Don’t look down: How Europeans can escape China’s clean-tech gravity

Summary

- China’s economic approach and trade tactics are dampening the EU’s ambition to become a clean-tech powerhouse.

- The bloc needs to transition from imported fossil fuels to green energy, in order to maintain its strategic independence from other countries. This will be impossible if it can no longer make its own green technologies.

- However, member states differ markedly in their appetite for bolstering European clean-tech firms and climate policy. Their stances reflect how strong their clean-tech sectors are, how much clout old industries have, the country’s exposure to Chinese competition, and public opinion on China and climate change.

- Although a broad group of European political and business leaders agree that China is an economic challenge, they differ on their assessments of the scale and long-term fallout of the problem. This has constrained efforts to build a durable coalition for a more robust European policy response.

- Clarifying trade-offs—through impact scenarios, transparent cost debates and appealing to new constituencies—is essential to creating a shared European approach that strengthens both climate ambition and economic security.

Shooting for the moon

When European Commission president Ursula von der Leyen launched the European Green Deal in 2019, she called it “Europe’s man on the moon moment”. The green deal aimed to create the world’s “first carbon-neutral continent” by 2050. It was a bold vision to remake the EU by transforming the continent’s economy into a sustainable, resource-efficient powerhouse fuelled by home-grown innovation.

Yet as Europeans boarded the “green deal” spaceship for their lunar voyage, they discovered the hull was stamped with “Made in China”—it was not the European craft they had planned for. Steering was faster, but proved trickier. Space debris from Russia and Donald Trump’s America forced a course correction that guzzled precious fuel. Now some Europeans doubt whether the “green moon” is even worth reaching. They see an image in their mind’s eye: an astronaut with a flag in hand to plant on the moon. But the flag is not European: it’s Chinese.

The unease among Europe’s green mission crew reflects a stark choice. The faster the EU advances towards its climate goals, the more it has to depend on other states. The harder it tries to reduce those dependencies, the more politically and economically costly the transition appears.

“De-risking” is a shorthand for curbing reliance on any single source for imports, which, if weaponised, could massively disrupt domestic production, supplies and security. Due to China’s exceptional position in global manufacturing supply chains (in 2023, it accounted for 28% of global manufacturing), the term “single source” has become almost interchangeable with “China”. Chinese technologies underpin the green energy transition. Their solar panels, wind components, batteries and, most notably, electric cars, are so aggressively priced that Europe risks locking itself into a new dependency just as competition intensifies for its indigenous clean-tech industries.

At the same time, the Chinese leadership has demonstrated that it is willing to use coercive trade tactics: from withholding graphite exports to Swedish battery makers, to punitive measures against Australia and Lithuania, and export restrictions of rare-earth elements and permanent magnets for Europe. That means that green technologies are not only tools of decarbonisation, but securing their supply chains is the foundation of the EU’s long-term energy security, industrial leadership and economic resilience—precisely because they free the bloc from dependence on other countries.

However, the European Green Deal faces mounting backlash as legacy industries—from steel to combustion-engine vehicles to the chemical sector—push for rollbacks in response to rising costs and red tape. At the same time, mainstream right-wing and populist parties frame climate policy as the reason for high prices and the decline of European competitiveness.

EU member states vary sharply in their levels of trade and investment with China, the strength of their domestic clean-tech industries, the power of their legacy industries, and the political salience of China and climate policy in national debates. Their readiness to pursue de-risking and economic security policies without stalling the green transition differs accordingly. In many cases, a key issue is underestimating China’s industrial challenge to Europe’s future.

This paper examines these dynamics across five EU member states that provide a balanced geographic representation: Denmark, France, Germany, Italy and Poland. The first part of the analysis will look at the structural and political factors that shape how EU member states navigate the tension between climate ambition and economic security. This will explore the political and economic conditions that shape member states’ willingness to pursue de-risking while maintaining momentum on the green transition.

The paper will then examine the attitudes of major political parties, business groups, trade associations and unions towards the European climate agenda, and China as an economic and security actor. This analysis will shed light on where national debates converge, where they diverge, and where blind spots persist in current European discussions on climate and economic security. It will also reveal how European leaders can move forward to align climate ambition with economic security.

China’s industrial challenge to Europe

China’s industrial dominance is based on a concerted strategy set in motion more than a decade ago. Policies launched under Made in China 2025 and subsequent sectoral roadmaps are now shaping market outcomes at the expense of European business market share and sourcing decisions. Made in China 2025 explicitly aimed for dominance in clean-energy equipment, electric vehicles (EVs) and batteries—goals that have largely been realised.

Chinese leaders centred their strategy on export-led growth based on advanced manufacturing, which they bolstered with coordinated industrial policy and state support. This enabled Chinese firms to achieve scale and cost levels that European producers have struggled to match. And the competition is intensifying. Since last year, Chinese exporters have diverted goods facing trade barriers in the United States to Europe, leading to a new high in the EU’s trade deficit with China in 2025.

This “China shock” will hit Europe’s clean-tech industry hard. The collapse of Europe’s solar manufacturing base is a stark warning. Electric car makers may be next: the sector lost 104,000 jobs in 2024 and 2025. Europe’s pioneering wind sector is also under significant strain and is rapidly losing market share in global markets to Chinese competitors.

There is no evidence that Beijing is going to change course. Its blueprint for the upcoming 15th Five-Year Plan, due in March 2026, signals an intensified push for dominance in strategic manufacturing sectors, including clean energy technologies. Building on Made in China 2025, the new five-year plan prioritises advanced manufacturing, technological self-reliance and rapid domestic deployment. Sectors that include “new energy” (a broad term in China’s policymaking lexicon for clean and renewable energy technologies), new materials, hydrogen and nuclear fusion stand as core growth drivers. They will be propelled by “extraordinary measures” that mobilise state finance, compulsory procurement orders of indigenous technology and preferential support for domestic firms.

On technological self-reliance, the plan explicitly calls for raising the share of government procurement devoted to “self-developed” products, sending a clear “buy Chinese” signal designed to guarantee domestic innovators a protected home market before they compete globally. While Beijing still signals openness to trade, the emphasis on “autonomous and controllable” value chains points to a more restrictive operating environment for foreign firms in strategic sectors.

As Beijing doubles down on plans that will further entrench its dominance in strategic sectors, the case for European de-risking only strengthens. Yet rising costs, tighter fiscal space and mounting domestic resistance to climate policy are making sustained political support for de-risking clean technology and the broader economic security agenda increasingly difficult.

Costs and backlash in Europe

EU efforts to reduce reliance on China—for example through regulation that mandates a minimum percentage of EU-sourced components—have tended to narrow the immediate supplier base and often lead to fewer and more expensive non-Chinese alternatives in the short term. For example, Chinese-made wind turbines cost at least 30% less than European-made ones. Member-state governments and European industry groups have warned that “buy European” procurement rules risk inflating production costs and weakening global competitiveness. Although experience from the telecommunication sector has shown that replacing Chinese equipment in the network would incur minimal cost to the average consumer, at a time when the cost of living is a dominant political concern, these trade-offs are increasingly toxic, especially as public support for climate policy becomes more conditional and fragile.

A strong clean-tech manufacturing base requires not only diversified supply chains but also large export markets to achieve scale. The return of US president Donald Trump and his administration’s hostility toward climate policy have already shrunk one of the most important potential markets for European clean-tech exports: EU exports of batteries, EVs and charging infrastructure to the US dropped to €200m in September 2025, from €1.5bn a year earlier. A more closed or volatile US market will deprive European manufacturers of the scale needed to compete with Chinese producers in clean tech. It also compresses margins and reduces their ability to absorb the short-term costs associated with supply chain diversification.

Domestically too, European leaders face opposition to the Green Deal. In several member states, major political parties are now campaigning explicitly to dismantle elements of the EU’s climate framework, branding climate policy as economically punitive and strategically naive. Dependence on China and fears of industrial decline have been cited in political debates as arguments against phasing out the combustion engine. These dynamics risk turning de-risking from a pillar of Europe’s climate and industrial strategy into a faultline that undermines political support for the transition itself.

De-risking and climate will succeed and fail together

Europeans cannot achieve genuine strategic autonomy or reduce exposure to geopolitical risk without decarbonisation. Unlike the US, the EU is not endowed with abundant domestic fossil resource; unlike China, it cannot rely on large-scale coal production to underpin energy security.

Control over the manufacturing and deployment of clean energy technologies, therefore, becomes a strategic asset in its own right. European leaders cannot afford to lose control over who makes, operates and regulates the key technologies Europe needs, like batteries, solar panels and wind turbines, in the quest to move fast on the energy transition. If Europe rolls these technologies out quickly but deepens structural reliance on a single external supplier, in particular countries that have a record of deploying economic coercion tools, it will weaken its own industries and limit its ability to make independent policy choices.

Besides, if European publics perceive the green transition as hollowing out domestic industry and shifting value creation abroad, it becomes increasingly difficult to defend politically. When voters see factories closing or jobs moving overseas because of Chinese imports, including in clean tech, it could fuel nativist politics and climate scepticism. Climate sceptical politicians have increasingly framed the clean transition as a policy that hands European industries and jobs to China. In this context, cheaper clean technologies and lower energy prices are not enough to build durable support for the transition.

Taken together, these dynamics mean that failure in one agenda will undermine the other. A climate transition that deepens reliance on a single external supplier will weaken industrial capacity and erode political support. A de-risking strategy that neglects the clean energy transition entrenches dependence on energy imports. The two agendas are therefore not competing: they are codependent. Europe’s challenge is recognise that each depends on the other.

The political economy of going green

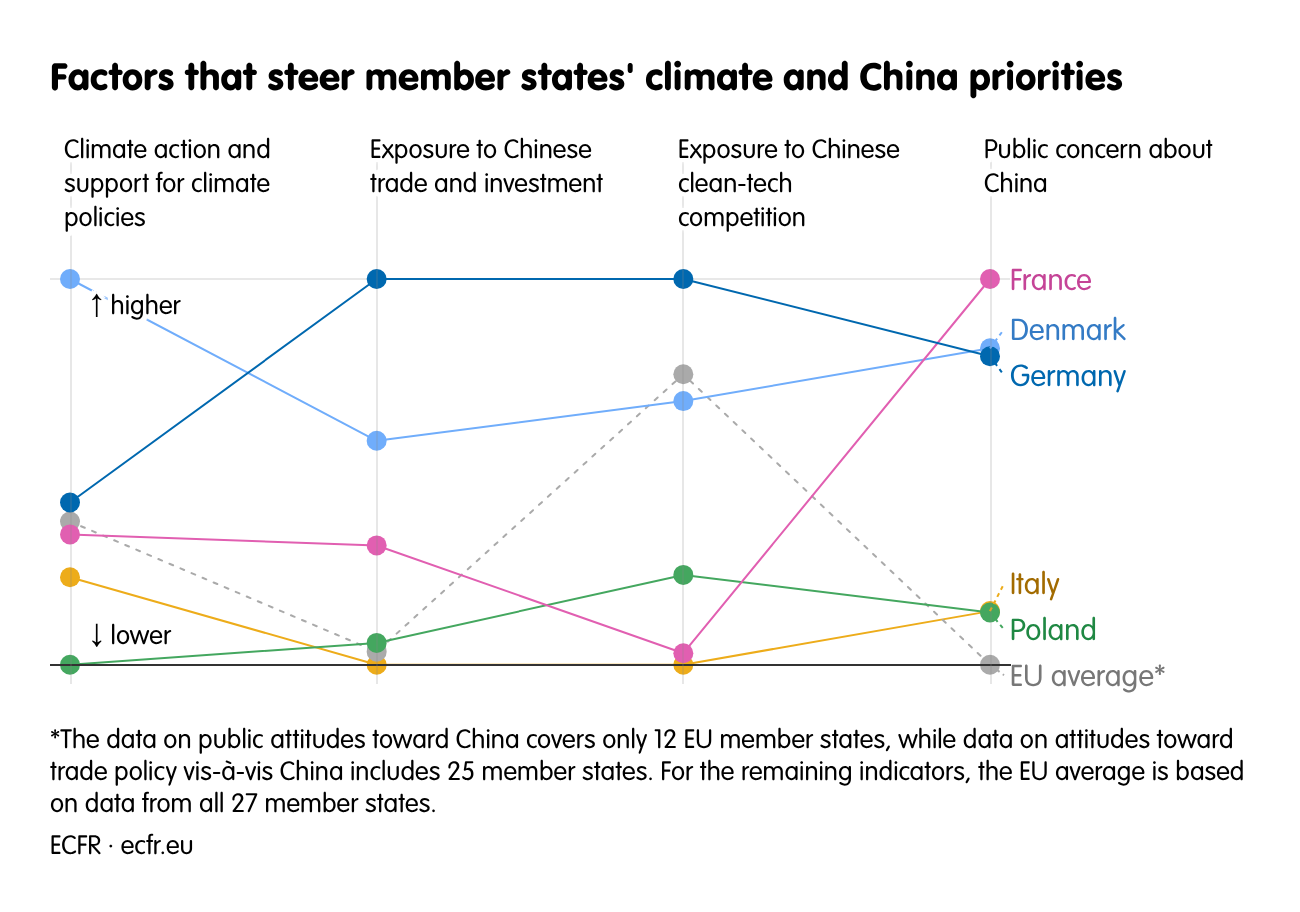

Member states and businesses differ in their stances on going green and cutting reliance on China. Mapping these positions shows where political alliances can emerge to align climate ambition with economic security.

This section maps four factors that influence how EU member states weigh climate ambition against geopolitical and economic risks. These are: how much governments prioritise climate action; their trade and investment ties to China; the competitiveness of domestic clean-tech industries; and public views on China. (Detailed data sources can be found in Annexe 1).

High levels of trade and investment with China make European governments more aware of their strategic vulnerability and wary of taking steps that could provoke economic retaliation. This tension is sharpest in Germany, and to a lesser extent, Denmark, where deep commercial ties with China coexist with growing concern over dependency. By contrast, countries with fewer trade and investment ties with China, such as France, Italy and Poland, align more closely with the EU’s economic security agenda and are more willing to support defensive tools such as tariffs.

Countries with robust clean-tech sectors, such as Denmark, are more likely to see climate ambition and de-risking as complementary. In places where these sectors are weaker, such as Italy, politicians can use scepticism about the cost of climate policy to shield local industry from Chinese competition.

Read more about the factors shaping EU countries’ attitudes

Denmark

Denmark broadly aligns with the EU’s de-risking agenda. All major parties agree Europe needs tougher trade and industrial policies to break free from Chinese supply chains. This stance is reinforced by its world-class clean-tech industry, especially in wind, which is viewed as both a vital asset to defend and a prerequisite for hitting Denmark’s aggressive climate targets.

The problem is that Denmark is highly exposed to China through exports and foreign direct investment (FDI), particularly in pharmaceuticals and shipping, which leaves it vulnerable to Chinese leverage and trade retaliation.

Over the past five years, the Danish government has adopted several measures to reduce economic and security vulnerabilities, including safeguarding critical supply chains, screening FDI, securing telecom infrastructure and restricting research cooperation with “non like-minded states”.

Denmark’s coalition government agrees that Europe must avoid over-reliance on Chinese supply chains for critical technologies and materials, and adopt bolder trade and industrial policies. The centre-left Social Democrats believe that lessons from Europe’s energy dependence on Russia should be applied to its trade relationship with China, calling for “every option in our toolbox”, including state support, to fortify European industries. Coalition partner centre-right Venstre has warned that free trade is “naive” against rule-breaking rivals. Following China’s October 2025 export controls, the Danish foreign minister from the Moderates called on the EU to “flex its muscles” in unified retaliation.

Denmark’s trade and investment ties to China exceed the EU average and top the countries covered in this study, driven primarily by high levels of exports and FDI to China. Denmark is at the forefront of biotechnology and pharmaceutical production, with giants like pharmaceutical Novo Nordisk, which relies on China as both a key consumer market and a supplier. Packaged medicaments and active pharmaceutical ingredients dominate bilateral trade. Chinese demand also drives some 10% the total Danish value added in transportation services, in particular shipping, thanks to shipping giants like Maersk, whose major Chinese port and logistics stakes leave it vulnerable to Beijing’s regulatory whims or coercion.

Despite this high level of exposure, Denmark’s largest business and employers’ association supports using trade defence measures against unfair competition from China. The Confederation of Danish Industry (DI) backs punitive tariffs on Chinese EVs even in the face of Chinese retaliation, while still stressing that a negotiated “peaceful resolution” is preferable to a broader trade conflict.

Climate is high on the Danish political agenda: the government announced in November the world’s most ambitious 2035 climate target. But the urgency to accelerate renewable deployment and the adoption of lower-cost Chinese clean tech will be weighed against protecting Denmark’s vital wind industry, which makes a significant contribution to local jobs and the economy. Danish wind firms warn that without state support, local content requirements and trade protection measures, Europe risks replicating its dire experience in solar manufacturing, where Chinese competition nearly wiped out the domestic industry.

Italy

China is not a central foreign policy priority for Italy, but Rome has gradually aligned more closely with European approaches. While open to business with China, Italy has taken selective steps against unfair competition, supply chain dependency and Chinese involvement in strategic sectors. With modest trade and investment ties to China and a tepid climate stance, the government is primed to favour protecting local industry from Chinese competition, even if this slows the green transition.

The Italian government lacks a formal China policy, but its approach has grown more guarded, shaped by concerns over unfair competition, supply chain dependency and Chinese presence in strategic sectors. Ministers have openly warned about the impact of Chinese overcapacity on Italian manufacturing, and Italy voted in favour of the European Commission’s proposal in 2024 to impose tariffs on Chinese EVs, a view that is shared by the largest business association in Italy and also the Italian public.[1]

Italy’s overall exposure to Chinese trade and investment is limited. Chinese FDI accounted for a mere 0.02% of GDP in 2024. However, risks are concentrated in specific sectors. Apparel and textiles, which accounts for 5.1% of Italian GDP, form over a quarter of its exports to China. Weak Chinese consumer demand for luxury goods and competition from low-cost Chinese online imports have battered the fashion sector. These sector-specific dependencies make Italy vulnerable to Chinese retaliation and constrain Rome from pursuing tougher economic security measures against Beijing.

Chinese companies have stakes in Italian infrastructure, including seaports and energy grids. Most investment flowed in before Italy tightened its FDI screening mechanism via the “Golden Power” law, which the Draghi and Meloni governments wielded to restrict or veto Chinese investments in semiconductors, telecommunications and tyre production. More recently, Rome issued a signed decree establishing preferential criteria for procuring IT tech developed in EU and NATO member states to cut reliance on Chinese companies for critical technologies.

While senior figures in the governing coalition, including current prime minister Giorgia Meloni and foreign minister Antonio Tajani, viewed Italy’s 2023 decision to exit China’s Belt and Road Initiative as a mistake, the government had carefully managed the move to avoid a rupture in bilateral relations. Rome maintained high-level engagement with Beijing and renewed strategic partnership agreements shortly thereafter, underlining the government’s intention to balance political signalling with continued economic cooperation, and to avoid the risk of retaliation.

The Italian government’s approach is to secure the economic benefits of Chinese investment without becoming overly dependent on China in critical sectors. On the one hand, the government has actively encouraged Chinese carmakers to establish production facilities in Italy, but with strict cyber and local content conditions. On the other hand, Rome has introduced public tenders for solar energy projects that exclude Chinese solar modules, cells and inverters, designed to de-risk supply chains and support EU producers.

However, the government’s cautious climate stance could make it more inclined to support trade or industrial policies that shield domestic industry from Chinese competition, even if such measures slow down the green transition. The government does not oppose climate action in principle but is sceptical of the pace and cost of the EU’s climate agenda, which it fears will hurt Europe’s industrial capacity and competitiveness. Senior ministers have described elements of the Green Deal as “ideological” and warned that it risks becoming a “commercial, industrial and environmental suicide”. The government has pushed back against the EU’s 2035 ban on internal combustion engines and the target to cut emissions by 90%. Meloni argues that the 2035 ban is “wrong on industrial and also geopolitical levels” since China controls much of the electric vehicle supply chain.

Poland

Neither China nor climate ranks among the top political priorities in Warsaw. Poland has played a modest role in shaping the EU’s China policy but has not opposed the bloc’s increasing assertiveness. The country does not trade heavily with China, but it has received notable levels of Chinese FDI and its automotive supply chains are vulnerable to Chinese competition.

At the same time, Poland has a fast-growing clean-tech sector and a strong manufacturing base. Although it seeks to benefit from Chinese partnerships in areas such as EVs and renewables, Russia’s invasion of Ukraine has made it wary of overdependence. As a result, Poland is likely to support trade instruments that protect both national and EU industries from unfair competition and undesirable dependency on China.

Russia’s full-scale invasion of Ukraine changed how Polish politicians view China. Officials from the Civic Coalition (KO), the main centre-right political alliance and current ruling party, have warned that China should end any support for Russia or face economic consequences, calling China a “quiet player” in the conflict. In September 2025, the Polish government closed its eastern border with Belarus in response to Russia-led military exercises, disrupting some 90% of EU rail trade with China. This reflects a shift in its policy towards China, where security now outweighs trade.

Despite this shift, the government has not yet outlined an official China strategy. It quietly backs the EU’s more guarded stance towards China, while avoiding public confrontation. Warsaw has not opposed EU initiatives on economic security and the de-risking toolbox, and even voted in favour of the commission’s proposal to impose tariffs on Chinese EVs. Domestic de-risking efforts focus on limiting China’s presence in critical sectors, like telecommunication and pharmaceuticals.

Chinese direct investment in Poland accounts for 0.15% of the country’s GDP, one of the highest among the five countries surveyed. The Polish government has increased its scrutiny of infrastructure investments in recent years. A case in point is the long-term lease of the Gdynia port terminal to the Hong Kong-backed Hutchison Port Holdings. The leasing was controversial because of the port’s proximity to NATO naval bases, Poland’s main port and defence facilities. The government subsequently designated Gdynia as critical infrastructure, which allows authorities to impose stricter security rules, monitor operations more closely and potentially intervene in crises.

Poland also plans to systematically phase out Chinese telecommunications equipment from its 5G networks, where companies such as Huawei and ZTE hold a 45% market share.

Although Poland does not rely on China for exports, it tops the five surveyed countries in import dependence. Chinese goods form a big slice of total imports. While these imports are largely concentrated in non-critical sectors such as electronics, machinery and textiles, Poland is also highly dependent on China for active pharmaceutical ingredients. The health ministry has proposed subsidies for drugs whose ingredients are produced in Poland to address this.

Poland faces stiff competition from Chinese clean tech, putting many jobs at risk. It is the largest manufacturer of light vehicles in central and eastern Europe and boasts a growing wind sector that rivals Denmark’s in employment. Together, these two sectors employ 305,000 people, roughly 9% of all manufacturing jobs in the country, mostly in motor vehicles. That leaves Poland second only to Germany in exposure among the countries studied. This has prompted the government to provide more support for domestic supply chains in the wind sector, favouring Polish firms and local content.

Poland’s car sector is responding to competition from imported Chinese EVs by localising higher value-added activities through tech partnerships with Chinese companies. Polish automotive stakeholders therefore opposed the government’s backing of EU tariffs on Chinese EVs, warning that such measures could undermine investment and market access. Indeed, Chinese EV manufacturer Leapmotor, which operates the Tychy plant in Poland through a venture with Franco-Italian automaker Stellantis, paused production of its T03 model after the tariff vote.

Chinese investment to date has largely been focused on assembly, adding limited value to the economy. Before the pause in operation, the Tychy plant was making “European” Chinese EVs from imported kits, bypassing local suppliers. Poland’s car industry may not welcome this outcome because—however modest its value—every scrap of business counts. Yet this business model is far from optimal for the country as a whole.

Germany

Germany’s high exposure to Chinese trade and FDI, and competition on clean tech, both drive and limit its pursuit of a European economic security agenda. Its industries, particularly car makers, have deep economic ties with China. Their lobbying, and divisions among political parties, complicate the formulation of a coherent policy on economic security and climate.

But the industrial pressure from Chinese competition is shifting perceptions on the economic risks from China, especially among small and medium-sized businesses. Recent supply disruptions on rare earths and permanent magnets, and fiercer competition, have strengthened the case for reducing critical dependencies. The public is sceptical of China, which creates room for tougher rhetoric and selective defensive measures. Still, the government may baulk at bolder trade measures that could harm its most globally (or China-) exposed companies.

Germany is one of the countries most vulnerable to China and stands to lose the most from intensifying competition from Chinese products, including in clean technologies. Developments in 2025 show that these risks are no longer theoretical. China’s export controls on rare earths, permanent magnets and semiconductors—nominally aimed at America—laid bare Germany’s position, prompting warnings from the German automotive association that prolonged controls could halt car production. Medical technology companies, electronics and auto firms have already scaled back or suspended production. Indeed, engineering and technology firm Bosch has reported disruptions at three German production sites due to chip shortages linked to China.

Chinese FDI in Germany accounted for 0.15% of the country’s GDP in 2023, leaving its critical infrastructure among the EU’s most vulnerable to Chinese influence. For example, Chinese kit dominates 5G networks. Germany’s coalition government is now screening Chinese FDI more aggressively, excluding Chinese vendors from future 6G networks and purging existing networks of Chinese equipment. It also now supports supply chain diversification in the wind sector—the largest in Europe by jobs and output—with a “resilience roadmap” that says that 30% of permanent magnets should come from alternative sources by 2030. Political scrutiny even led a German wind developer to drop a planned turbine deal with a Chinese supplier.

Despite these measures, Germany remains vulnerable. China was Germany’s largest trading partner for most of the past decade, until America overtook it in 2024 amid a 3.1% decline in China-Germany trade, which likely marks the start of a lasting slump. The Centre for European Reform calculates that falling exports to China have already cost Germany around 0.5% of GDP, a trend likely to intensify as China doubles down on an export-led model targeting advanced manufactured goods that directly compete with Germany’s industrial base.

German companies accounted for roughly 60% of EU FDI into China from 2022 to 2024, driven largely by car industry deals. Major German manufacturers, such as BMW and Volkswagen, have pressed ahead with EV investments in China despite losing market share and profitability there.

The clash between protecting business and pursuing economic security looms largest in Germany’s debate over trade protection. The last coalition government was divided over imposing tariffs on Chinese EVs. German carmakers and their industry association opposed the tariffs because they are deeply reliant on the Chinese market for sales, profits and sourcing of components, and are concerned that potential Chinese retaliation could impose greater costs than the benefits from the tariffs.

By contrast, Germany’s Mechanical Engineering Industry Association (VDMA), which represents small and medium-sized mechanical and plant engineering companies, now demands strong protection measures, including local-content rules and tariffs, to correct “China’s aggressive economic and trade policy”. Unlike large national business associations, whose members are deeply invested in Chinese supply chains, they are less exposed to retaliation but face fiercer undercutting by Chinese competition. German machinery manufacturers have lost significant ground in China, with their share of the import market shrinking from 20.4% in 2015 to just 15.1% in 2024. As a result, they are more willing to support assertive economic security measures, including trade defence tools and local content requirements, to shield the domestic industry from unfair competition.

Germany has an ambitious national target of climate neutrality by 2045, yet public support for climate spending is only average by EU standards. Roughly a third of Germans believe that climate should be among the EU’s top four budget priorities. Business opposition, particularly from the automotive sector, has pushed Berlin to lobby for greater flexibility in the EU’s planned 2035 ban on new combustion engine vehicles, exposing the rift between green goals and industrial muscle. The government will struggle to accelerate Germany’s clean policy in the short term. Emissions reductions slowed to modest levels in 2025 amid calls for regulatory rollbacks and new fossil fuel infrastructure. The government will continue to face difficult coalition politics where partners like Bavaria’s powerful Christian Social Union (CSU), led vocally by Markus Söder, openly frames climate action as antithetical to industrial competitiveness and jobs.

France

France pairs keen economic and political engagement with China with a strong commitment to European resilience. Paris, a champion of strategic autonomy, supports EU measures to safeguard the bloc’s industrial competitiveness against Chinese pressure—emboldened by public scepticism of China (among Europe’s highest) and its strong taste for tough trade measures.

Compared to Denmark and Germany, France has significantly lower exposure to Chinese trade, investment and clean-tech competition. As such, France faces fewer domestic constraints in wielding defensive tools. While climate policy does not rank among the highest priorities for either the government or public, France maintains a solid foundation of existing policies that help sustain its climate agenda.

China is France’s largest non-EU trading partner, but its exposure through direct investment is relatively modest. President Emmanuel Macron sees China as creating significant global economic risks through its “unsustainable” trade surplus. Macron, in fact, threatened Beijing with tariffs if the trade deficit was not addressed, stating that Europeans would be forced to take strong measures. The government has long advocated for the adoption of preference for European firms in strategic industries and public procurement. France’s largest employers’ and business association, (Mouvement des Entreprises de France (MEDEF) has called for the creation of a “Buy European Act” and bolder trade policies.

France has been an early and staunch proponent of the EU’s economic security framework and de-risking agenda, in line with its quest for strategic autonomy from both China and America. The government strengthened FDI screening, extending it to critical raw materials, to protect national interests. While France enacted legislation to limit Huawei’s role in 5G, Chinese vendors still provide about 13% of network infrastructure, and Chinese firms hold minority stakes in several major French ports. French officials stress that realistic de-risking is the goal, not decoupling.

While Macron positioned climate action as a structural priority when he was first elected, and created a dedicated ministerial role for ecological planning after his re-election in 2022, this emphasis has softened over time. Industrial competitiveness, cost pressures, and concerns about social and political backlash, particularly amid the rise of the far right, have increasingly shaped the government’s approach. Macron has even called for a “European regulatory pause” and to scale back EU sustainability reporting regulations.

France supports broader EU initiatives, such as the Green Deal Industrial Plan and the Critical Raw Materials Act, while rolling out its national “France 2030” strategy. A key element of the initiative is reducing reliance on China-controlled critical supply chains by investing domestically and across Europe to secure sources of critical raw materials, such as funding lithium mining projects in France and sourcing nickel from New Caledonia. The development of a “battery valley” in Dunkirk, for example, is intended to secure France’s position in the European EV supply chain, as are initiatives to promote domestic production of rare earth magnets (eg, the “magnet valley” project in Lacq).

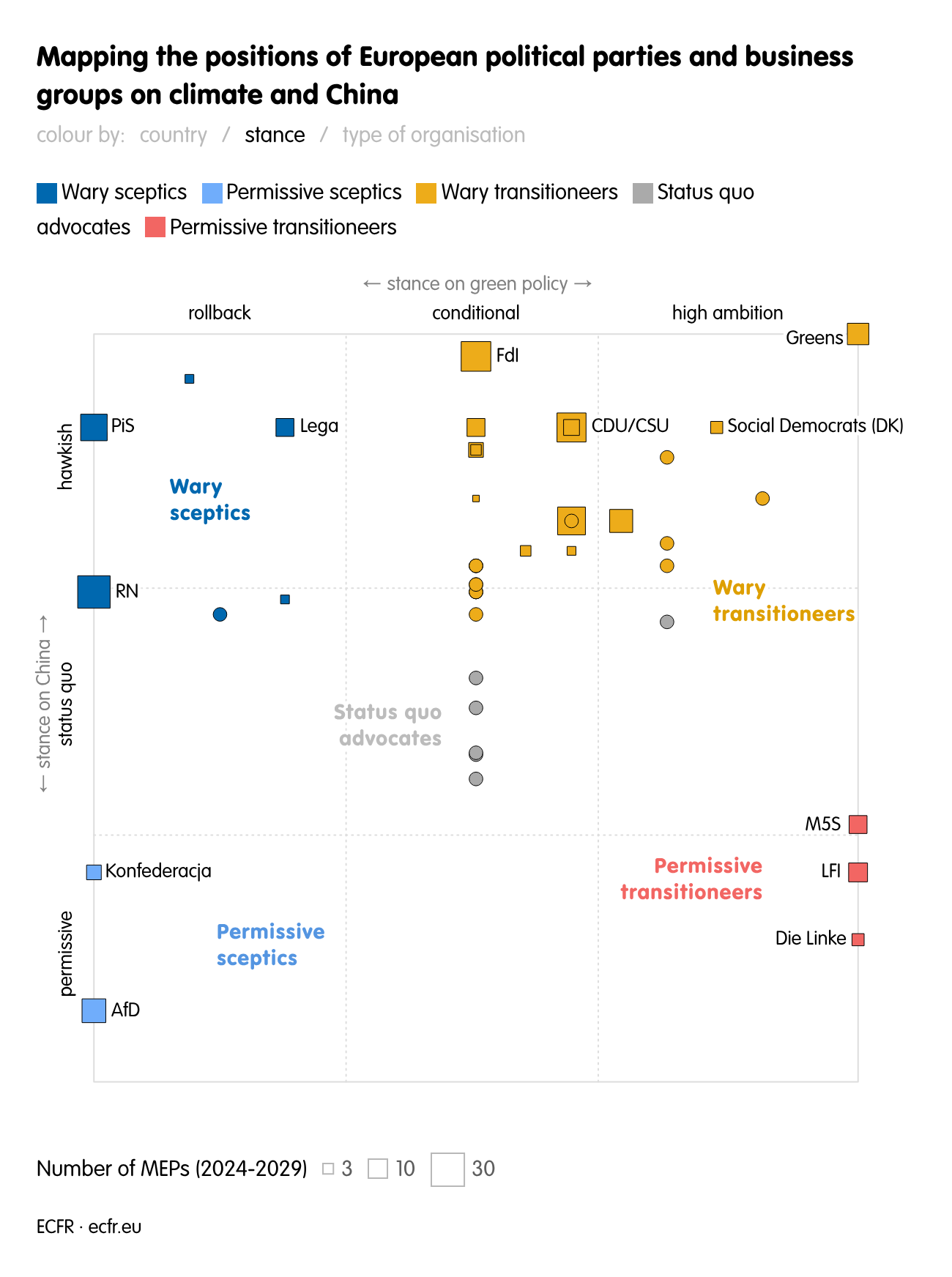

Coalition mapping

This section maps how political parties, business groups, trade associations and advocacy organisations position themselves along the de-risking/China axis, and where coalitions can form or fracture. Actors fall into four broad camps based on how they balance climate ambition with their stance towards China.

Read more about the political mapping here

Status quo advocates

The first camp is the “status quo advocates”—those political parties or business groups that broadly accept the EU’s climate objectives and acknowledge the risks from Chinese competition and dependency. However, they favour incremental adjustments over structural overhaul, prioritising near-term competitiveness and stability in existing trade relations.

A number of industry and employer associations across the countries analysed fall into this camp, including the Danish Employers Association, Germany’s VDMA and the Polish Confederation Lewiatan. Their support for the climate agenda is conditional on measures that preserve their near-term competitive position, and their approach to China is primarily economic rather than political or security focused. As a result, while they broadly accept the risks, the remedies they propose are incremental and largely defend the status quo. They frame Europe’s regulatory and administrative burden as a challenge on par with the competitive and supply chain pressures stemming from China. They emphasise the use of market-based instruments to achieve climate goals, call for regulatory simplification, and argue that the EU’s trade and industrial policy tools should not be targeted at specific countries.

Automotive lobbies in this group, including the Polish Automotive Industry Association (PZPM) and Germany’s VDMA consistently oppose tariffs and countervailing duties, fearing that retaliation would cost them “more in China than they gain in Europe”. The VDMA, for example, decries tariffs on Chinese EVs, saying that they raise costs for consumers and slow the rollout of electromobility.

Although these groups back decarbonisation in principle, they decry the EU’s climate framework as premature and competitiveness-sapping. They have lobbied for technological neutrality, meaning that the government should not exclude a broad mix of “cleaner” energy options, such as nuclear power and synthetic fuels, alongside renewables, in achieving the energy transition.

Wary transitioneer

The “wary transitioneer” camp is the largest group in this analysis. It reflects the mainstream position on China and climate policy in the geographic scope of this analysis. The camp contains groups that support decarbonisation while favouring measures to reduce strategic dependence on China. Its members see the two agendas as mutually reinforcing but politically delicate. Most governing parties in all five countries fall into this category, alongside business and industry groups, particularly those representing clean energy sectors. What unites them is a shared assessment that China poses not only economic risk, but also national security and energy security risks for Europe. On climate, they form a broad church of a “transitioneer” coalition: they span from advocates to pragmatists and are united in their backing on climate policies—albeit with varying speed, ambition and conditions.

They are “wary” because they see China not only as an economic rival but as a geopolitical threat to European interests. For the political parties in this group, China’s military expansion, assertive behaviour in the South China Sea and support for Russia’s war in Ukraine reinforce perceptions of China as a security challenge. As a result, they are wary about Chinese stakes in critical infrastructure and strategic sectors, including EVs, telecommunication, ports and wind energy, and support closer scrutiny of Chinese participation in those areas.

There is also broad agreement that Chinese subsidies, overcapacity and state-backed industrial policy threaten Europe’s industrial edge. This underpins support for EU trade defence and economic security instruments. While not all actors explicitly supported tariffs on Chinese EVs in 2024, they broadly back various remedies—such as local content preferences, anti-dumping and countervailing duties, non-price procurement criteria and foreign subsidy investigations—to restore fair competition in the single market. French and Danish business groups, including France’s Automotive Platform, the French Confederation of Small and Medium Enterprises (CPME) and the DI, demand safeguards, such as tariffs or local-content rules, to restore fair competition. Germany’s largest business and industry association, the Federation of German Industries (BDI), falls into this camp.

Wary transitioneers support green goals in principle and do not seek to dismantle EU or national climate frameworks. They differ both from outright climate sceptics and from those advocating scrapping the Green Deal or abandoning emissions targets. Instead, they encompass a wide spectrum: from actors pushing to go beyond current EU and national targets to those who condition support for the climate agenda on “flexibility measures”, such as delaying elements of emissions trading expansion, providing stronger financial support, or embracing technological options such as nuclear power, synthetic fuels and hybrid vehicles. Though some actors in this group, such as Meloni’s Brothers of Italy (FdI), are no green champions, they form the core pan-European coalition willing to preserve the climate agenda against rising scepticism.

Wary sceptics

The “wary sceptic” camp combines a defensive posture towards China with scepticism towards the EU’s climate agenda. They argue that green policies have weakened European industry and left it exposed to unfair competition. The camp includes right-leaning populist parties and select business groups that combine a hawkish view of China with scepticism towards the EU’s climate agenda. What binds them is a double defensive posture: strong concern about China as an economic and security threat, and opposition to EU climate policies that they see as undermining competitiveness.

This camp agrees that competition with China is neither fair nor market based. They see Chinese state subsidies, overcapacity and industrial strength as a threat to Europe’s factories and jobs. Without defences, they warn, Chinese products will flood the market and hollow out European industry. Poland’s Law and Justice party (PiS) has explicitly linked this argument to the EU’s climate agenda, claiming that the Green Deal is financing Chinese industries and destroying European jobs.

Their caution towards China is driven less by concerns about human rights, which receive limited attention, and more by those around security and resilience. Political parties in this group, such as Denmark’s Democrats (DD), France’s National Rally (RN) and Italy’s Lega, consistently sound the alarm about Chinese involvement in critical infrastructure. This is particularly in transport and energy infrastructure, but also increasingly about Europe’s industrial supply chains. In Poland, this is framed through a Russian lens: PiS is warning Europe against repeating “the same mistake that was made with Russia”, in which Europeans assume that deep economic interdependence with China guarantees security or stability.

The wary sceptics broadly oppose the EU’s climate agenda. They push to roll back or delay key legislative files, such as expanding emissions trading to buildings and transport, and the 2035 ban on internal combustion engine vehicles. Right-wing populist parties cast their opposition in ideological, sovereignty and cost-of-living terms, describing EU climate policy as a “punitive ecology” that hikes prices for ordinary citizens, undermines national autonomy and invites “less Europe” rather than pragmatic environmental protection.

Permissive transitioneers

Groups that prioritise rapid climate action and are more open to economic engagement with China fall into the “permissive transitioneers” camp. They view access to low-cost clean technologies as essential to accelerating the transition.

This group comprises political parties regarded as left-wing, including La France Insoumise (LFI), Germany’s Die Linke (The Left), and Italy’s Five Star Movement (M5S). Despite their differences, they are united by an uncompromising commitment to ambitious climate action.

Permissive transitioneers champion the EU’s green agenda, urging the overshooting of existing EU targets, including faster deployment of renewables and stricter emissions cuts. They support a rapid phase-out of internal combustion engines and treat climate policy as a tool for economic and social transformation. However, their eco-socialist orientation leads them to spurn market-based instruments such as the EU Emissions Trading System, which they decry as socially unjust taxes that hit households harder than large emitters.

Their openness to China dovetails with this decarbonisation agenda. Without Beijing’s clean-tech cooperation, they say, Europe cannot pull off a swift energy transition—and add that Chinese investment in renewables could boost European manufacturing capacity. Die Linke, for example, has emphasised localised production for environmental and social reasons. Notably, France’s LFI, despite its generally permissive stance towards China—including calls to reopen EU-China negotiations under the Comprehensive Agreement on Investment and towing Beijing’s line on Taiwan—has called for 100% tariffs on Chinese electric vehicle imports and public subsidies to protect the French automotive industry. This suggests that even among climate-friendly political groups, there is growing recognition that access to cheaper clean technologies alone is insufficient to sustain durable political support for the transition.

Security thinking within the permissive transitioneers is shaped by an aversion to confrontation. Increased Western military presence in the Indo-Pacific is framed as “unnecessary provocation”. Actions such as US house speaker Nancy Pelosi’s 2022 visit to Taiwan were portrayed as a deliberate provocation that heightened tensions rather than enhanced security.

This perspective meshes with a broader transatlantic scepticism that feeds their relatively soft line towards China. China is often framed in contrast to the US, particularly in climate policy debates, through a narrative of “imperialism on one side, ecological pacifism on the other”. Criticism of China’s human rights record gets defused by redirecting attention towards US foreign policy or Europe’s colonial past, portraying China less as an aggressor and more as a victim.

Permissive sceptics

This is the smallest of the four groups and includes only two far-right political parties: the Alternative for Germany (AfD) and Poland’s Confederation Liberty and Independence (Konfederacja). It contains no business or industry organisations. Permissive sceptics reject the EU’s climate policy agenda outright, often questioning or dismissing climate science, while simultaneously advocating the preservation or expansion of economic ties with China.

Their position rests on economic priorities and faith in competition. Climate policy is portrayed as economically destructive, raising consumer prices and undermining European competitiveness. The EU’s carbon pricing instruments, such as the Emissions Trading System (ETS) and the Carbon Border Adjustment Mechanism (CBAM), are cast as heavy burdens on industry and as drivers of economic downturns. In contrast, this camp presents engagement with China as sound business; its tech rise is an opportunity, rather than threat.

Ideology and sovereignty fuel this camp’s outright rejection of EU climate policy. They depict climate measures consistently as ideologically driven, branding the Green Deal as “economic suicide” or an “eco-socialist redistributive machinery”. The group has even tried to scrap climate legislation entirely. Energy sovereignty is emphasised over decarbonisation, with support for a “technologically neutral” approach that keeps coal and other fossil fuels in the energy mix. Human rights concerns are dismissed as irrelevant or counterproductive, reinforcing a permissive stance towards China.

Permissive sceptics see no security threat from China and resist hawkish Western foreign policy. They reject claims that China materially supports Russia, and frame tensions over Taiwan and Ukraine as the result of great-power rivalry driven primarily by America. Economic disruption, rather than security risk, is presented as the main danger of confronting Beijing.

Although marginal in mainstream climate and China policy debates, this group commands significant electoral support. The AfD currently leads in opinion polls in Germany, while Konfederacja is the second-largest opposition force in Poland. Their political relevance should therefore not be underestimated, despite their otherwise isolated policy positions.

How to forge coalitions for economic security

Bridge mainstream politics and business

Across the five countries analysed, most governing parties sit firmly in the wary transitioneer camp, alongside many mainstream business and industry groups. There is broad agreement that Chinese overcapacity, state subsidies and structural dependencies pose a serious threat to European industry. In principle, this group supports a wide range of economic security tools: from classic trade defences such as tariffs and foreign subsidy probes to non-price criteria in public procurement, local content requirements and tighter conditions on Chinese investment.

Yet, this shared diagnosis and nominal support for these toolshave failed to generate a reliable coalition, at least among the countries analysed in this report. They have not been able to sustain political support for climate ambition and a coherent strategy that advances a robust economic security agenda towards China.

The main point of divergence lies in how actors interpret China’s role and intentions. Those who view China primarily as an economic competitor fixate on the short-term cost of European industrial policy and a “negotiated solution” to restore balance, which curbs their appetite for assertive trade and economic security measures. In contrast, those who see China more as a strategic and security player stress the longer-term political, economic and security consequences of ongoing dependence. These differences shape tolerance for costs, retaliation and the competitiveness impact of de-risking measures—in turn constraining political willingness to act.

The challenge in building a coalition is therefore not a lack of tools or concern, but the absence of a shared understanding of the problem across time horizons, and of the broader economic, political and security repercussions beyond immediate costs.

A good starting point for building coalitions is to align political and business actors around a shared, forward-looking understanding of China’s stated policy goals and their implications for Europe. This demands clarity on its five-year plan priorities—industrial, economic, security goals, climate and clean technology deployment targets—and how these tilt competitive dynamics for European businesses at home, in China and globally. Elaborating scenarios of what will happen if Europe fails to counter sustained Chinese dominance across key industrial sectors, including clean technologies, can help make the longer-term risks more vivid and galvanise action.

Much of the industrial pressure now confronting European governments and firms was signalled years ahead, through initiatives such as Made in China 2025 and China’s dual circulation strategy, serving as a reminder of the costs of delayed recognition and the limits of reactive coalition-building.

Have an honest debate about costs

This does not mean that short-term costs can be set aside. Figuring out how to address these outlays is central to sustaining political and financial support for climate policy and de-risking. Opposition to each now increasingly pivots around cost, albeit for different ideological and economic reasons. Right-wing critics depict green measures as an elite imposition that burdens ordinary folk; left-wingers assail carbon pricing as a capitalist ploy with a regressive sting, hitting low-income households hardest since they devote more of their earnings to energy.

De-risking stirs unease among businesses and consumers over who foots the “resilience premium” from supply chain diversification and local sourcing—and how these costs ripple into prices. Businesses do not want to be the “first movers” in diversification and there is little appetite in the market for paying more for European-made components without protective measures. These are not ideological rifts but hard economic questions that merit serious political debate and rigorous research. Addressing them transparently, through clearer distributional choices, targeted compensation and a candid tally of the long-term toll of inaction, is a precondition for building a coalition that can support both decarbonisation and economic security over time. It also helps establish a credible “business case” in which European firms can justify higher short-term costs of de-risking in return for a long-term resilience dividends.

Speak their language

Populist parties are united in their support for fossil fuels and their fierce criticism of the climate agenda, but their views on China vary widely and do not map neatly onto the traditional left/right spectrum. Far left and far right alike tilt towards Beijing, albeit for different reasons. On the left, permissive stances often reflect a desire to distance Europe from an erratic, climate-sceptic America and to treat China as a necessary partner for global decarbonisation and governance. On the right, openness to China is more often linked to admiration for its governance model and rejection of liberal norms.

While it may be unrealistic to expect many right-wing populist parties to support ambitious climate policy, understanding the logic behind their positions on China could be a path towards creating workable coalitions around policies of the economic security agenda. Europe’s ability to sustain a coherent foreign policy, including towards China, will depend on building new domestic majorities rather than on mainstream parties clinging onto shrinking voter bases. For the permissive parties on the left, economic security can be pitched as essential to safeguard the green transition from supply chain disruptions and trade coercion. For the permissives on the right, economic security should be a matter of industrial and energy sovereignty and policies that boost domestic industries.

The green moonshot

As Europe’s green mission hurtles towards von der Leyen’s 2050 moonshot of a carbon-neutral continent, how member states and economic actors navigate the trade-offs between decarbonisation and de-risking will affect the mission’s speed and determine Europe’s long-term resilience.

Leadership in clean technology—solar, wind, batteries and more—will dictate where value accrues, who sets global standards and who wields strategic clout, and not just the mission’s pace. Without such capabilities, Europeans court a future as price-takers and rule-takers in a green technology universe moulded by China. Fail, and the flag planted on the green moon will bear China’s red—not Europe’s blue.

Methodology

Annexe 1. Approach behind “Factors that steer member states’ climate and China priorities”

Climate policy and politics

Countries that score higher on this indicator tend to prioritise climate in both public policy and political discourse. In these countries, climate is high on the agenda despite competing imperatives such as de-risking or industrial competitiveness. The author used the following metrics to provide a score:

- The progressiveness of national climate policies, diplomacy, greenhouse gas reduction and energy trends. They are based on the Climate Change Performance Index.

- Public opinion on climate as a national policy priority. This metric is based on Standard Eurobarometer 103, spring 2025.

- Public support for climate as a priority in the EU budget. It is based on Standard Eurobarometer 103, spring 2025.

Exposure to Chinese trade and investment

Countries with greater economic exposure to China through trade and investment are more vulnerable to potential disruptions if Beijing leverages those dependencies. As a result, they may be more cautious or constrained when implementing de-risking measures that could provoke retaliation. The author has used the following metrics to quantify exposure:

- Imports from and exports to China as a share of total extra-EU27 trade. It is based on Eurostat data on international trade in goods.

- Inbound and outbound FDI from and in China as a share of the country’s GDP. It is based on Eurostat data on EU direct investments and GDP and components.

Exposure to competition from Chinese clean-tech firms

Countries that score higher on this indicator have a larger share of jobs and economic value in sectors that directly compete with Chinese clean-tech industries. This makes them more likely to support assertive trade and industrial policy responses, such as defensive trade measures or targeted industrial support, to counter unfair competition. The author has used the following metrics to quantify exposure:

- Share of wind industry jobs as a percentage of total manufacturing employment. This is based on IRENA data on renewable energy employment by country and Eurostat data on employment in national accounts.

- Share of automotive manufacturing jobs as a percentage of total manufacturing employment. This is based on Eurostat data on employment in national accounts.

- Value added (as a percentage of GDP) in manufacturing activities related to renewable energy production. This is based on Eurostat data on the environmental goods and services sector and GDP and components.

Public concern about China

Countries scoring higher on this indicator have publics that are more sceptical or hostile toward China, and tend to support tougher trade and industrial policies to reduce economic dependence and protect European markets. These sentiments provide greater political space for governments to adopt more assertive positions towards Beijing. The author has used the following metrics to quantify the indicator:

- The percentage of the public that views China as a rival or adversary to the EU. This is based on an ECFR survey conducted in November and December 2024. The EU average represents data from Bulgaria, Denmark, Estonia, France, Germany, Hungary, Italy, Poland, Portugal, Romania, Spain, Ukraine and the United Kingdom.

- Support for trade agreements aimed at reducing reliance on China. This is based on a Project Tempo survey conducted in August and September 2024.

- Support for higher tariffs on Chinese EVs. This is based on Project Tempo survey conducted in August and September 2024.

Scoring system (0–1)

For each issue, scores are assigned on a 0–1 scale, where 0 reflects the lower end of each issue and 1 reflects the higher end, based on relative exposure, concern or political salience across countries.

For each issue area, the final country score is calculated as the average of all indicators within that issue. All indicators within an issue are weighted equally.

Annexe 2. Approach to “Mapping the positions of European political parties and business groups on climate and China”

To assess how key political parties, business groups, unions, think-tanks and climate advocates position themselves within Europe’s climate-industrial realignment, ECFR used a two-axis framework. This framework captures each actor’s relative support for EU climate action and their strategic posture toward China.

Each stakeholder is scored on the basis of their position on a defined list of policy agendas, drawn from public sources, including manifestos, policy documents, interviews, parliamentary activity and media statements. Scores range from 0 (low alignment) to 2 (high alignment) along each axis.

Axis 1: Support for climate action

This axis captures how strongly actors support core components of the EU’s climate policy framework. Stakeholders are assessed across four specific issues:

- Simplification agenda: Their position on efforts to streamline EU climate regulation, including on permits, administrative processes and reporting burdens.

- EU climate target: Their position on the commission’s proposed target of a 90% reduction in emissions by 2040.

- Technological neutrality: Their position on technological flexibility. For example, whether they advocate for a flexible mix of clean technologies (eg, carbon capture and storage, nuclear, battery, EVs) or push for specific solutions (eg, renewables only, hybrids, e-fuel) in reaching energy and mobility electrification targets.

- CBAM and ETS expansion: Their position on strengthening the EU ETS and implementing the CBAM as part of the green industrial transition.

Scoring system (0–2)

- 0 – Low ambition/pro-rollback: Opposes core instruments or targets.

- 1 – Moderate or conditional ambition: Accepts climate policy direction but calls for exemptions and policy flexibilities.

- 2 – High ambition/pro-green transition: Supports higher ambition in EU or domestic climate targets and tools.

The climate axis score is the average of the four issue scores.

Axis 2: Strategic assertiveness on China

This axis reflects how actors engage with China as a geopolitical and economic force. It incorporates both security-related and economic policy positioning, based on the following dimensions:

Security and governance

- China’s global security posture (eg, Ukraine, Taiwan, South China Sea).

- China’s geopolitical influence (eg, Belt and Road Initiative).

- Human rights and political system (eg, Xinjiang, surveillance).

- Chinese involvement in critical infrastructure (eg, Huawei, ports, energy systems).

Economic and industrial issues

- Assessment of Chinese overcapacity and market distortion.

- Support for EU trade defence tools vis-à-vis China.

- Screening of inbound Chinese investment in strategic sectors.

- Acknowledgement of supply chain dependency risks.

Scoring system (0–2)

- 0 – Permissive stance: Downplays strategic or economic risks; opposes defensive measures; advocates continued or expanded engagement with China on commercial and industrial grounds.

- 1 – Selective assertiveness or status quo: Acknowledges specific risks but supports a cautious or calibrated response; favours preserving current levels of economic and political engagement.

- 2 – Hawkish stance: Consistently frames China as a structural strategic challenge; supports robust EU-level trade and industry policy tools to reduce dependency, defend against coercion and unfair competition.

The China axis score is the average of the eight issue scores.

Acknowledgements

The author would like to thank Kat Fytatzi for her editorial support throughout the process, and Nastassia Zenovich for her meticulous work on the graphs. He is also grateful to Sonia Li for research support; to Szymon Kardaś, Camille Lons, Alberto Rizzi, Janka Oertel and Emmanuel Molding Nielsen (Think Tank Europa) for their advice and guidance.

[1] Data from polling conducted by Project Tempo, an independent, non-partisan research and advisory organisation, in 2024 on European voter attitudes to the economy, politics and climate change. [unpublished]

The European Council on Foreign Relations does not take collective positions. ECFR publications only represent the views of their individual authors.