Countries around the world will have to engage in a wholesale transformation of their economies and infrastructure if they are to meet their environmental targets. Climate is rapidly becoming inextricable from the more conventional forms of political and material power

The transition away from a carbon-fuelled economy is now widely accepted as inevitable. The politics of global resources and supply chains are being reshaped by an emerging international consensus on the need to reach ‘net zero’ greenhouse-gas emissions during the second half of the twenty-first century. This race to zero carbon is driven by a combination of technological progress, declining costs, rising investment, and policy measures to support the transition.

The fossil fuel industry may still underpin the global economy but, as its strategic importance and market value decline, so will its political power. A large proportion of the world’s remaining oil, gas, and coal resources – and the associated downstream infrastructure that cannot be repurposed – will become stranded assets as green alternatives and carbon regulation become more popular, with high-cost producers at particular risk. Similarly, countries with large and relatively new industrial bases may experience sharp economic adjustments in the medium term unless they can retrofit their assets to use green energy molecules and electrons, including hydrogen, ammonia, and biofuels. States that rely on recently built steel furnaces and cement kilns – such as China, India, and several Middle Eastern nations – are likely to be among those most affected by these developments.

At the same time, the physical effects of climate change and concurrent environmental crises will have an especially severe impact on many developing countries, particularly African states, low-lying Pacific island nations, and those that host biodiverse, fragile habitats in tropical regions. Habitat and biodiversity loss, land-use changes, a rise in the sea level, and desertification will all heighten the need for investment in adaptation and resilience measures. They will also affect the availability, distribution, and productivity of arable land and coastal fishing waters, and will alter human and animal migration patterns. In the long term, these changes will affect the distribution of economic and political power between states, including within supranational bodies.

In this shifting and unpredictable environment, countries increasingly weaponise climate diplomacy. Global players exercise diplomatic power through the timing and substance of their announcements of national targets for reducing carbon emissions, the policy measures accompanying them, and the conditions they place on related financial aid. For instance, China made a surprise announcement in September 2020 that its carbon dioxide emissions would peak “before 2030” and that it would aim to achieve carbon neutrality by 2060. This expression of a marked rise in China’s climate ambition emphasised the country’s sovereignty over its development pathway.

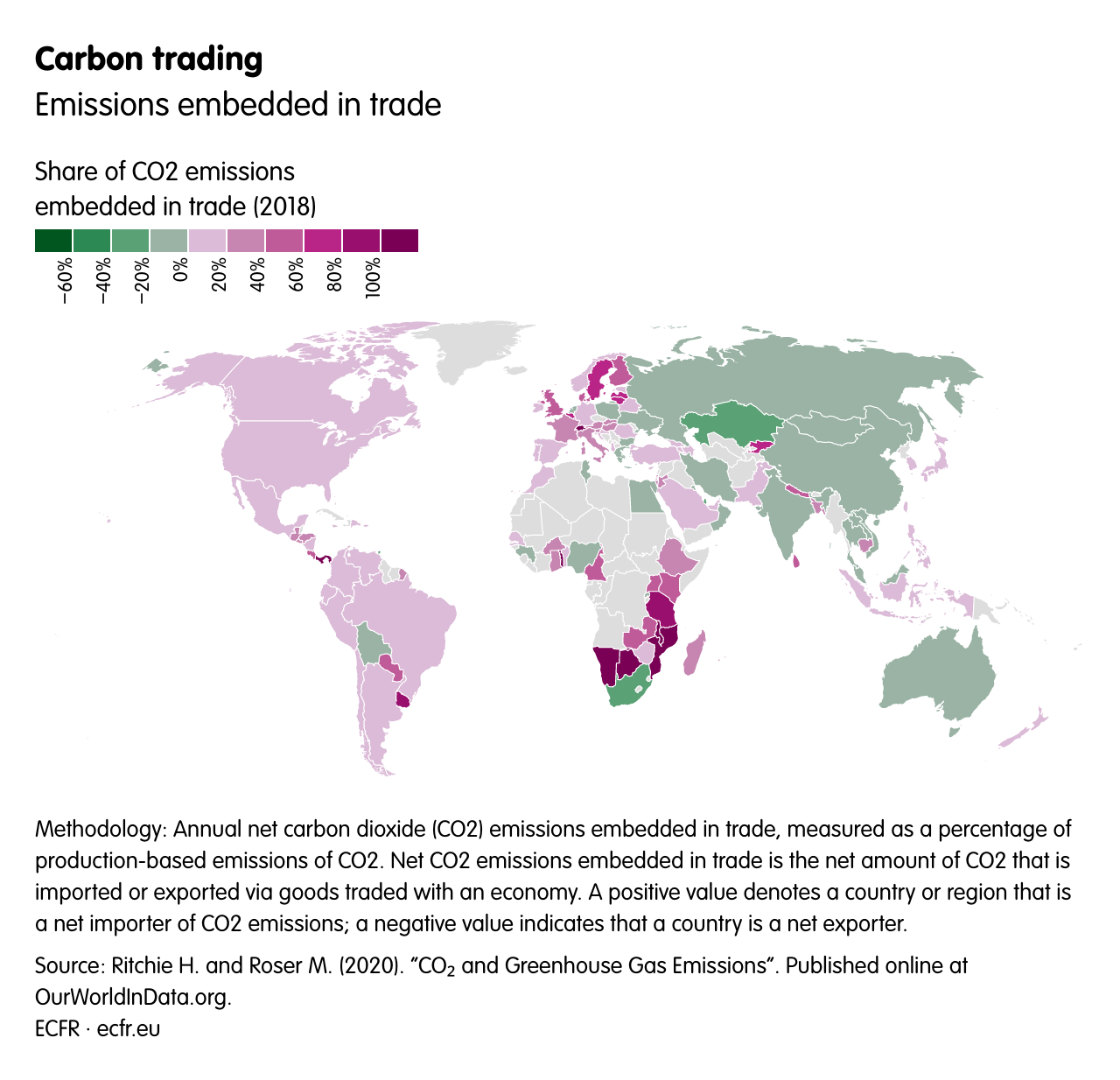

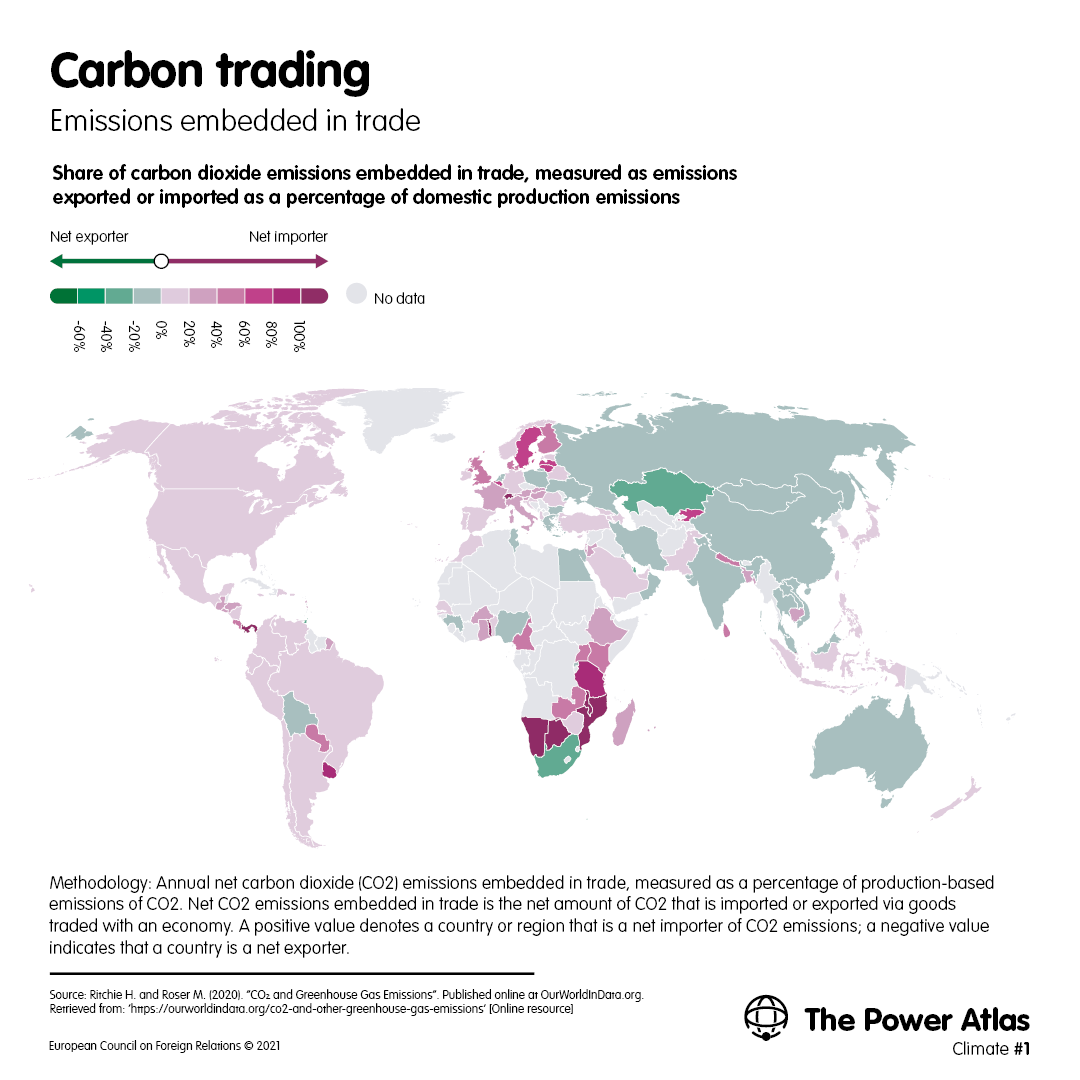

The European Union is wielding its economic power through legislative proposals under the European Green Deal. The EU may be positioning itself to benefit from first-mover advantages in key industries of the future by proposing unprecedented measures to tax carbon-intensive imports at its borders (see: Map 1) – despite the diplomatic risks of doing so. Ultimately, this move may prove highly beneficial to societies around the world by accelerating the adoption of sustainable practices. But its short-term effect is to protect European industries as they improve their ability to transition away from carbon, and to place the EU’s trade partners in developing countries under greater pressure to introduce the same carbon pricing measures.

Emissions mitigation and adaptation are closely linked to investment, but states with deep pockets have long avoided financial commitments to green the economies of countries with less responsibility for, and greater vulnerability to, climate change. Despite the need to recover from the pandemic and to mitigate the increasingly obvious impact of climate change, the G7 has repeatedly failed to meet its target of providing developing countries with $100 billion per year in climate finance. This funding target – which is a drop in the ocean relative to developing countries’ overall investment and adaptation needs, and which is included in the 2009 COP16 climate accords – is intended to help these states manage the impact of climate change, and to develop national action plans to counter it.

Given the importance of technology and innovation in adapting many sectors to the climate challenge, there is another source of power that will play a growing role in states’ attempts to make the transition to net zero. Access to the labour force and natural resources necessary to develop green technology, and the ability to exploit and monetise them, will also shape states’ capacity to strike economic bargains on climate in the coming decades.

The map of climate and resources power is complex and uncertain – but governments need to understand it if they are to operate in a world that is compelled to take action on climate change.

Energy transition

The global energy mix

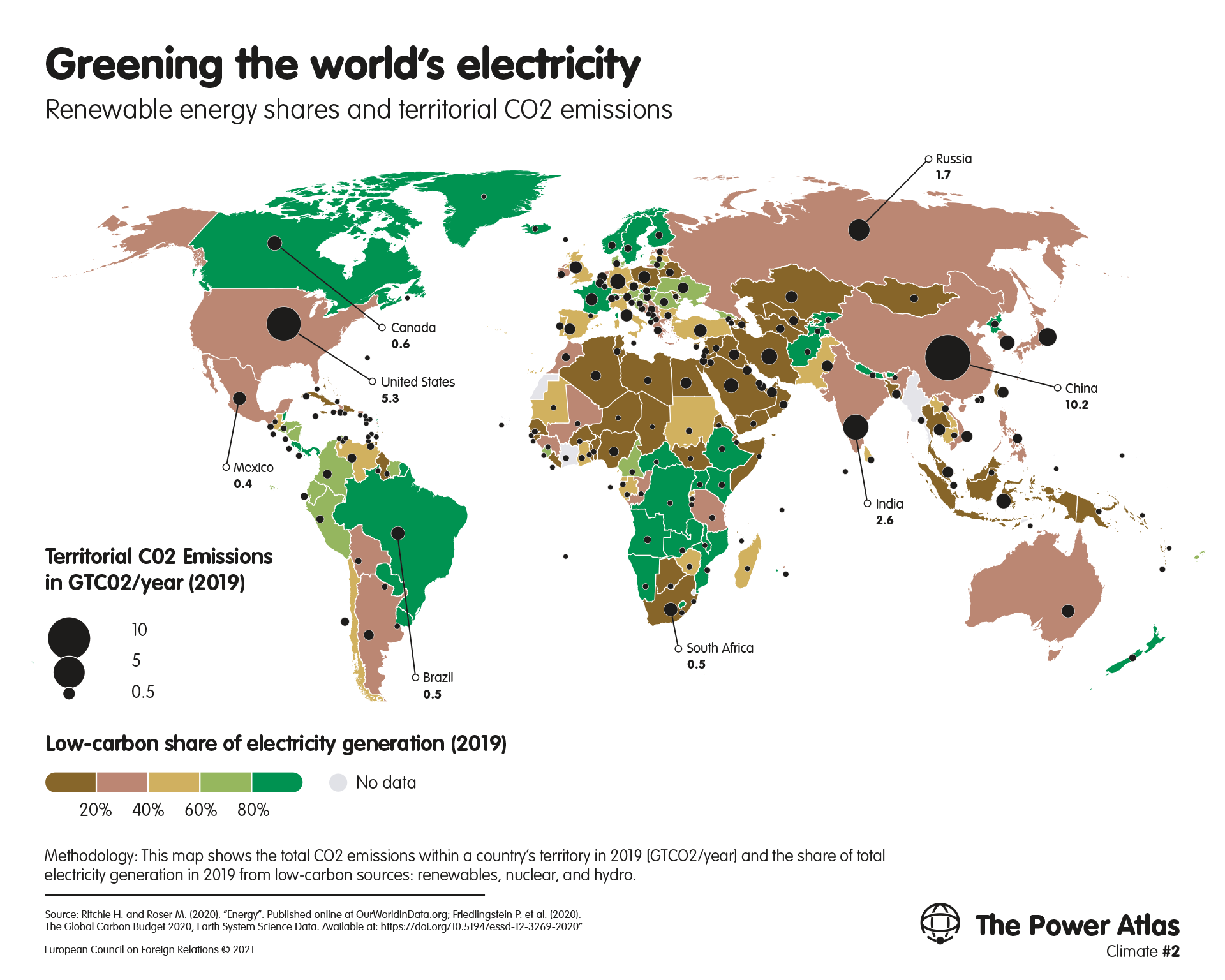

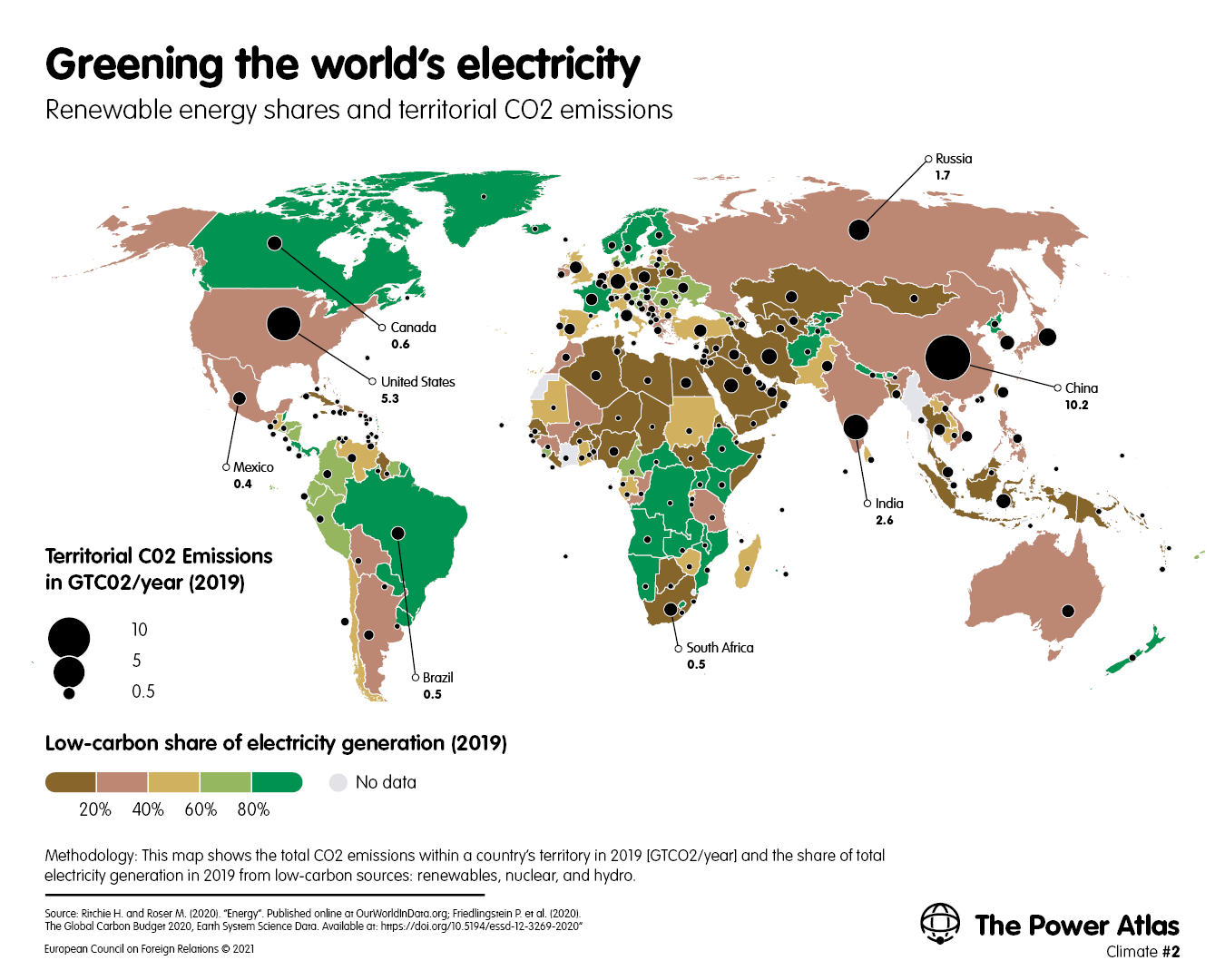

Today, there is considerable variation in the carbon intensity of countries’ energy mixes (see: Map 2). The picture is incrementally shifting as they add new – usually renewable – sources of power and heat, and retire older ones. One critical factor in the energy mix is demand, which changes as countries experience demographic growth or decline, and as their economies develop in various sectors – in some cases, with the explicit goal of transitioning away from carbon use. Energy demand is likely to grow significantly in some of the largest, most carbon-intensive economies, particularly those of India, South Africa, Indonesia, Mexico, and China (even as it remains relatively steady in Europe and the US, both of which are decarbonising). At the same time, these countries will come under pressure to ensure that future additions to their energy capacity are zero-carbon, secure sufficient access to renewable electricity, and forgo easily accessible fossil fuel alternatives.

Given the size of some countries’ fossil fuel economies and the speed of their economic growth, incremental transformation will be insufficient to meet the climate challenge. They will need to implement ambitious policies if they are to phase out fossil fuels. Regardless of whether they do so, there may be rapid changes in international demand for fossil fuels, shifting the balance of power between energy-producing and energy-importing countries.

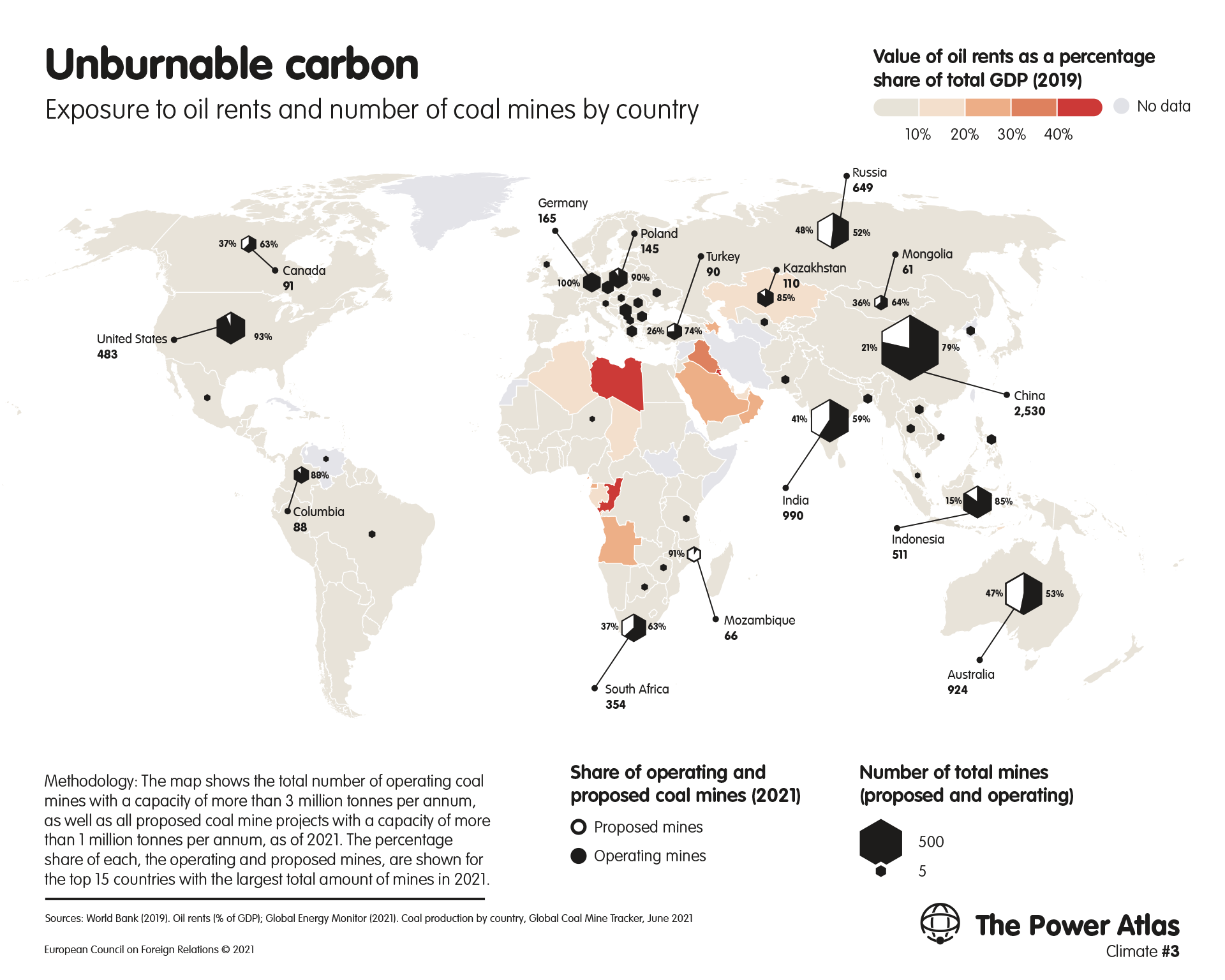

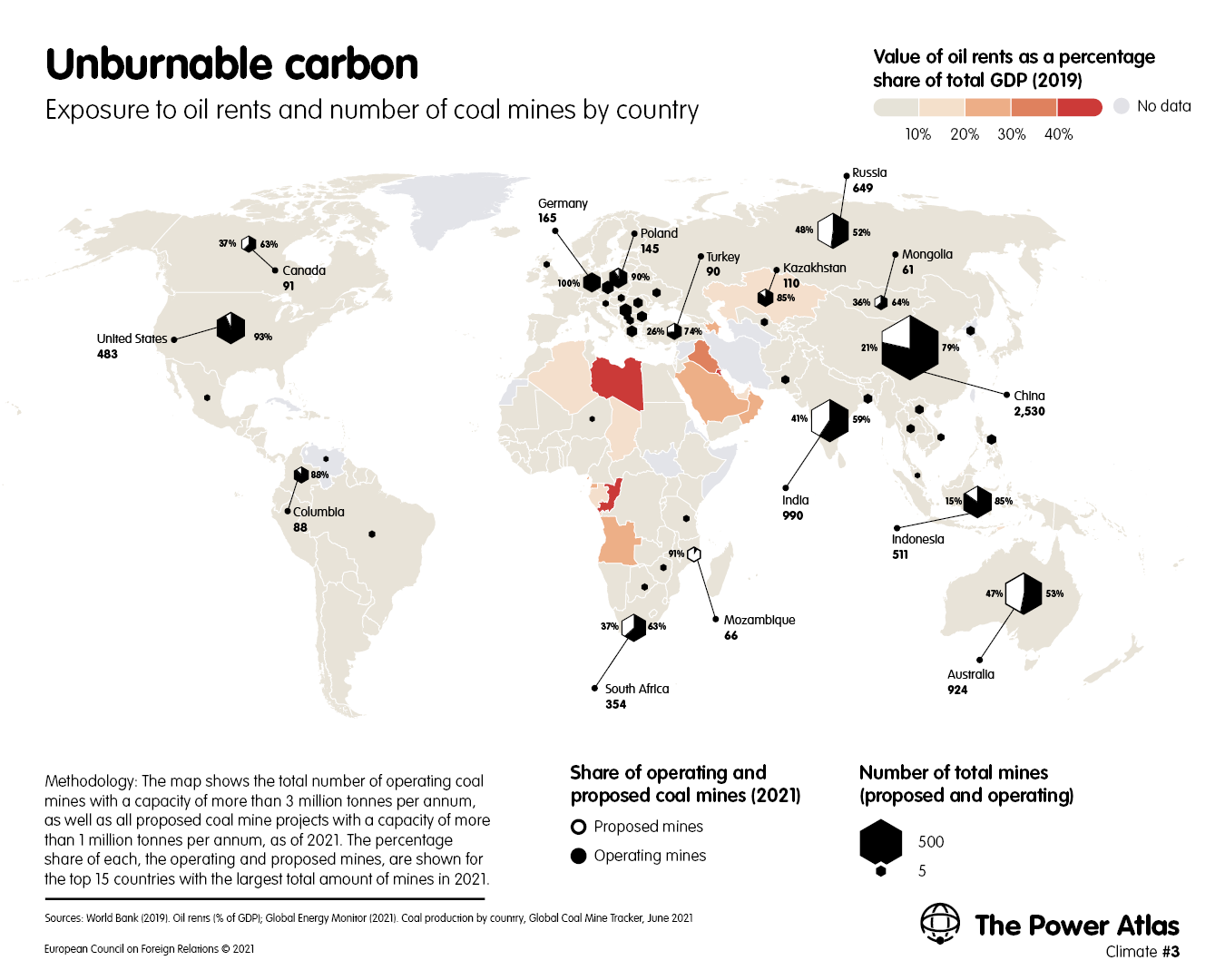

Fossil fuel extraction is likely to become economically unviable for the United States, Canada, and other high-cost oil producers before it does for the lowest-cost OPEC producers, such as Saudi Arabia, Qatar, Iraq, and Kuwait (although those in the former groups are less economically dependent on energy production; see: Map 3). Even as oil and gas markets shrink – and as technologies for alternative sources of power are still coming on line – socio-economic pressure to monetise carbon before it is too late may lead these and other economies to expand production in the short term. They could thereby expose themselves to greater stranded-asset risks – in what is sometimes called the ‘green paradox’. The extent to which this occurs will depend on whether producer countries are convinced that other global players are serious about the transition away from carbon, these states’ internal development needs and political makeup, and the availability of other sources of revenue.

Green energy is the new gold: the race is on to develop and deploy technologies that allow for the production and consumption of non-carbon energy. There are high hopes for success in sectors such as renewable energy, smart grids, and new energy vehicles. But, in many countries, it will likely be disruptive to replace electricity generation infrastructure quickly enough to decarbonise.

Technological solutions are emerging in sectors where electrification is challenging – such as steel, cement, shipping, and aviation – but face a long road to commercialisation. Some governments have responded to this challenge more quickly than others, by investing and innovating in, for instance, carbon capture and storage, battery storage, and advanced nuclear technologies (China and the US), and green hydrogen and battery production (the EU and China).

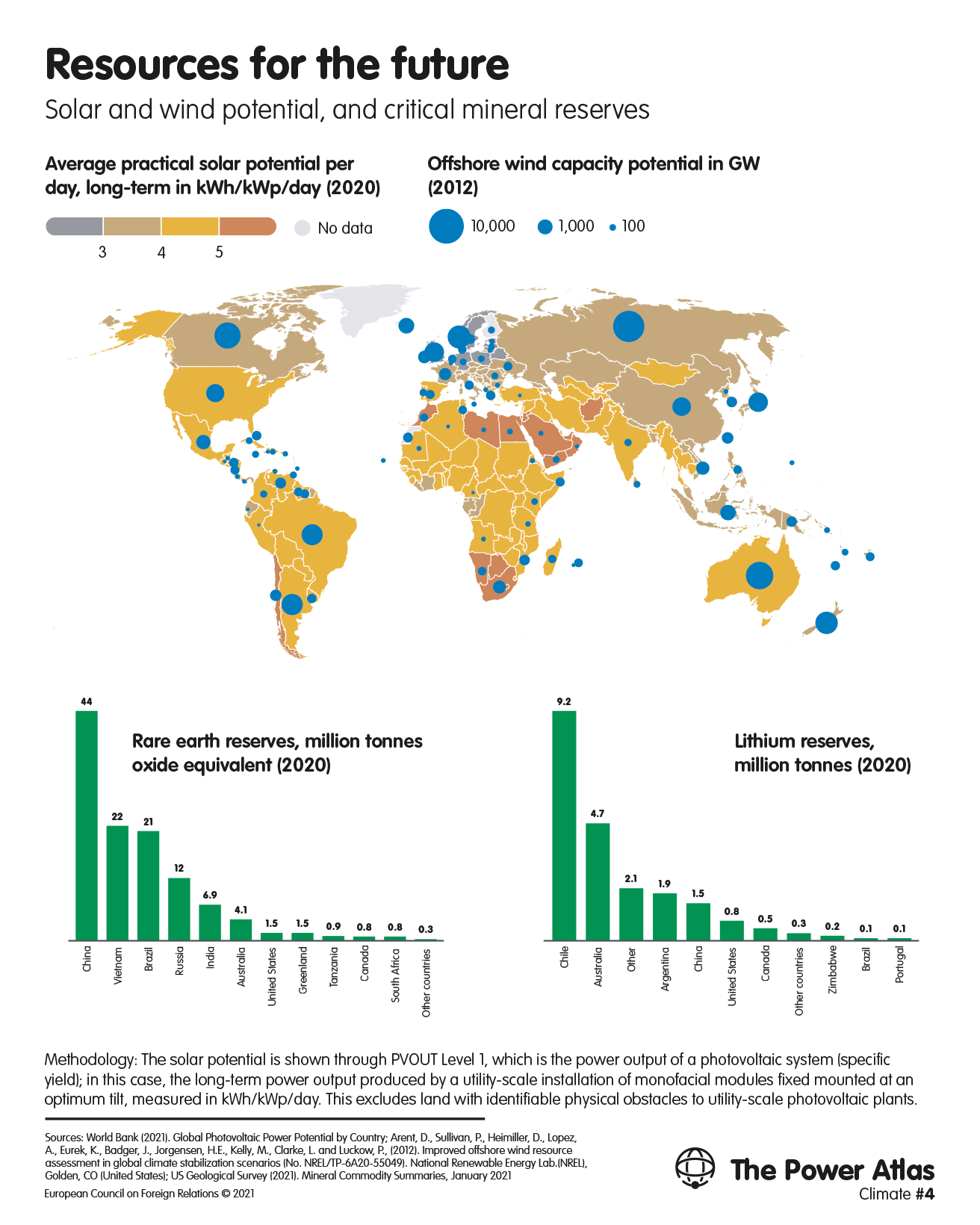

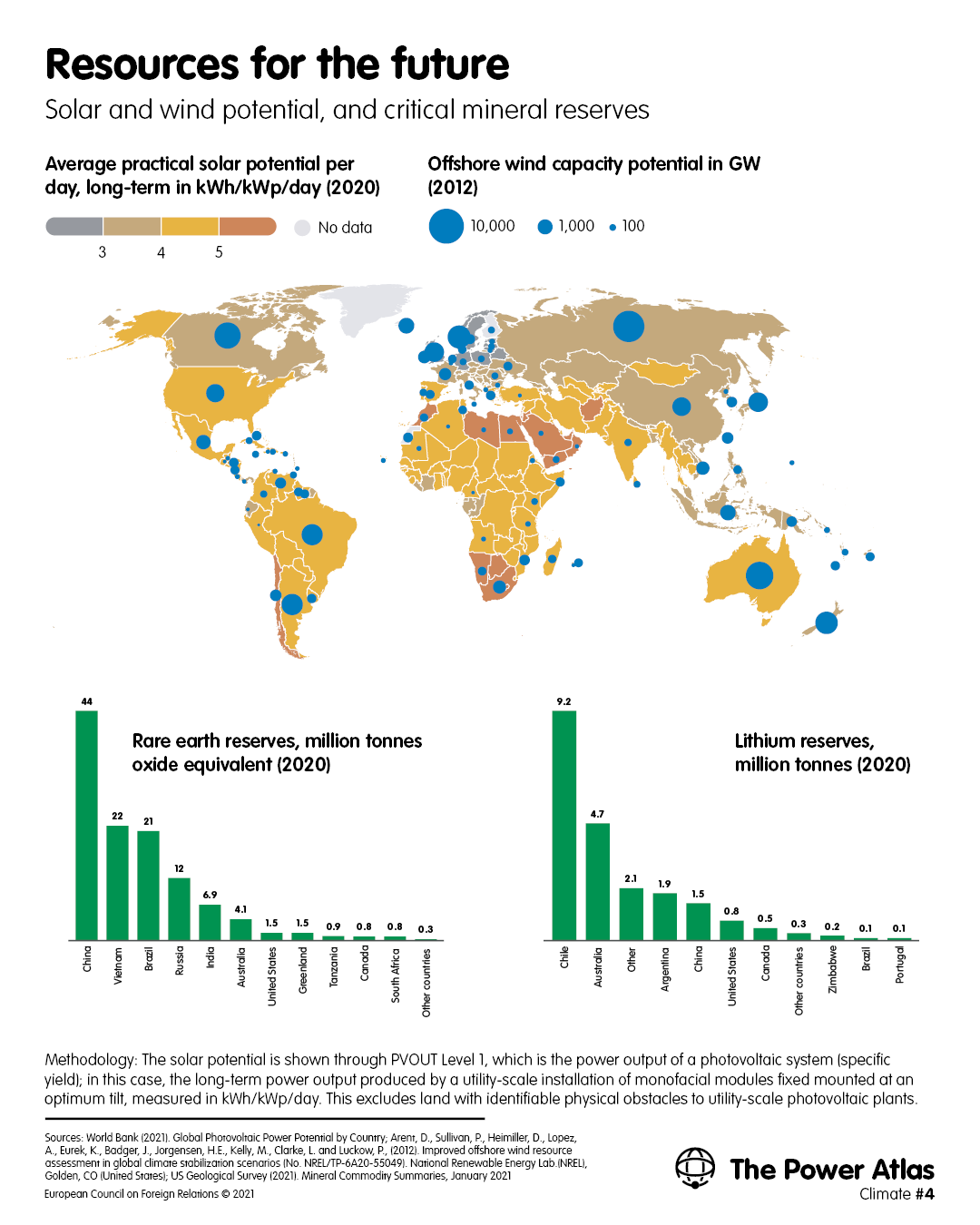

Once these and other technologies become commercially viable, states will need significant natural resources and infrastructure to adopt them. As renewable, electricity-based fuels displace oil and gas, countries with the largest, lowest-cost solar and wind resources – and those that produce the rare earth metals used to harvest them – may be well positioned to strike energy bargains with the world’s large energy consumers. States and regions with areas of particularly high solar photovoltaic potential include Chile, Mexico, the US, Morocco, Algeria, Namibia, South Africa, Botswana, most of the Middle East, China, and Mongolia. Locations with high wind energy potential include the United Kingdom, Ireland, Iceland, and Scandinavia, as well as the coastlines of Canada, the US, Chile, Argentina, South Africa, Namibia, Somalia, Russia, Australia, France, south-eastern China, and New Zealand (see: Map 4).

Nonetheless, profitably exploiting these resources will require access to rare earths. These 17 elements are relatively common throughout the Earth’s crust, but many deposits of them are undeveloped. China, Vietnam, Brazil, Russia, India, and Australia currently have the largest reserves of rare earths. Reserves of lithium – a metal that, like cobalt, is essential for battery production – are primarily concentrated in Bolivia and Argentina, followed by Chile, the US, Australia, and China.

Climate risks

Vulnerable states

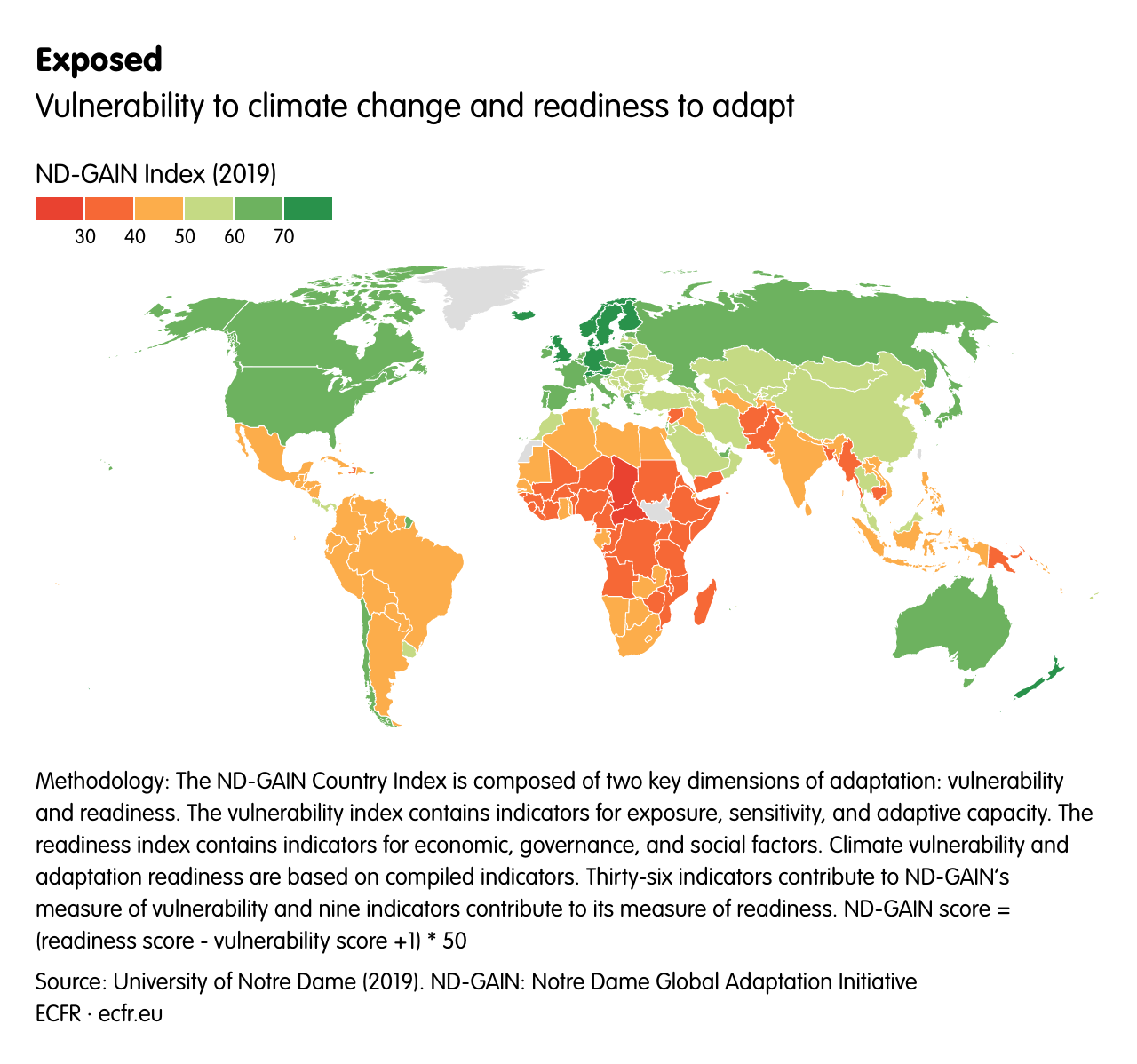

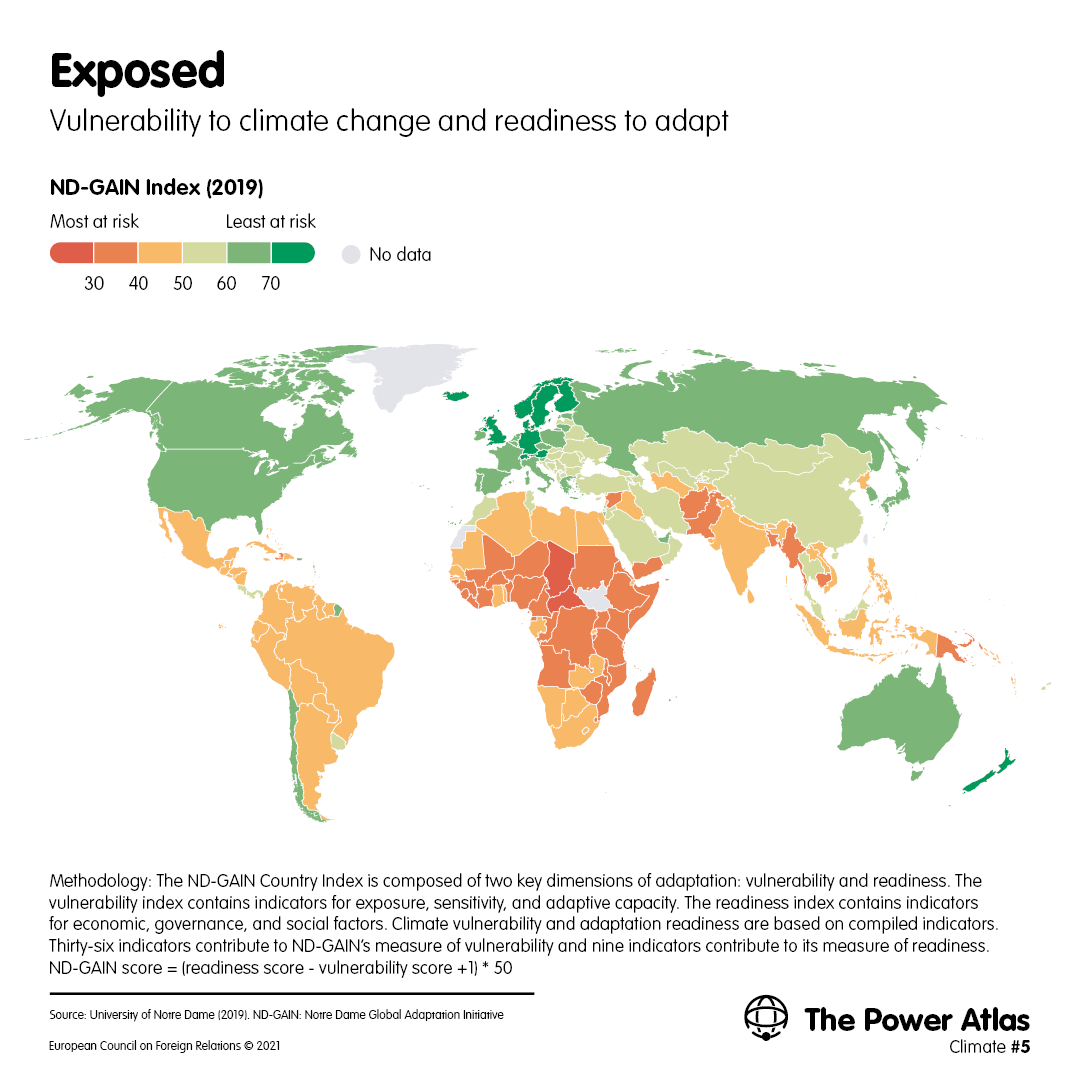

The Notre Dame GAIN index ranks countries’ readiness to deal with the impact of climate change across the economy, governance, and social infrastructure, as well as their vulnerability according to exposure, sensitivity, and adaptive capacity (see: Map 5). Most of the poorest performers in the index are low-income and lower-middle-income states in North Africa, sub-Saharan Africa, Latin America, south Asia, south-east Asia, and the Pacific. The climate-related risks that these countries face involve extreme weather events, a rise in the sea level, water stress, and crop failures – all of which can increase mortality rates. These problems could lead to a host of second-order effects, including human displacement, disease, health system failures, and chronic socio-political instability. Pacific island states could be submerged by a rise in the sea level, as could large swathes of low-lying land in south Asia, north America, and Europe in particular.

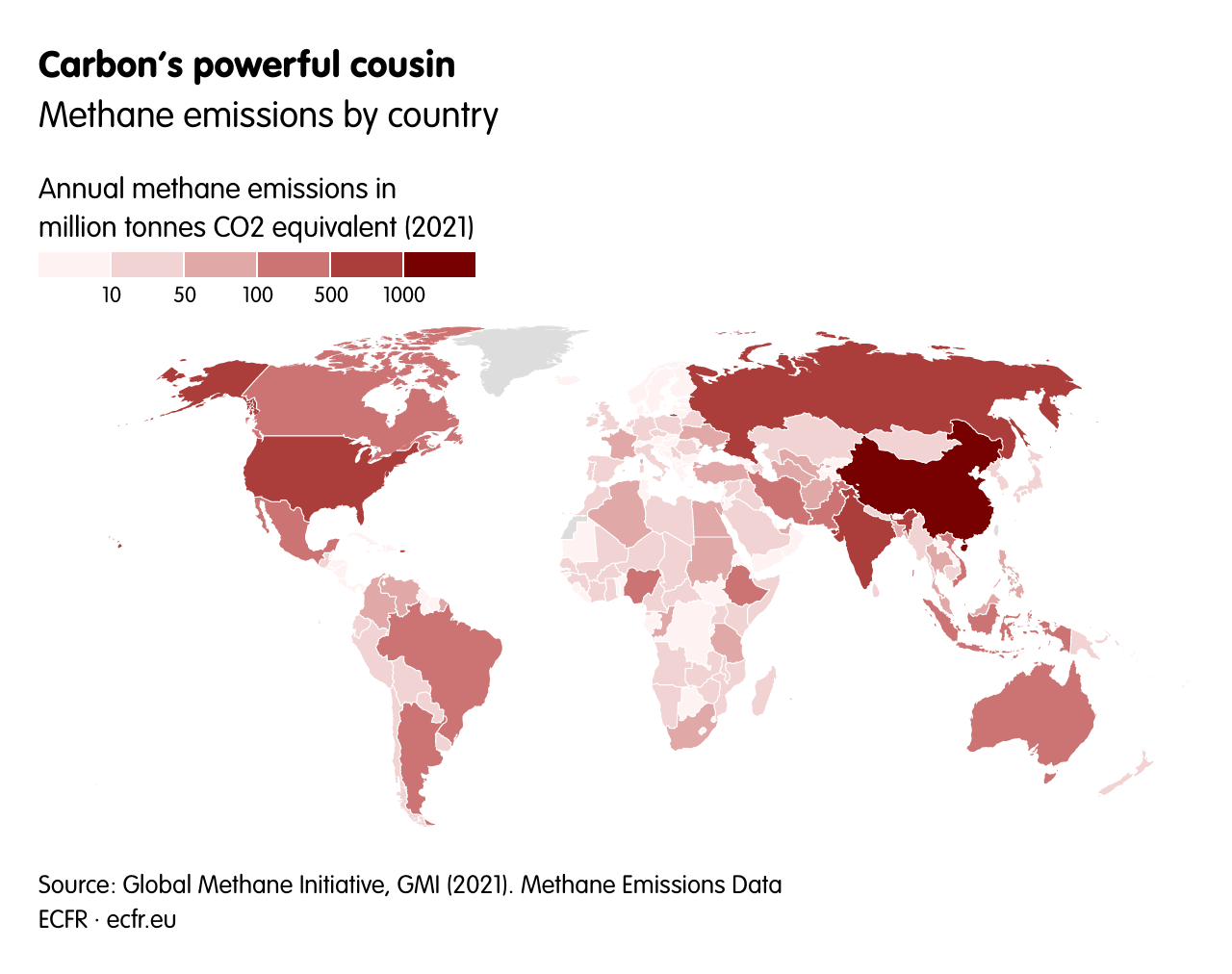

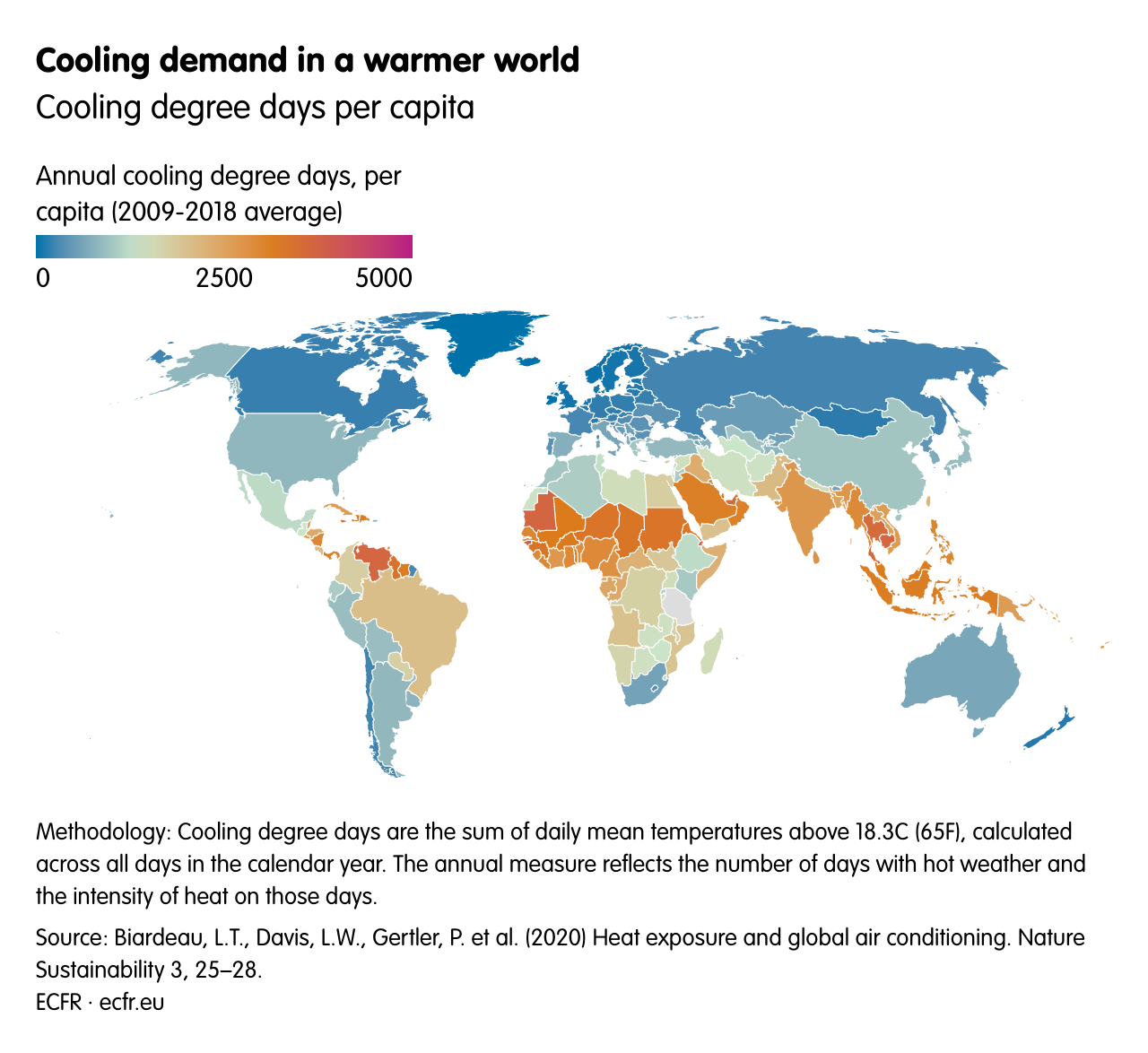

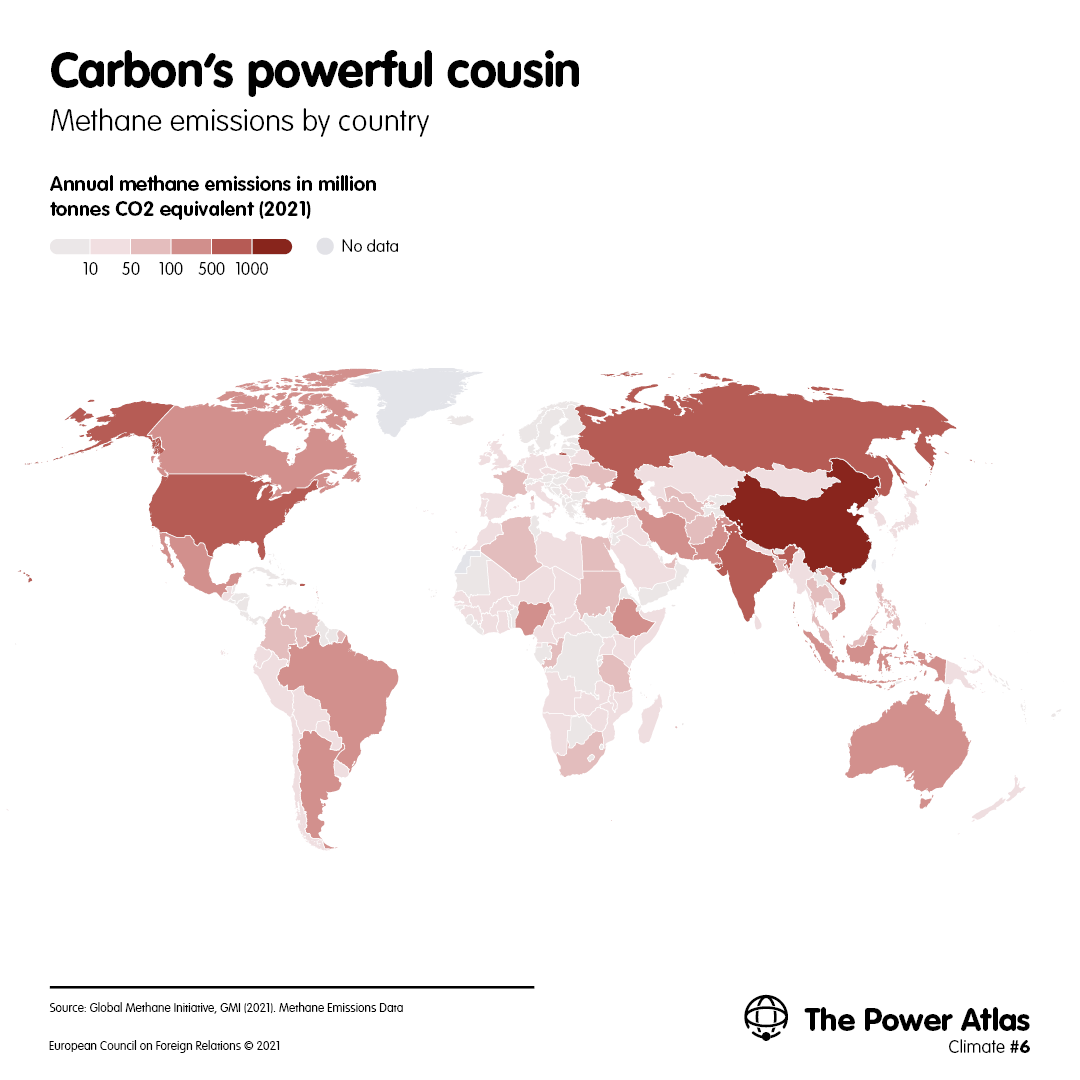

There are many pathways for the global transition to net zero, each of which has uncertain climate implications. Some pathways risk simply substituting one set of problems for another, while others risk truly catastrophic outcomes. For instance, if the global shift away from coal becomes a shift towards gas, rising upstream methane emissions (see: Map 6) may increase atmospheric warming in the short term. Furthermore, if heat waves become more widespread and frequent, there will be a sharp rise in demand for electricity, including that from fossil-powered generators. This problem, which is particularly acute in countries prone to extreme temperatures, would also contribute to warming. For example, India is projected to see the greatest share of increased cooling degree days – at 27 per cent of the global total – followed by China, Indonesia, Nigeria, Pakistan, Brazil, and Bangladesh (see: Map 7). Other countries in the top 30 for such increases are largely in south-east Asia, north America, Africa, and central America.

A misjudged or delayed transition to net zero would risk crop failures, fishery collapses, and ocean eutrophication. Similarly, the irreversible destruction of oceanic and land-based carbon sinks would reduce the Earth’s capacity to absorb atmospheric carbon and increase both warming and the need to remove greenhouse gas.

Water stress, agriculture, and food security

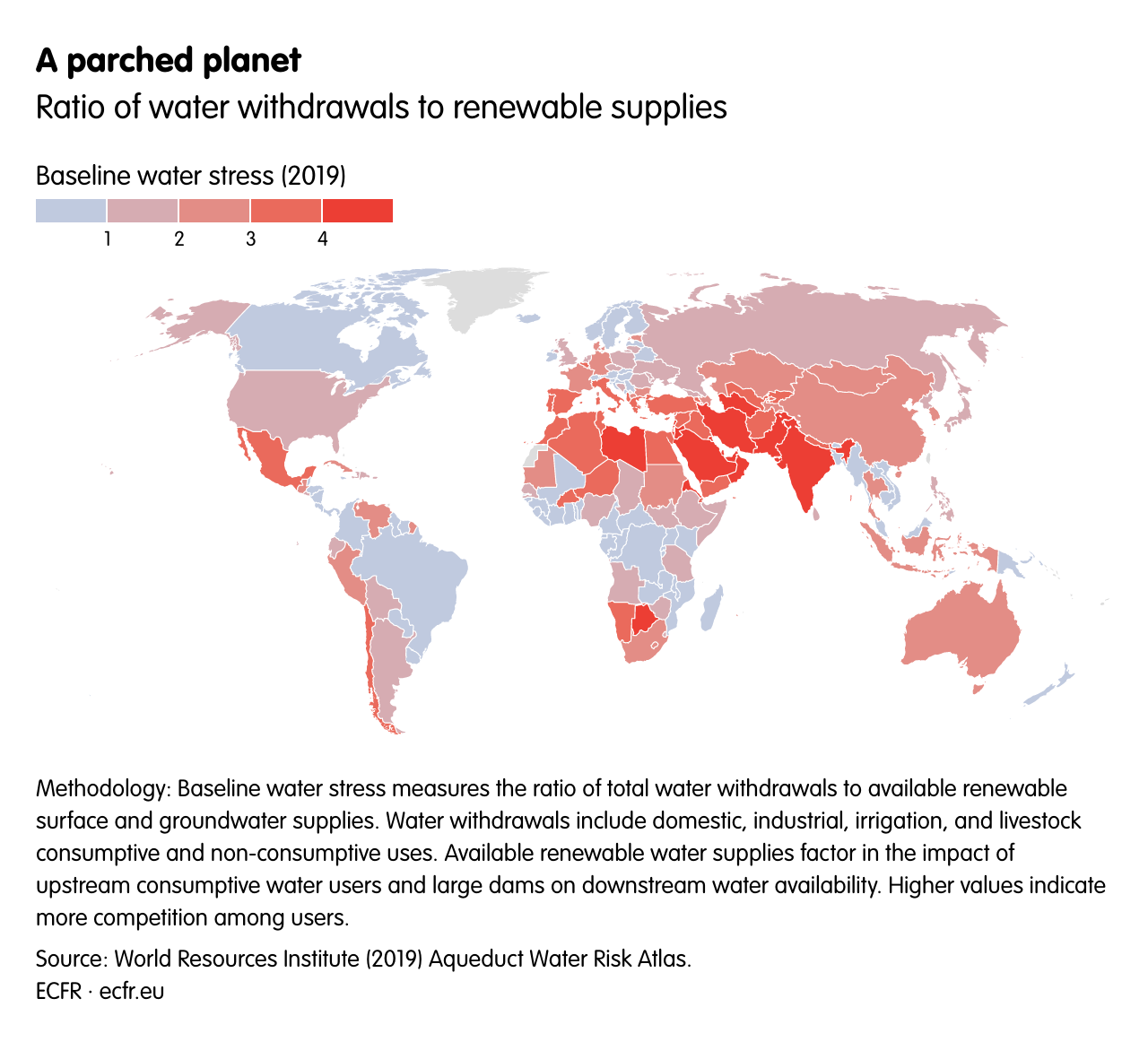

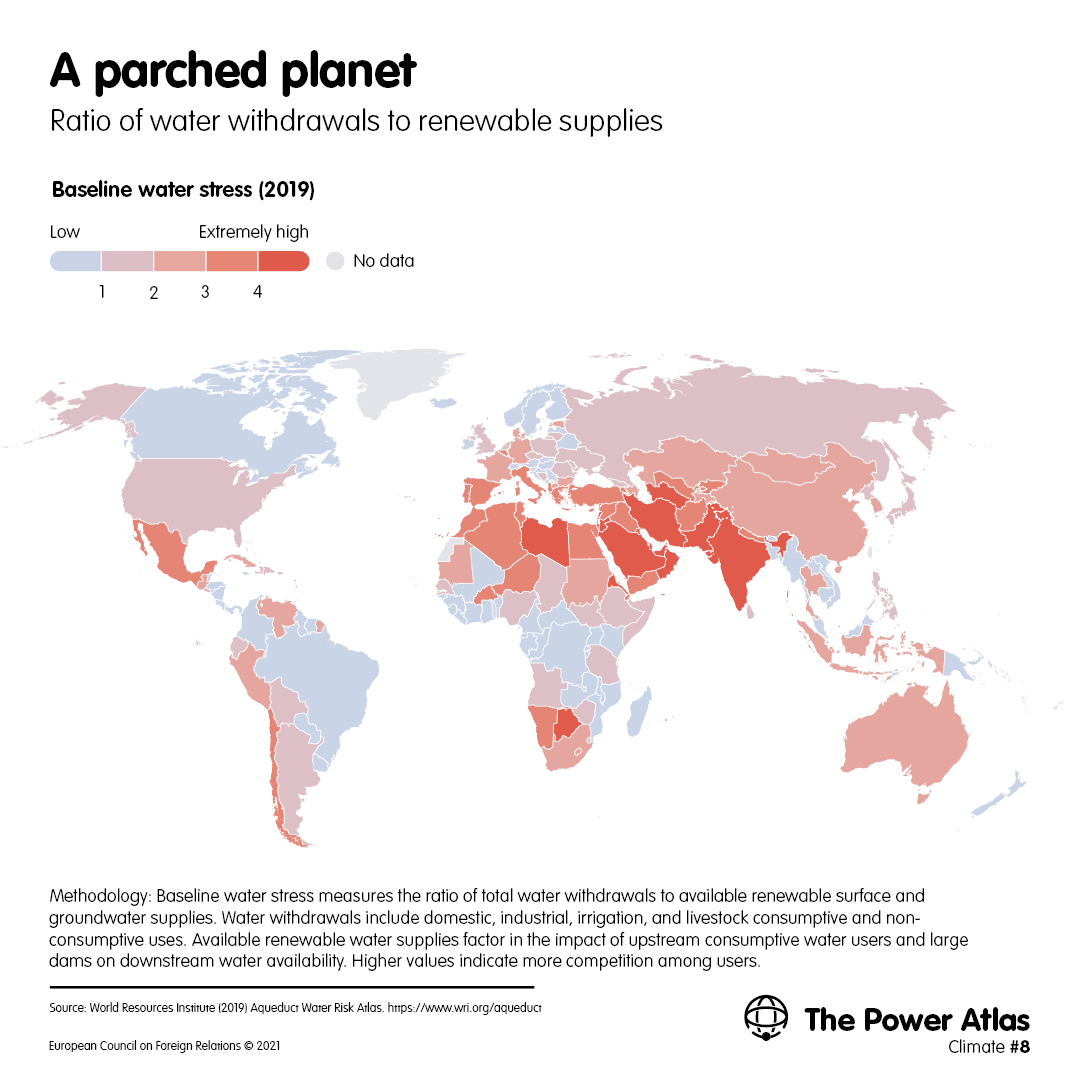

Aside from energy, water and food will be the most precious resources in a climate-stressed world that is home to a growing and increasingly affluent population. In most projected climate scenarios, those with access to ample supplies of water and food are likely to have broader developmental and trade options, and to be able to insulate themselves from the worst human costs of climate change. By 2040, the most acute water stress will likely be felt in states in the Middle East, south Asia, and central Asia (see: Map 8), while those least at risk (in part due to lower consumption) are countries in central and southern Africa, as well as central America. Nations with the largest arable land areas include the US, India, Russia, China, Brazil, and Canada.

Exposure to the risks of climate change and the energy transition, particularly for countries lacking the resource to adapt or diversify respectively, has long been a major sticking point in international climate negotiations. This is because developed countries have resisted providing the necessary financial and technological resources to address these risks. Adaptation and vulnerability will continue to be pivotal negotiating issues as countries with the least to gain, most to lose, and least capacity to protect themselves require progressively greater financial and technical support from wealthy nations – support that may well not be forthcoming in the absence of incentives to provide it.

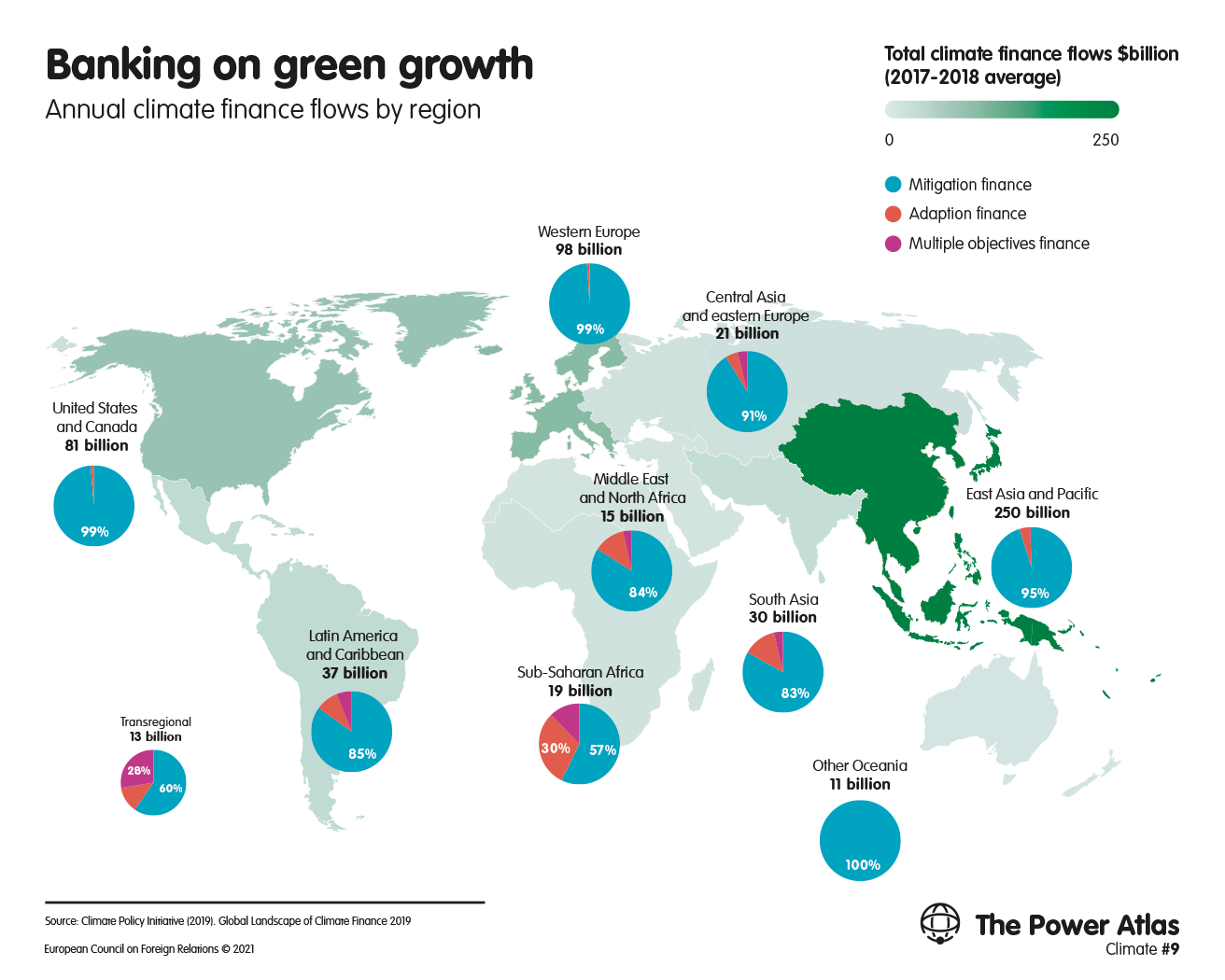

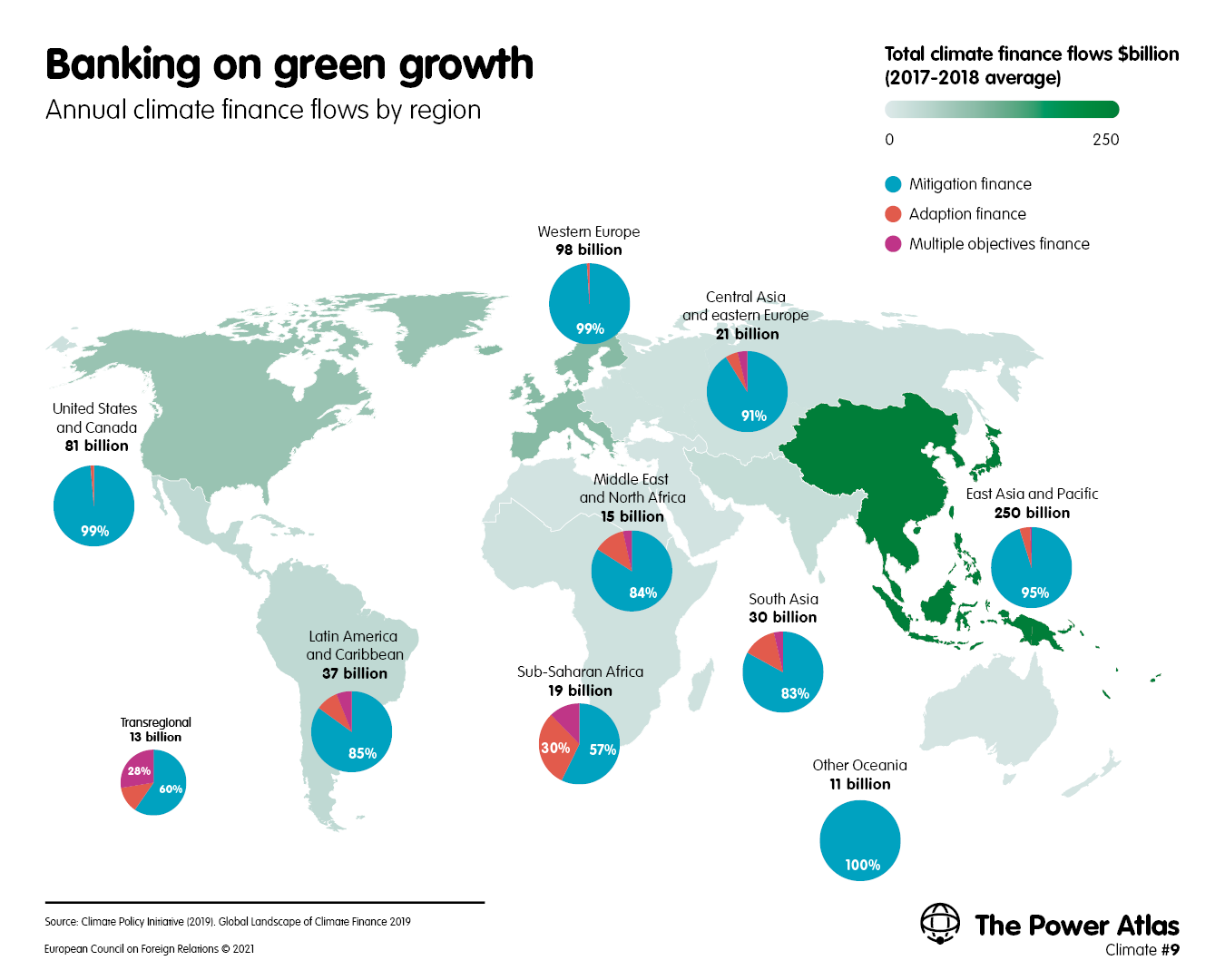

Historically, financing of climate change mitigation has dominated international and domestic, public and private, climate finance flows (usually involving renewable energy and energy efficiency projects). The amount of funding flowing into adaptation, particularly in vulnerable countries, is far less, and a fraction of what is needed to protect against the projected impact of climate change in these countries (see: Map 9). Meanwhile, climate mitigation finance and development aid remain critical to help poorer countries – which have underdeveloped financial markets and power grids – create alternatives to carbon-intensive infrastructure in the medium and long term, and to drive down the costs of technologies for renewable energy generation, and the financial costs of building and operating them.

Climate-related financial flows are still very small relative to overall investment. Although global and regional powers may seek to build up spheres of influence by bolstering their climate finance commitments and establishing green financial hubs, climate finance will remain largely marginal without a wholesale realignment of financial markets through regulation. At present, international bargaining over climate finance is more a question of optics than a genuine transfer of power from developed to developing countries.

Still, optics matter. And countries that receive aid do not quickly forget where this support came from when it was needed. The US-led Build Back Better World initiative, announced after the 2021 G7 meeting, focuses on climate (alongside health, digital technology, and gender equality). The initiative underlines the West’s determination to compete with China and other powers in the struggle for control and influence over the key sources of power and connectivity in a post-carbon world.

Fossil fuel subsidies and investments

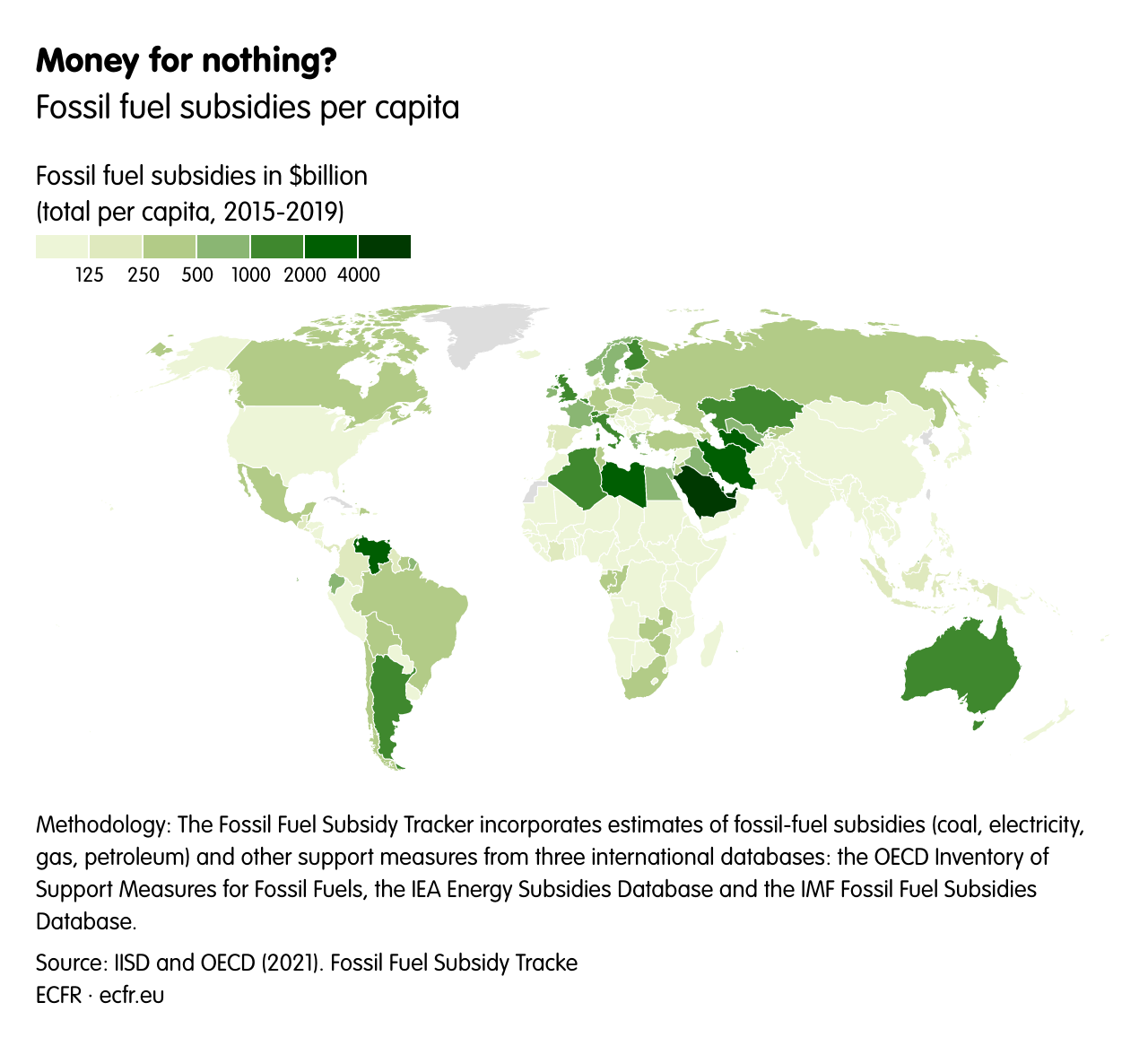

Infrastructure that emits large amounts of carbon – or that facilitates market access for high-carbon fuels and activities – still dominates new investment. This is partly due to the decisions made by G20 governments, which have provided an estimated $3 trillion in fossil fuel subsidies since they adopted the Paris Agreement, in 2015 (see: Map 10). If the international consensus on the need for emphatic climate action holds and technological progress continues on current trends, investment in carbon-emitting infrastructure should become less economical. But should the political balance shift or innovation in key areas stall, there could be a low-profile increase in investment in fossil fuels. China’s sprawling Belt and Road Initiative (BRI), which involves more than 120 countries, is particularly relevant in this respect. While some participants in the BRI are trying to green investments linked to the initiative, there are significant administrative and capacity-related obstacles to doing so. Despite the apparent slowdown in China’s overseas coal investments since the start of the pandemic, there is a high risk of carbon-intensive investment in BRI infrastructure in sectors such as gas, transport, mining, and forestry.

New commercial bank financing for high-carbon fossil fuels by country of domicile (total, 2016-2020)

$10 billion

Defined amounts below $10 billion

Delays to climate action

To compete, thrive, or – in many cases – simply survive in this environment, states and other international and subnational actors will need to act quickly and astutely. They will need to understand the new map of climate and resources power that is being drawn and redrawn before their eyes.

Some countries appear likely to make short-term tactical gains from climate change in various areas. And their efforts to capitalise on these potentially short-lived opportunities may cause geopolitical ripples, or even prove to be serious strategic mistakes, in the coming years. Canada and Russia, for instance, may well see a significant expansion of fertile, arable areas as permafrost melts (although this is highly contingent on seasonal climate variability and access to water resources for irrigation). Similarly, as ice cover recedes in the summer months, shipping costs and transit times could fall due to the expansion of routes crossing Canadian and Russian territorial waters through the Arctic Ocean. Given that such developments could lower the distances required for commercial shipping, it seems likely that they could benefit European states dependent on the Suez route more than American ones reliant on the Panama Canal.

Stalling climate action to reap these potential benefits, however, could be very risky for these countries and catastrophic for others. Accelerating ice and tundra melt in polar regions could destabilise water supplies, incentivise the permanent conversion of forested areas into arable land, drive up methane emissions from livestock, release vast quantities of trapped methane, and raise the sea level. Therefore, greater access to arable land would not automatically boost the economies of Arctic countries, particularly if it was accompanied by geopolitical tension and conflict.

Although there is a great deal of uncertainty about many future dynamics of climate and resources power, it seems that swimming against the tide of climate action will not pay off. Given the wholesale transformation of economies and infrastructure states will have to engage in to meet their environmental targets, climate and resources power is rapidly becoming inextricable from the more conventional forms of political and material power explored elsewhere in this atlas. Global climate politics is likely to undergo rapid shifts as countries try to implement the Paris Agreement. But leadership in achieving the deal’s goals seems more likely to pay dividends than efforts to prevent or slow the transition.

We use cookies on our website. Some of them are essential, while others help us to improve this website and your experience.If you are under 16 and wish to give consent to optional services, you must ask your legal guardians for permission.We use cookies and other technologies on our website. Some of them are essential, while others help us to improve this website and your experience.Personal data may be processed (e.g. IP addresses), for example for personalized ads and content or ad and content measurement.You can find more information about the use of your data in our privacy policy.You can revoke or adjust your selection at any time under Settings.

If you are under 16 and wish to give consent to optional services, you must ask your legal guardians for permission.We use cookies and other technologies on our website. Some of them are essential, while others help us to improve this website and your experience.Personal data may be processed (e.g. IP addresses), for example for personalized ads and content or ad and content measurement.You can find more information about the use of your data in our privacy policy.Here you will find an overview of all cookies used. You can give your consent to whole categories or display further information and select certain cookies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}