To date, it has financed 1,163 green and inclusive projects with €21.5bn. In 2024 alone, it directed €2.26bn to 121 projects across Central Asia—nearly twice the volume invested in 2023. An additional €784m mobilised from partners brought the total capital flowing to the region’s green sector to over €3bn. Uzbekistan and Kazakhstan were the primary destinations for EBRD resources, receiving €938m and €913m in 2024 respectively, with 58% of those aimed at promoting clean economy projects. The EBRD also supports green projects in Tajikistan, including renewable generation and electricity grids.

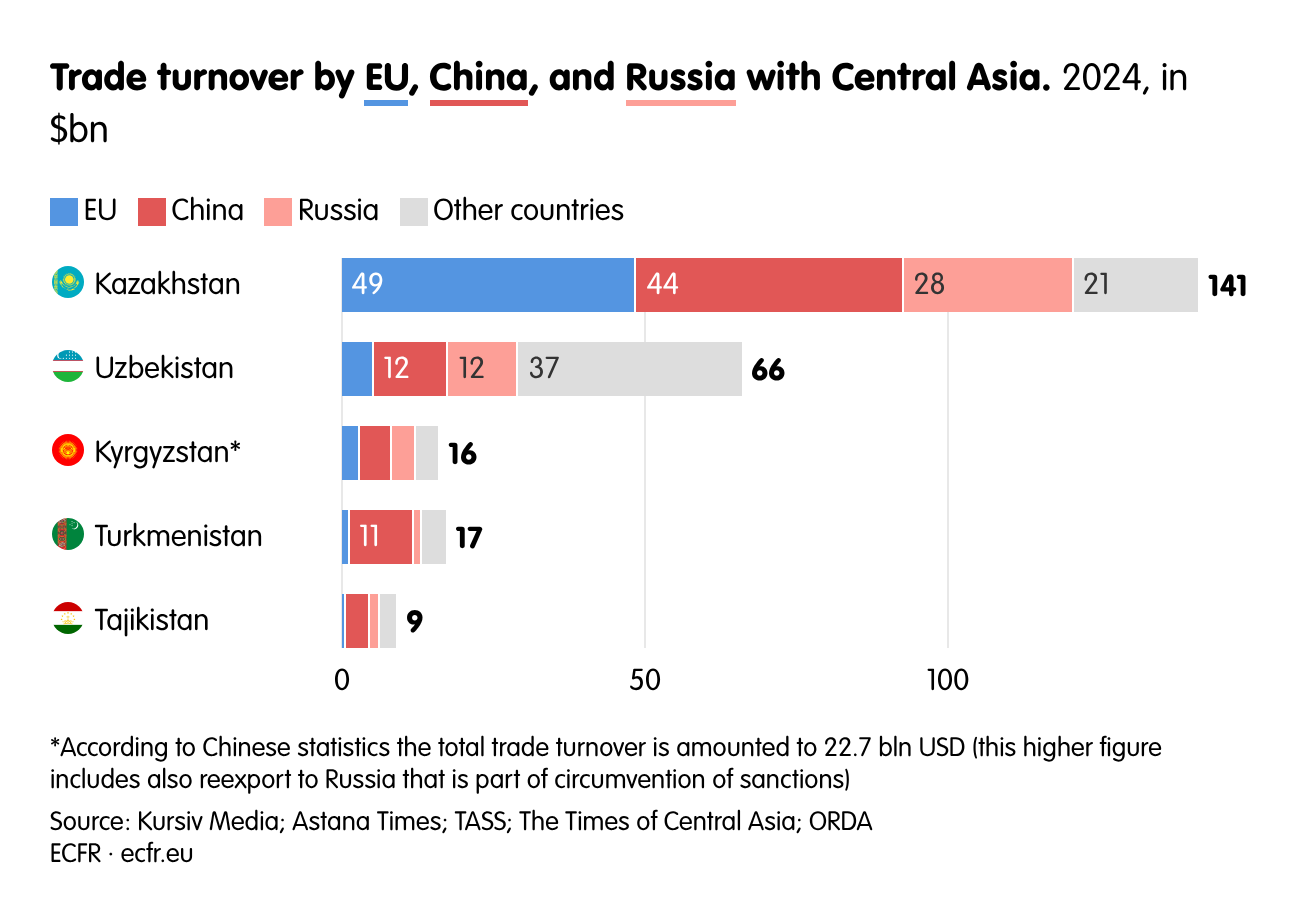

As for trade, the EU accounts for approximately 25% of the total turnover with Central Asia. The EU is Kazakhstan’s largest trading partner, with 90% of its exports to the EU consisting of oil, gas and uranium. However, in the other countries, the EU’s trade turnover is much lower than China’s.

Although EU direct investment in the region is growing steadily, it is still lower than that of other countries active in the region. According to official EU data, total EU investments in Central Asia over the past decade were €100bn, while according to the Kazakh authorities, China’s total investment in the region amounted to $40bn in 2024 only. These figures match data from the Asian Development Bank, which shows China’s FDI in the region amounted to roughly $27.7bn in the first half of 2024. According to the ADB, the largest share went to Kazakhstan ($10.4bn), followed by Turkmenistan ($9.5bn) and Uzbekistan ($4.3bn).

The agreements on CRM are not yet supported by significant financial proposals. The EU currently plans to allocate only €16m for critical raw materials and €30m in renewable energy projects. The outcome of the recent 3rd EU-Central Asia Economic Forum in Tashkent is also unimpressive in this regard. In total, agreements worth only €100m were concluded, including very little related to CRM: one between the EU and UNODC/UNECE worth €3m for the SECURE CRM project, and another between the EU and EBRD worth €3m, for the GROW CRM project.

Key barriers to cooperation

Energy cooperation between the EU and Central Asia runs up against a thicket of obstacles, including political reluctance, outdated infrastructure, weak legal frameworks and scarce investment. These internal challenges are compounded by powerful geopolitical pressures, notably the influence of China, the US and Russia, as well as the still-fragmented cooperation within Central Asia itself. The slow pace of implementation of EU initiatives and investments poses an additional constraint. Neither member states nor European companies are making full use of funds or showing sufficient determination to mobilise the funds already committed by the EU for energy cooperation in the region.

Political will: The missing spark

Although Central Asian countries, especially Kazakhstan and Uzbekistan, show interest in cooperating with the EU, they are less willing to carry out reforms that would create the necessary conditions for this cooperation to flourish. While Astana and Tashkent have taken steps to reform laws to support investment and business activity, significant challenges remain: legal unpredictability, low transparency, persistent corruption and weak protection mechanisms for investments. As previously mentioned, even greater barriers exist in Tajikistan and Turkmenistan. The relatively democratic and open Kyrgyzstan has in recent years been moving closer to an authoritarian model under President Japarov, turning the environment less conducive for investment.

The OECD regularly highlights that attracting private investment to the region and doing business is hampered by numerous legal and institutional barriers. Despite efforts to modernise business regulation, the region continues to face challenges with complex, fragmented, and sometimes contradictory legal frameworks that hinder entrepreneurial activity and small firms. Frequent regulatory changes, often imposed without input or notice from the business community, further exacerbate these difficulties.

While some reforms in tax policy and administration have been implemented in most countries—notably digitalisation of tax administration—taxation remains riddled with problems. Businesses also grapple with costly and complicated customs procedures and border regulations. Additionally, dispute settlement, especially within domestic courts, continues to be a major challenge. Although authorities in Kazakhstan and Uzbekistan are dedicated to pursuing reforms and maintaining macroeconomic discipline, successful implementation will demand substantial political determination and administrative capacity.

Another aspect of the underdeveloped legal framework is the specific nature of the energy markets in these countries. Unlike the liberalised and relatively integrated EU market, the markets in Central Asia are poorly integrated, with low competition, high electricity subsidies, and underdeveloped exchanges. Furthermore, state-owned entities play a dominant role in these markets.

Another example is hydrogen regulation. Although some Central Asian countries hold promise for hydrogen production (such as Kazakhstan, as previously mentioned), adequate legal frameworks and support mechanisms for hydrogen projects are still lacking. Existing regulations primarily focus on traditional fossil fuels, leaving low-carbon technologies and green hydrogen without a dedicated legal framework or fiscal incentives. The absence of comprehensive regulations covering hydrogen production, storage and transport limits sector development and deters foreign investors. Moreover, the lack of safety standards and environmental norms for hydrogen production and distribution increases the risk of accidents and limits the scale of implementation.

Infrastructure constraints

Central Asian countries currently have no gas connections to the EU bypassing Russia. Discussions about gas pipelines linking Central Asia with Europe, including the Trans-Caspian gas pipeline project, have been ongoing since the 1990s but have never been implemented.

As for the power grid, most Central Asian countries have been connected since Soviet times through the Unified Energy System of Central Asia (UES CA), created in the 1960s initially including the southern regions of Kazakhstan, Kyrgyzstan, Tajikistan, Turkmenistan and Uzbekistan. The system was designed to enable electricity exchange and balancing between hydro and thermal capacities, but many changes occurred after the collapse of the USSR. In 2003, Turkmenistan left the UES CA, followed by Uzbekistan in 2009. It was only in 2016, after the normalisation of political relations between Uzbekistan and its neighbours, that intra-regional cooperation in the electricity sector began to improve. In June 2024, Tajikistan was partially reconnected to the UES CA, and full synchronisation of the Tajik electricity system with it is expected in 2026.

Currently, cooperation within the CA UES enhances electricity security in the region’s countries at different times of the year. Kyrgyzstan and Tajikistan traditionally export hydro energy in winter, while Uzbekistan and Kazakhstan export thermal energy in summer. Turkmenistan, which operates largely in isolation from the UES CA, maintains a limited synchronous connection with Uzbekistan, used occasionally for emergency support and short-term balancing.

A significant part of the transmission networks dates back to the Soviet era, and some countries’ grids are physically connected to the Russian transmission network (Unified Energy System, or IPS/UPS), which is operated from Moscow. This is the case with Kazakhstan, and indirectly applies to Uzbekistan and Kyrgyzstan too, since their grids are connected to Kazakhstan’s. Although the UES CA is not synchronised with IPS/UPS, meaning they do not operate at the same electrical frequency and phase—so power flow is not as seamless—the physical connections between the two systems enable balancing and exchange of electricity. Under certain conditions, they provide Russia with situational leverage over these countries. For example, during periods of stress (peak demand for electricity, outages or droughts affecting hydropower), Russia could potentially limit flows or impose conditions for support.

More importantly, Central Asia’s grid also needs upgrading. According to 2012 data from the Asian Development Bank, approximately 75% of the network in Tajikistan and Uzbekistan is over 30 years old; in Kyrgyzstan and Kazakhstan, the proportion is 64% and 44%. According to a 2023 World Bank report, nearly 40% of the existing power generation infrastructure in the whole region has exceeded its expected lifespan, leading to frequent power outages.

Outdated, underdeveloped and inflexible networks contribute to electricity shortages that have been common in recent years. In January 2022, Uzbekistan experienced a nationwide blackout, resulting in power outages in Kazakhstan and Kyrgyzstan. During the winter season of 2022-2023, blackouts occurred in both Uzbekistan and Kazakhstan.

According to the Asian Development Bank, in order to ensure uninterrupted electricity transmission, Central Asian countries should invest approximately $33bn in grid modernisation and expansion by 2030. However, there are currently no incentives for private or state-owned companies to do so.

Technical barriers also hinder the exploitation of critical raw materials and rare earth metals. For example, only 40% of Uzbekistan’s territory has undergone geological surveying, and only 16 of the 71 identified deposits of critical raw materials are currently in production. In addition, the lack of skilled labour and technical expertise needed for advanced mining technologies may slow down the process of developing deposits.

Infrastructure barriers also hinder the development of hydrogen projects. These include steep production costs and the construction of cross-border transport infrastructure, alongside the slow development of the international hydrogen market. Hyrasia One exemplifies these issues. While an ambitious initiative, high implementation costs (€40–50bn) cast serious doubts about its viability.

Water scarcity

While intra-regional tensions over water management have eased since the early post-Soviet years, and some joint management initiatives are currently in place, water remains a scarce resource, further strained by the impacts of climate change. Traditionally, Kazakhstan, Uzbekistan and Turkmenistan primarily use water for agriculture, while Kyrgyzstan and Tajikistan rely on it for approximately 80% of their electricity generation. As the region pushes to develop renewable energy and hydrogen, competition for water is set to intensify and could potentially reignite tensions over resource allocation.

Recommendations

For Central Asia

Improve the legal framework

Central Asian states urgently need a more coherent and predictable legal framework to bolster investor confidence and ensure effective, transparent regulation of their rapidly evolving energy markets. To enhance energy cooperation with the EU, they need to align their legal frameworks with EU standards. This includes adopting transparent investment laws, strengthening intellectual property protection for energy technologies and establishing robust dispute resolution mechanisms aligned with international norms such as the Energy Charter Treaty principles or international arbitration standards. Streamlining regulatory approvals for cross-border projects and incorporating ESG criteria will attract EU investments in renewables and gas. Such reforms would foster trust, reduce risks, and unlock sustainable energy partnerships, ultimately boosting economic integration and regional stability.

Deepen regional cooperation

Strengthening regional cooperation and deepening institutional integration would significantly improve cooperation with the EU. The Central Asian Community, if established, could evolve into a truly integrated organisation, covering energy markets, water and energy resource management, data collection and strategic investment planning. Deepening ties with Azerbaijan can play a crucial role in connecting Central Asia with the south Caucasus and the EU, contributing to the establishment of the Middle Corridor.

Make renewables a priority

Expanding renewable energy sources in Central Asia can strengthen its energy security, accelerate decarbonisation and increase competitiveness, paving the way to export clean energy to foreign markets. This would not only generate additional revenue but also bolster the region’s position in the global energy transition. As Central Asian countries start to develop renewable energy infrastructure, aligning their efforts with the EU’s energy diplomacy and clean energy transition goals could become vital. By adopting EU-compatible standards and joining global pledges, such as the Global Renewables and Energy Efficiency Pledge, they can attract technical assistance, investments via Global Gateway, and partnerships through EU programmes such as SECCA.

Investment in the grids

Modernising infrastructure is essential to develop renewables in Central Asia. Funding could come from transmission tariffs. Currently, these rates are insufficient to cover the costs of network maintenance. Increasing them would generate necessary funds, besides helping attract private capital (although hikes need to be managed carefully to avoid political discontent). Central Asian countries could rely on support from European banks (EIB, EBRD) to expand power grids, including interconnections between countries.

Develop hydrogen for internal needs

Countries in the region should develop their hydrogen potential cautiously, prioritising internal rather than external needs, and carefully considering water access issues. Hydrogen can be an important means of decarbonising industrial production, including steel, chemical and oil refining. However, the costs of building export infrastructure are currently very high, and the hydrogen market is still too underdeveloped to make it worth it. As a result, an export orientation could prove unprofitable for both Central Asia and the EU.

For the EU and its member states

Be pragmatic and fast

Given Central Asia’s political diversity, fragmented legal regimes and chronic infrastructure development delays, the EU should keep its strategy grounded in reality. Weak connectivity with Europe and outdated energy infrastructure are long-term problems, not quick fixes. Expectations of political liberalisation need to be tempered. The EU and its member states should therefore narrow their focus to a limited set of strategic priorities and start with deepening ties with Kazakhstan and Uzbekistan.

Focus on renewables and CRM

Investments in renewable energy and critical raw materials should be a top priority. In renewables, EU companies should become involved in capacity expansion and network investments, including ownership stakes in infrastructure. This would strengthen the medium- and long-term prospects of delivering clean electricity from Central Asia via the Caspian Sea to Europe. EU companies could play a role in developing renewable energy zones.

Rapid action is also needed regarding CRM. Memoranda must be followed quickly with specific contracts, including involvement in exploration and extraction, given that many resources are still undeveloped. EU companies cannot afford to move slowly, especially in light of agreements such as the recent US-Kazakhstan deal on tungsten, for example.

Beyond extraction, EU countries also need to invest in the processing of critical raw materials, a segment currently heavily dominated by China. This aligns with the interests of Central Asian countries themselves, which are keen in expanding their own processing capacity. Kazakhstan has already identified four priority areas: battery materials, semiconductor inputs, heat-resistant alloys for jet engines and permanent magnet recycling. The country also plans to produce 15 tonnes of gallium per year, expand production of high-purity manganese sulphate and increase the output of graphite for battery components. Facilities in Zhezkagan and the Ulba Metallurgical Plant will soon begin manufacturing heat-resistant nickel alloys and recycling permanent magnets in cooperation with EU partners. Investments in processing will drive job growth and prosperity in the region, strengthening the EU’s position there.

Boost institutional and financial support

The EIB and EBRD should keep their involvement pace, and their plans to open a branch in Tashkent are positive. However, this should be followed by a tangible increase in investment. The EU already has credible instruments at its disposal and has earmarked €12bn for Global Gateway in 2025. What it lacks is speed. It is currently lagging behind its competitors, above all China, but also the US and even Russia. Donald Trump is already concluding binding agreements with Kazakhstan and Uzbekistan, while Chinese companies operate many CRM projects in the region, importing about 70% of its mined output.

The EU’s priority should be the launch a dedicated Central Asia Clean Energy Partnership under Global Gateway, with a €5–10bn multi-donor investment platform for bankable renewable and green hydrogen projects. De-risking instruments, such as EFSD+ guarantees and blending grants, should be paired with rapid deployment of technical assistance teams to harmonise standards, streamline permitting and build cross-border grid interconnections, especially across the Caspian Sea. A concrete, high-visibility initiative would outpace Chinese and Russian offers, secure diversified clean energy imports for Europe and anchor Central Asia firmly in the EU’s green value chain.

Boost technological and regulatory support

The EU should complement investment with support on technology transfer, ESG standards support, and regulation and management of water and energy crises. It should also build on existing intra-regional initiatives, such as the agreement concluded in September 2025 between Kazakhstan, Kyrgyzstan and Uzbekistan on the joint management of water resources. The agreement stipulates that Kyrgyzstan will release water from the Toktogul Hydroelectric Power Plant (HPP) reservoir to downstream Kazakhstan and Uzbekistan. In return, Kyrgyzstan will receive electricity from both countries through spring 2026.

The EU and its member states should help Central Asian countries build transparent market mechanisms, establish electricity exchange trading and advance tariff policy reform. This support should combine regulatory guidance with technical assistance to establish stable legal frameworks that give investors predictability and confidence. In addition, the EU could facilitate cooperation with European transmission system operators and regulators to accelerate alignment with international standards. Together, such measures will unlock investment, improve sector efficiency and strengthen regional energy security.

Protect the infrastructure

All infrastructure projects, from electricity bridges and pipelines to joint hydrogen facilities, will require special protection given Russia’s proximity and the threats it poses to Europe’s energy infrastructure. This demands investing not only in physical security and surveillance but also in strengthening cyber-resilience, which has become a critical vulnerability in the region. Moreover, close coordination with Caspian and Black Sea states will be essential to ensure rapid threat detection, crisis response and long-term safeguarding of critical energy corridors.

Team effort

Central Asia is no longer merely a geopolitical stage for external powers to play their great game. With the difficult post-Soviet years behind it, the region is becoming integrated and increasingly taking charge of its own destiny. This creates an opening for the EU. In the context of Europe’s accelerated decoupling from Russian energy and the broader global competition over supply chains, Central Asia can play a pivotal role in the EU’s energy security and its green transition.

Yet commitments alone do not produce interconnectors, modern grids, processing plants or stable regulatory environments. The central message of this paper is that the EU must convert an improved framework into faster delivery.

With Central Asian states resolving their disputes with each other, combined with Turkey and Azerbaijan increasingly keen on developing the Middle Corridor, the time is ripe for EU to step in. Kazakhstan has already become a major oil supplier to the EU, but renewables are the most promising long-term arena: Central Asia’s solar, wind, geothermal and hydropower potential could support domestic decarbonisation and, over time, exports through Caspian and Black Sea electricity bridge projects.

Meanwhile, the region’s critical raw materials potential is substantial but underutilised. The EU’s current toolbox is stronger than ever, but implementation is lagging. Weak investor protections, fragmented markets, outdated grids, limited regional interconnections, scarce water and slow mobilisation of EU resources constrain progress.

A credible EU role requires a more pragmatic and faster strategy. The EU should start by deepening ties with Kazakhstan and Uzbekistan, the region’s largest and most diverse economies, focusing on renewables and critical raw materials (including processing). It should then scale up institutional and financial engagement, support market reforms and regulatory alignment, and help protect critical infrastructure. By delivering concrete projects rather than aspirational rhetoric, the EU can position itself as a predictable “third force” in Central Asia, supporting stability and sustainable growth while securing diversified energy and value-chain partnerships.

Acknowledgements

The author thanks all his interlocutors from Central Asian countries and those working in EU institutions for engaging discussions on the issues raised in this policy brief. He also expresses special thanks to Taisa Sganzerla for her excellent editing of this policy brief and her invaluable comments, questions and suggestions, which helped him express his thoughts more clearly. The author thanks Nastassia Zenovich for her beautiful visualisations, which made the text more attractive.

About the author

Szymon Kardaś is a senior policy fellow on energy within the European Power programme, based in ECFR’s Warsaw Office.

[1] Data published by Argus Eurasia Energy, March 6th 2025, p. 7.

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.